Kalkine has a fully transformed New Avatar.

Company Overview - Scentre Group manages, develops and has an ownership interest in Westfield branded shopping centers in Australia and New Zealand. The Company has a portfolio of approximately 38 Westfield shopping centers in all metropolitan cities and some regional centers. The Australian portfolio has around 11,135 retail outlets in 3.4 million square meters of retail space. The Company has an interest in nine centers with over 1,400 retail outlets in excess of 379,000 square meters of retail space. Its Westfield Chatswood is located in the affluent Northern Suburbs of Sydney, approximately 11 kilometers from the CBD. Westfield North Lakes is located 25 kilometers north of Brisbane’s CBD. Its Westfield Kotara is located six kilometers south-west of Newcastle’s CBD.

Analysis – Scentre Group’s portfolio of shopping malls enjoy a dominant position in premium locations in Australia and New Zealand. This enables them to capture a high share of wallet in their catchment area, providing a disincentive to new competition. Network benefits from the larger format malls include established transport links and a critical, mass of retailers which both serve to drive foot traffic. Scentre Group’s premium malls should benefit from solid ongoing tenant demand reflecting premium positioning, higher sales productivity and exposure to higher income demographics.

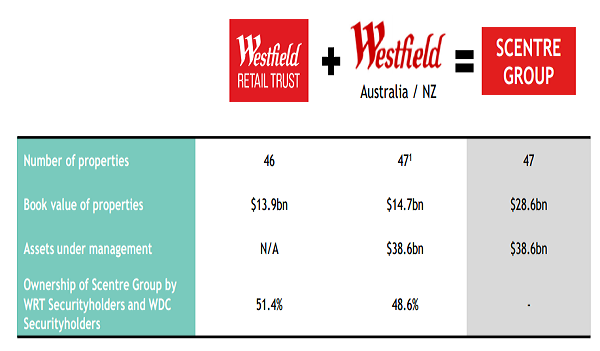

Scentre Group Formation (Source - Company Reports)

Scentre Group was created by combining the Australian assets of Westfield Group with those of Westfield Retail Trust in mid – 2014. Scentre Group’s portfolio of shopping malls was a beneficiary of strong compound annual growth in Australian retail sales in the 2000s. High sales growth strengthened the negotiating position of landlords enabling mall owners to lock in tenants to lease terms that incorporate relatively high annual escalations. This is evident in Scentre Group’s portfolio with the standard specialty lease containing annual escalations of consumer price index or CPI plus 2%. The increasing tenant rental burden is illustrated by higher occupancy costs for Scentre Group’s specialty tenants which have gradually increased from 15.3% of sales in December 2004 to 19.2% as at December 2013.

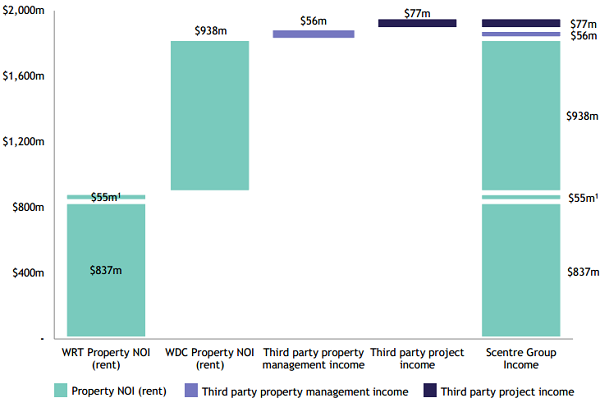

Income Forecast (Source - Company Reports)

Scentre Group’s other growth source is from development activities. The firm has identified a pipeline of AUD 3 billion (Scentre Group share is AUD 2 billion) of future development opportunities during the next five to seven years on the existing property portfolio. Barring a severe downturn in retail we expect this pipeline to be delivered with Scentre Group likely to capture development spreads of between 100 to 200 basis points. We believe Scentre Group is well positioned to continue growing earnings and distributions. However structural changes in the retail sales environment could pressure rental growth rates to below historic averages.

