Kalkine has a fully transformed New Avatar.

Company Overview: Service Stream Limited is a provider of essential network services, including access, design, build, installation and maintenance across copper, fiber and wireless telecommunications networks, as well as to private and public energy, and water entities. The Company's segments include Fixed Communications, Mobile Communications, and Energy & Water. The Fixed Communications segment provides design, construction, maintenance and customer connection services to the owners of telecommunications network infrastructure in connection with the roll-out of the National Broadband Network in Australia. The Mobile Communications segment provides program management and turnkey services for infrastructure projects in the telecommunications sector. The Energy & Water segment provides a range of metering and energy services to electricity, gas and water networks, and through the Customer Care business provides contact center services and workforce management support for contracts.

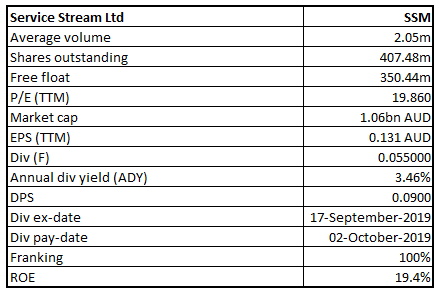

SSM Details

Decent Performance in FY19: Service Stream Limited (ASX: SSM) is one of the leading essential network services providers in Australia. The market capitalisation of the company stood at circa $1.06 Bn as of 31 October 2019. In FY19 (for the period ended on 30 June 2019), the company delivered another year of growth across all key profitability metrics and the first-time contribution to earnings from the recently acquired Comdain Infrastructure business. During FY19, the company generated revenue (including other income) amounting to $852.2 million, up 35% on FY18 revenue of $632.9 million. This was mainly driven by the growth in each of 2 reporting segments of telecommunications (+10%) and utilities (+156%) with the acquisition of Comdain Infrastructure contributed $160.2 million (+150%) to the latter. The company’s earnings before interest, tax, depreciation and amortisation (or EBITDA) stood at $89.5 million, which implies an improvement from $67.3 million and reflecting 33% YoY rise following average annual growth in the same metric of 38% over preceding 3 financial years. EBITDA growth was achieved by each of telecommunications (+22%) and utilities (+127%), and acquisition of Comdain Infrastructure contributed $11.1 million (+106%) to the latter. Net profit for the company was recorded at $49.859 million, up 21.29% on y-o-y.

As at 30 June 2019, the company managed to retain the net cash position of $10.5 Mn despite outlay to acquire Comdain Infrastructure. Based on the FY19 performance, the Board of Directors declared a fully franked final dividend of 5.5 cents per share, which reflects a rise of 22.2% on final dividend of 2018. The total dividends for FY19 stood at 9.0 cents per share (fully franked), which is 20.0% higher than the prior year.

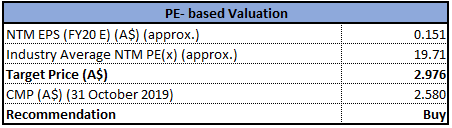

The company has a favourable outlook backed by decent demand for the maintenance services across both telecommunications and utilities markets. Additionally, the company is well-positioned to secure additional organic growth opportunities throughout the core markets. The priorities for FY20 mainly include 1) finalising Comdain Infrastructure integration and maintaining focus towards enhancing the financial and project management controls via the adoption of ERP system, and 2) maintaining readiness to deliver the increased volume of wireless services. Based on the foregoing, we have valued the stock using a relative valuation method, i.e., Price to Earnings multiple, and arrived at a target price of lower double-digit growth (in % term). At CMP of $2.58, the stock of the company is trading at P/E multiple 17.09x of FY20E EPS.

.png)

FY19 Key Financials Measures (Source: Company Reports)

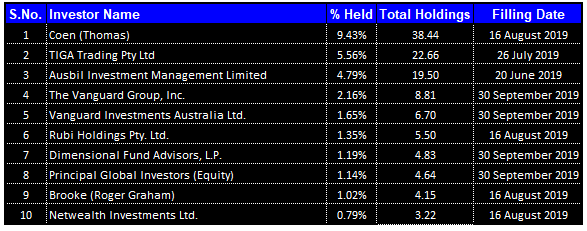

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Service Stream Limited:

Top 10 Shareholders (Source: Thomson Reuters)

Key Margins Higher Than Industry Median: The company’s net margin stood at 5.9% in FY19, which is higher than the industry median figure of 2.7% and, therefore, it can be said that SSM is possessing better capabilities to convert its top-line into the bottom-line. Gross margin stood at 95.6% in FY19, which is also higher than the industry median of 12.9%. The company’s RoE stood at 19.4% in FY19, which is comfortably higher than the industry median figure of 9.9% and, therefore, it can be said that SSM has delivered better return to its shareholders as compared to the broader industry.

SSM’s current ratio stood at 1.25x in FY19, which is higher than the industry median of 1.14x, representing a decent liquidity position to meet its short term obligations. The company’s Debt/Equity ratio stood at 0.20x in FY19, which is higher than the industry median of 0.46x and, therefore, it can be said that SSM’s balance sheet is less leveraged as compared to the broader industry.

