Company Overview - Santos Limited is an oil and gas producer. The Company's principal activity is the exploration for, and development, production, transportation and marketing of, hydrocarbons. It has an Asian portfolio, with a focus on three core countries: Indonesia, Vietnam and Papua New Guinea. It has interests in four liquid natural gas (LNG) projects, comprising GLNG, PNG LNG, Darwin LNG and Bonaparte LNG. Its business units include Asia Pacific, Eastern Australia, GLNG, and Western Australia and Northern Territory. The Asia Pacific unit includes operations in Indonesia, Papua New Guinea, Vietnam, India, Malaysia and Bangladesh. It is a producer of natural gas, gas liquids and crude oil in eastern Australia. It sells gas to domestic retailers and industry while gas liquids and crude oil are sold in the domestic and export markets. It produces domestic natural gas in Western Australia and is also a producer of gas liquids and crude oil. It also has an interest in the Bayu-Undan/Darwin LNG project.

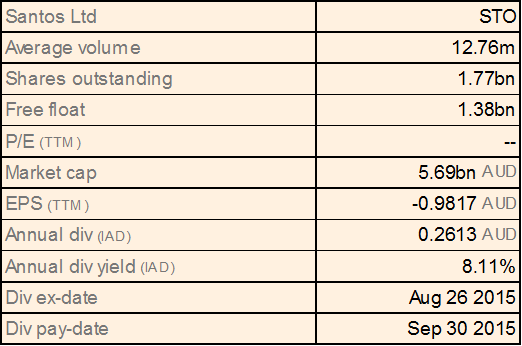

STO Dividend Details

Delivered solid production driven by LNG: Santos Ltd (ASX: STO) reported an overall production increase of 7% year on year (yoy) to 57.7 mmboe during fiscal year of 2015 which is a record annual production from 2007, and on track with the group’s issued guidance range of 57 mmboe to 59 mmboe. But Santos sales revenues plunged 20% yoy to $3.246 billion in FY15 as the average realized oil prices fell by 37% yoy to $71.44/bbl. On the other hand, STO has been trying to offset this pressure to a certain extent and tried cutting its capital expenditure by 54% in fiscal year of 2015 against prior corresponding period (pcp).

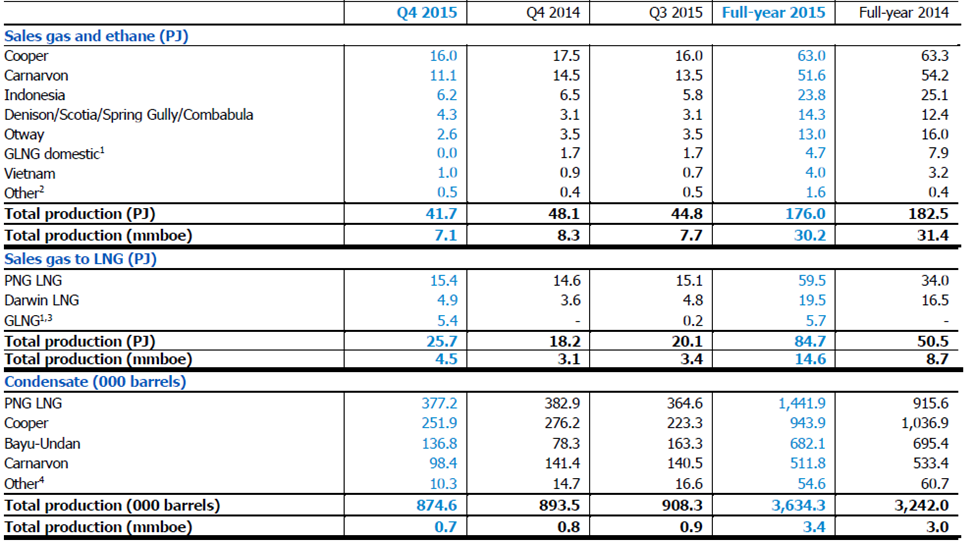

Production performance in fourth quarter and full year of 2015 (Source: Company Reports)

LNG production enhanced to 14.6 mmboe in fiscal year of 2015, driven by higher PNG LNG production as well as contribution from GLNG. The group’s share of sales gas production from GLNG’s upstream fields reached 5.4 PJ during the fourth quarter 2015, which is 218% rise against the third quarter of 2015, on the back of ramp up of LNG train 1. Accordingly, Train 1 produced 544,000 tonnes of LNG during the fourth quarter and delivered daily LNG production rates of greater than 10% above the nameplate capacity. STO started work of the second LNG train and estimates to deliver the first LNG from the second train by second quarter of 2016. The group also entered into an agreement with AGL Energy to buy 254 petajoules of gas for supplying its GLNG project, wherein the gas would be delivered at Wallumbilla for a duration of 11 years starting from January of next year. The gas would be sourced from coal seam gas fields in Queensland while the pricing is as per the oil-linked formula. As per the Darwin LNG highlights, the project also reported a decent performance during the quarter and delivered an annual LNG production of 3.8 million tonnes. Santos gross gas production improved 7% yoy to 57.0 PJ driven by improved Darwin LNG capacity utilization. Santos shipped around 15 LNG cargoes from Darwin LNG project during the fourth quarter of 2015 and delivered over 58 cargoes during the full year of 2015. Santos also enhanced its net condensate production by 75% yoy to 136,800 barrels in Darwin LNG project during the fourth quarter of 2015 while the net LPG production improved by 60% yoy to 7,500 tonnes even though the yields were decreasing.