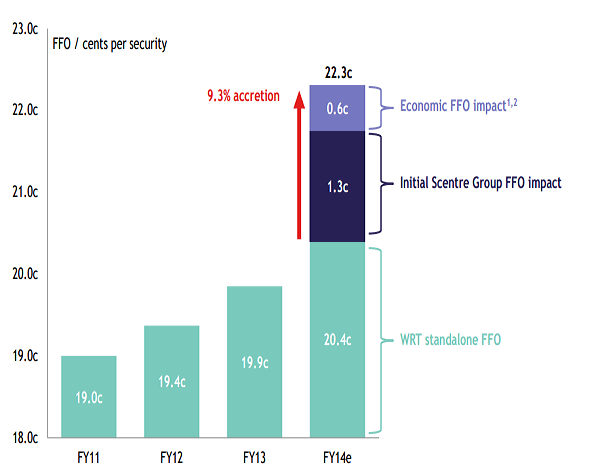

Expected Earnings Accretion (Source - Company Reports)

The company’s long term development pipeline to reinvigorate and upsize its malls is also a disincentive for new competition. Redevelopment of existing malls refreshes and improves the customer experience, drives foot traffic , increase share of the retail wallet in the catchment area and steals foot traffic from competitors. The combination of these factors strengthens the landlord’s ability to extract rent increases. Despite online retail pressure, Scentre Group’s large and well positioned malls will remain an attractive distribution channel for retailers as we expect there will be ongoing demand by customers to touch, feel and discuss items before purchasing, particularly at its well-located inner city shopping malls.

SCG Chart (Source - Thomson Reuters)

Scentre Group’s larger format malls with a high number of customer attracting anchor tenants benefit from efficient scale given they capture a high share of foot traffic in their catchment areas providing a disincentive to new competition. Scentre Group’s malls are largely located in built up areas, where there is often a shortage of land for alternate development. Scentre group also benefits from the network effect with customers more attracted to malls with a large choice of retailers than smaller malls or strips. The resulting foot traffic feeds demand by retailers for space in Scentre Group’s shopping centres.

The development pipeline is expected to continue to generate gross rental yields of 7.5% to 8.0%. If we use the low point of this range and combine it with a 40% gearing and a 6% cost of debt we arrive at a return on new invested capital or ROIC of 8.5%. We also expect long term asset value appreciation of at least 2% which collectively gives rise to a long term ROIC of 10.5%. It would be very difficult and more expensive for competitors to disrupt Scentre Group’s local monopolies on retail traffic. In the longer term ( three years plus), we believe the inner suburban location of many of Scentre Group’s assets will result in long term growth in foot traffic aided in part by the positive effects of population growth, affluence and rising inner city/suburban housing density. We expect the superior quality of Scentre Group’s assets will continue to drive foot traffic particularly the more affluent consumer cohort who covet and more importantly are prepared to pay for the retail experience.

Scentre Group is in good financial health with an interest coverage ratio of 3.3 times. Proforma gearing is about 37% but will decline to between 30% and 35% when the firm starts selling part shares in assets. With Scentre Group’s malls consistently maintaining an occupancy rate in excess of 99% during the past 10 years the assets have demonstrated tenant demand which we envisage will persist going forward. Operating earnings before interest are relatively predictable in the medium term with more than 98% of total rental income derived from minimum contracted base rent. Earnings stability is further aided by a long weighted average lease expiry of about seven years.

The capital structure of the firm consists exclusively of debt and equity. The firm has the highest grade credit rating of all the listed Australian REIT’s which should enable it to obtain funding from a diverse range sources when it renegotiates all its debt facilities in mid-2014.

As per our analysis, SCG owns the best quality retail portfolio in Australia and New Zealand with 47 assets worth around A$29.3bn. Many investors prefer the pure regional and asset class focus of SCG, which is now actively and internally managed as well. We put a BUY recommendation on the stock at the current price of $3.55.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...