.png)

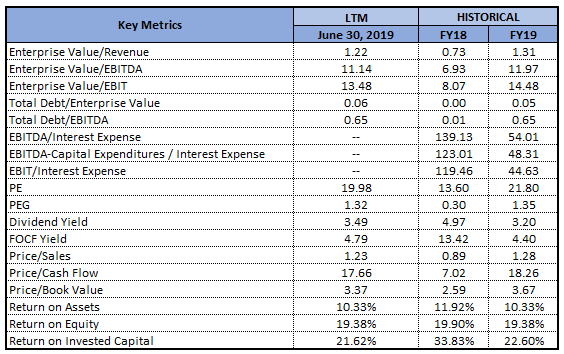

Key Metrics (Source: Thomson Reuters)

Securing of 5G Wireless Design & Construction Agreement: Recently, SSM announced that it has secured wireless design & construction agreement with Optus. The agreement happens to be a panel arrangement in the form of newly awarded Statement of Works for Mobile Deployment (or SoW) with Optus Mobile Pty Ltd, which operates under pre-existing Group Master Supply Agreement with Singapore Telecommunications Limited.

Under Statement of Work (SoW), Service Stream Limited will initial provide site acquisition, design and construction services on the Optus network nationally, with respect to 5G. The agreement also allows for site upgrades, small cell and RANCAP services with regards to existing 4G infrastructure, subject to the future negotiations. The term of SoW happens to be 3 years with an option of 1-year extension.

Extension of NMRA Contract with nbn: Service Stream Limited has made an announcement that it extended Network MACs and Restoration Activities contract with NBN Co. The NMRA contract has been extended for additional 18-month term out to June 30, 2021. Under NMRA contract, which was initially executed in the month of September 2012 as Network Augmentation and Restoration Activities (NARA) contract and that has been extended several times since, Service Stream Limited will continue to provide nbn with services relating to the improvement, maintenance and relocation of infrastructure across its fixed-line broadband network.

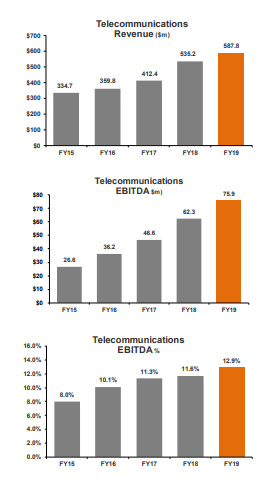

Telecommunications Revenue Rose $52.6 million YoY: The company’s telecommunications revenue rose by $52.6 million and a rise in the revenue relates to the customer connections and related services being performed for nbn co under various Activation & Assurance, Minor Projects and Design & Construction contracts. However, the rise was offset by the volume-related decline in fixed-line activities for other customers as well as in wireless operations. The following chart gives details of telecommunications revenue and EBITDA:

Telecommunications (Source: Company Reports)

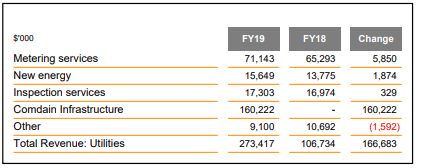

Significant Rise Witnessed in Utilities Revenue: The company’s utilities revenue rose by $166.7 million and a rise in the revenue was mainly because of inclusion of revenue from Comdain Infrastructure after its acquisition in the month of January 2019. It was added that the increases in revenue was also witnessed in metering services, new energy and inspection services. The following table provides an idea of the utilities revenue:

Utilities Revenue (Source: Company Reports)

The company stated that integration of Comdain Infrastructure has been going well and also ahead of schedule.

Dividend on Rise: Considering the company’s robust financial position, the Board of Directors continues to review capital management strategy in order to ensure that it remains effective when it comes to maximising the shareholder value. The Board declared an increased final dividend amounting to 5.5 cents per share (fully-franked), which takes total dividends with respect to FY19 to 9 cents per share (fully-franked) that is in line with the company’s progressive dividend policy approach. The company has a decent track record of consistent dividend payments with a CAGR of 56.5% over the last five years. The annual dividend yield of the company is about 4.1% on a five-year average basis (FY15-19). SSM’s dividends per share have been increasing since FY15 and, therefore, it can be said that the company is focusing on delivering returns to its shareholders. The growth trajectory in the dividends might attract dividend-seeking investors.

.png)

Dividend On Rise (Source: Company Reports)

What to Expect from SSM Moving Forward: The company is anticipating continued revenue and profit growth in FY20, however, it is subject to the continuation of prevailing market conditions. It was further added that FY20 would be characterised by full-year contribution from Comdain Infrastructure, partly offset by decreased earnings from the cessation of nbn D&C operations. The company’s earnings from FY20 onwards would be reported under AASB16 Leases and there are expectations of an uplift in EBITDA, arising from revised accounting treatment of the motor vehicle and property leases.

However, the priorities for FY20 primarily include securing the organic growth opportunities as and when they emerge throughout the existing operations and continuing to identify and assess further opportunities for market expansion and diversification. Additionally, there are expectations that the company’s less leveraged balance sheet as compared to the broader industry (evident from Debt/Equity ratio) might help the overall company in achieving long-term growth.

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: PE- based approach

PE- based approach (Source: Thomson Reuters), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters

.png)

Historical PE Band (Source: Thomson Reuters)

Stock Recommendation: The company’s stock has delivered a return of 10.17% in the span of previous six months while, on YTD basis, SSM witnessed a return of 49%. Between FY15- FY19, SSM’s total revenues have witnessed a CAGR growth of 19.99%, which reflects that the company is possessing respectable capabilities to garner revenues. During the same time span, its net income has encountered a CAGR growth of 43.71%. The company is possessing respectable operational capabilities and is evident from the CAGR growth of 16.50% in the span of FY15- FY19 in cash from operating activities. This, and revenue-generation capabilities, are expected to help the company in achieving overall growth moving forward. Based on the foregoing, we have valued the stock using a relative valuation method, i.e., Price to Earnings multiple, and arrived at a target price of lower double-digit growth (in % term). Hence, we give a “Buy” recommendation on the stock at the current market price of A$2.580 per share (down 0.769% on 31 October 2019).

SSM Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...