Kalkine has a fully transformed New Avatar.

Company Overview: Scentre Group Limited is the parent company of Scentre Group Trust 1 (SGT1), Scentre Group Trust 2 (SGT2) and Scentre Group Trust 3 (SGT3). The principal activities of the Company include the ownership, development, design, construction, asset management, leasing and marketing activities with respect to its Australian and New Zealand portfolio of retail properties. Its segments include Property investments segment, which includes net property income from shopping centers, and Property and project management segment, which includes external fee income from third parties, primarily property management and development fees, and associated business expenses. The Company manages, develops and has an ownership interest in Westfield branded shopping centers in Australia and New Zealand. It manages every aspect of its portfolio, including from design, construction and development to leasing, management and marketing.

.png)

SCG Details

Understanding of Key Growth Catalysts: Scentre Group (ASX: SCG) is a large-cap company in the REIT stock with the market capitalisation of circa $19.78 Bn as of 6 June 2019. It is the owner and operator of Westfield in Australia and New Zealand. Its portfolio included 41 Westfield Living Centres which are spread throughout Australia and New Zealand as at 31 December 2018 and the company’s ownership interests have been valued at $39.1 billion. Scentre Group owns 16 of top 25 centres in Australia and 4 of the top 5 centres in New Zealand. As per the report, over 35% of SCG’s portfolio garners annual retail sales of more than $1 billion and over 80% generates annual retail sales of over $500 million and, as a result, it looks like that the company might achieve decent growth momentum in the long-term. The company’s portfolio has been more than 99% leased for over 20 years and had witnessed over 55 years of continuous comparable net income growth. SCG has a vertically integrated operating platform and also has proven capability with respect to development, design, construction, leasing and management, with current and future development activity in excess of $3.7 billion. Thus, it can be said that the company’s future looks quite promising.

For the year ended December 31, 2018, 99% of rental income from the portfolio was derived from the contracted base rents while remaining 1% of rental income was directly related to the retailer sales. The group’s financial performance for year ended December 31, 2018 was strong and the funds from operations (or FFO) amounted to $1.3 billion which equates 25.24 cents per security and reflects a rise of 3.9% on Y-o-Y basis while the distribution amounted to 22.16 cents per security which implies an increase of 2%. Fundamentally, the stock looks in a decent position with a net margin of 87.1% and ROE of 9.9% in CY18. At CMP of $3.790, the stock of the SCG is trading at P/E multiple 10.90x of CY19E EPS. By looking at its unrivalled access to the potential customers, diverse range of brands, plans to repay the debt, and maintaining dividend pay-out ratio more than 85%, we have valued the stock using two Relative Valuation methods P/E, and EV/EBITDA multiple and arrived at the target price in the range of $4.3 to $4.4 (single digit upside (%)). Key risks: changing rules and regulation in Australia, intense competition, property ownership risks, property management and development risks, and adverse macro-economic conditions such as increase wages in Australia, etc.

.png)

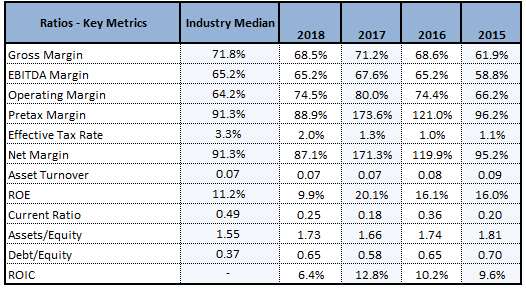

Key Financial Metrics (Source: Company Reports, Thomson Reuters), * 6 months to 31 December 2014

Top 10 Shareholders: The following table gives the broader picture of SCG’s top 10 shareholders:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Decent Key Metrics Amidst Certain Challenges: The company had posted average RoE and ROIC of 14.6% and 9.0%, respectively in the past 5 years with debt-to-equity ratio below 1.0x over the said period of time which represents that SCG is generating decent returns for the shareholders and focuses towards the repayment of debt. In CY18, the current ratio of Scentre Group stood at 0.25x, implying a rise of 38.2% on the YoY basis, which reflects its better liquidity position to address the short-term obligations have improved.

The company’s top line had witnessed a CAGR growth of 5.04% in the span of five years (CY14- CY18) which can be considered at decent levels and reflects its revenue-generation capabilities. The revenue-generation capabilities coupled with the improved in the company’s liquidity position might help the company in witnessing growth moving forward.

Key Metrics (Source: Thomson Reuters)

Pricing Of Senior Guaranteed Notes: Scentre Group had made an announcement that they have priced €500 million (or $800 million) of ten year fixed rate guaranteed notes which are having a coupon of 1.45% under Euro Medium Term Note Programme. The company added that the proceeds of the issue would be utilised towards the repayment of borrowings under SCG’s revolving credit facilities as well as for the general corporate purposes.

Also, the company had made an announcement that they have been assigned an “A Stable” credit rating from Fitch. The company’s top management had stated that this new rating from Fitch recognises SCG’s premier asset portfolio and the unique operating platform as well as its stability of income and robust financial position.

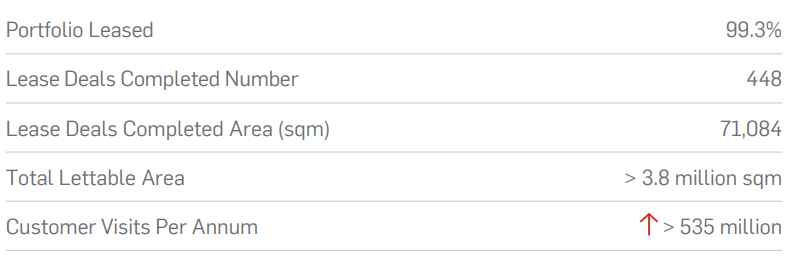

Understanding SCG’s 1st Quarter Operating Update: The management of Scentre Group had stated that the customer visitation had been growing during the quarter ended March 2019 which is being supported by the strong focus on customer experience. The company stated that it has been witnessing customer visitation of over 535 million visits annually and this continued to grow during the first quarter. The following picture gives an overview of the company’s operating performance:

Operating Performance (Source: Company Reports)

With respect to Development activity, the company added that Westfield Newmarket development is progressing well, and the staged openings are expected to commence in early Q3 CY19. Coming to the active project i.e. Westfield Newmarket, NZ, the project cost has been defined as NZ$790 million while the SCG’s share happens to be NZ$400 million. This project is expected to be wrapped up by Q4 CY19.

Introduction of New Joint Venture Partner: Scentre Group had made an announcement that the Perron Group would be a new 50% joint venture partner in Westfield Burwood in Sydney. Perron Group would be paying $575 million for its interest, which represents a 4.1% premium to SCG’s book value at December 31, 2018. The top management of Scentre Group had reflected favorable views with regards to extending the long-standing relationship with Perron Group into Westfield Burwood. They added that the proceeds will provide the group with further capital in order to pursue the strategic objectives of creating long-term value for the securityholders.

The proceeds, as a result of the transaction, would initially be utilised towards the repayment of debt. The transaction is anticipated to be dilutive to FFO per security in 2019 by around 0.2 cents per security. We expect that the reduction in debt might help in making the SCG’s balance sheet more attractive which might support in delivering long-term business objectives. Also, the forecast distribution for 2019 happens to be unchanged at 22.60 cents per security.

Decent Capital Management: Scentre Group’s distributions for the year ended December 31, 2018 amounted to 22.16 cents per stapled security which equates to the pay-out ratio of 87.8% of FFO that can be considered at respectable levels. The interim dividend which was paid on August 31, 2018 was 11.08 cents per stapled security of which distribution in respect of a Scentre Group Trust 1 unit and Scentre Group Trust 2 unit amounted to 3.34 and 7.74 cents per stapled security, respectively. However, final dividend in respect of Scentre Group earnings which has been paid on February 28, 2019 amounted to 11.08 cents per stapled security which comprises dividend with respect to Scentre Group Limited share of 2.96 cents per stapled security. Also, it comprised distribution with respect to Scentre Group Trust 1 unit, Trust 2 unit and Trust 3 unit of 3.40, 4.60 and 0.12 cents per stapled security, respectively. The company assesses the adequacy of capital requirements, cost of capital and gearing (i.e. debt/equity mix) as part of the broader strategic plan. It also reviews the capital structure in order to ensure sufficient funds and financing facilities. However, it reviews to also ensure that the dividends/distributions to the members are maintained within stated distribution policy and it also tries that the financing facilities for the unforeseen contingencies are maintained.

What To Expect From Scentre Group Moving Forward: As per the annual report for 2018, Scentre Group forecasts the growth in FFO for 12 months ending 31 December 2019 of around 3%. It also stated that the distribution for 2019 is expected to be 22.60 cents per security. The long-term view of the company’s top management is positive, mainly due to its leading position with respect to the sector and the management’s focus towards adaption to the constantly evolving retail landscape and delivering the superior customer experience that helps in driving strong visitation and customer advocacy.

The company stated that it commenced the redevelopment of Westfield Newmarket in Auckland in 2018 and it is on track to complete this in late 2019. The company seeks to manage the capital requirements to maximise the value to members via the mix of debt and equity funding. It also ensures that the entities of group comply with the capital and distribution requirements of their constitutions and/or trust deeds and with the capital requirements of the relevant regulatory authorities. Also, the group ensures that its entities maintain strong investment grade credit ratings as well as continue to operate as the going concerns.

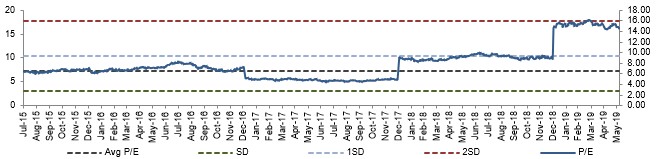

Historical PE band (Source: Company Reports)

Stock Recommendation: The stock of Scentre Group had witnessed a fall of 5.82% in the span of previous six months and, in the time frame of past three months, it had fallen 5.10% and, as a result, it is offering a decent opportunity to make an entry. The statutory profit for the year ended December 2018 amounted to $2.3 billion, which includes a revaluation uplift that amounted to $1.1 billion. The company had total assets amounting to $39.1 billion and its assets under management stood at $54.2 billion.

The company’s annual dividend yield, as per ASX, stood at 5.96% which can be considered at respectable levels and this might attract the attention of market players moving forward. By looking at its unrivalled access to the potential customers, diverse range of brands, plans to repay the debt, and maintaining dividend pay-out ratio more than 85%, we have valued the stock using two Relative Valuation methods P/E, and EV/EBITDA multiple and arrived at the target price in the range of $4.3 to $4.4 (single digit upside (%)). Given the backdrop of aforesaid parameters and looking at current trading level, we are positive on the stock and expect that it might witness growth in the long run. Hence, we give a “Buy” recommendation on the stock at the current market price of A$3.790 per share (up 1.882% on 6 June 2019).

SCG Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...