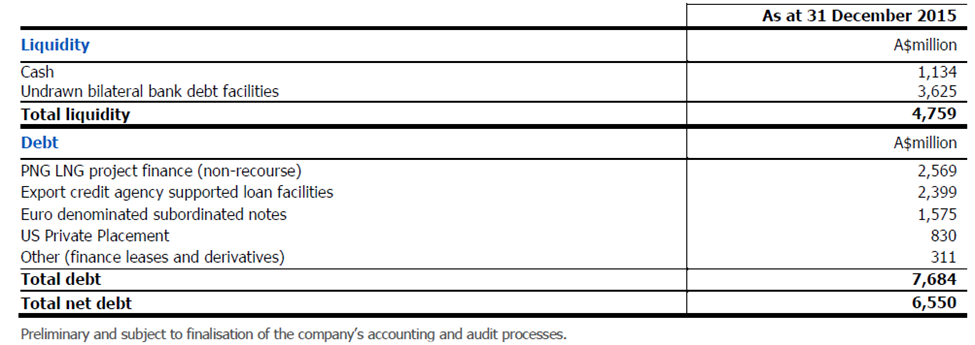

Strengthening capital position via capital raising and sale of its assets: Santos is strengthening its balance sheet to withstand the impact of ongoing commodity prices pressure. Therefore, the group declared a $3.5 billion of capital initiatives during November 2015 to enhance its balance sheet as well as decrease its debt. Accordingly, STO finished the equity issuances via its placement and entitlement offer and received these proceeds in the fourth quarter of 2015. Santos estimated to get $520 million of cash from its Kipper gas asset sale to Mitsui E&P Australia during the first quarter of 2016. The group reported a cash and committed undrawn debt facilities of $4.8 billion as of December 2015. Santos repaid over $2 billion of debt in the second half of 2015 and has a net debt position of $6.55 billion as of December 2015, which includes $7.68 billion of gross debt and derivatives less cash of $1.13 billion. STO does not have any major debt maturities till 2019 while its Euro denominated subordinated notes would mature by 2070, with the group having the option to redeem its first call by September 2017. Meanwhile, Credit rating agency, Standard and Poor’s ratings Services (S&P) issued a credit rating of BBB- for the group’s long-term senior unsecured credit rating as compared to its earlier BBB credit; thus, STO still maintains its investment grade credit rating.

Capital position as of December 2015 (Source: Company Reports)

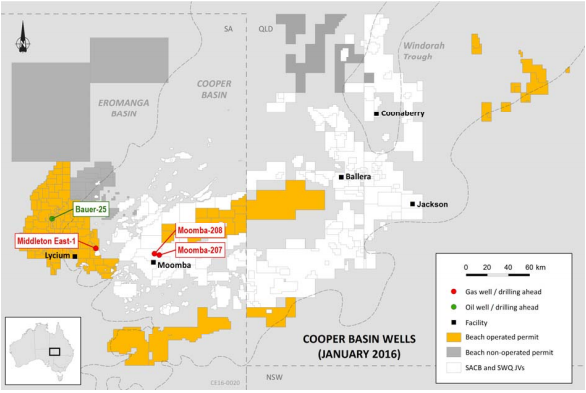

Cooper Basin highlights: Santos production from the Cooper Basin fell by 9% to 16.0 PJ during the fourth quarter of 2015 as compared to the same period of last year due to decrease in development activity as well as decrease in natural fields. However, this decrease was partly offset by the less downtime and lower fuel, flare and vent during the period. The group had drilled, cased and suspended around 12 new gas wells in the fourth quarter of 2015, while one well drilling was ahead than planned as of December 2015. Santos delivered the first gas to GLNG under the Horizon contract during starting of October 2015. Recently, the operator of Cooper and Eromanga basins development at South Australian gas project, Beach Energy reported that their six?well infill development drilling program was finished in the Moomba North Field, which were targeted to develop booked reserves at the Toolachee, Daralingie and Patchawarra formations. Santos has 66.6% stake in this project while Beach and Origin Energy have 20.2% and 13.19%, respectively.

Cooper Basin Wells (Source: Company Reports)

Beach Energy planned a phased approach in the drilling program which comprised the drilling of up to 26 new wells in the area, wherein six wells were already drilled in 2014. Beach applied the outcomes from 2014 program to its present drilling program which included optimizing well designs and enhancing well achievements. In January, Beach finished the final two wells of its present drilling program. These two wells, Moomba?207 and Moomba?208 had intersected gas pay on track with pre?drill estimates. Beach delivered a successful drilling program as all the six wells from its present program were cased and suspended as future producers. On the other side, Condensate production fell 9% while LPG production declined by 15% on the back of decrease in raw gas production. As per the Crude oil highlights, the Crude production fell by 9% during the fourth quarter as compared to the third quarter impacted by the decrease in development activity coupled with natural field decline. Merrimelia 64, a new horizontal oil well, was drilled, cased and suspended during the fourth quarter while McKinlay 10, the second well drilling is on track well before the schedule as of December 2015.

Outstanding dividend yield: STO stock plunged over 51.48% (as of February 16, 2016) in the last one year as the ongoing commodity prices decline continued to hurt its average realized oil prices which fell over 33% to US$44 per barrel during the fourth quarter of 2015, and consequently the group’s sales revenues fell by 24% to $828 million in the quarter against pcp. On the other hand, Santos had focused to decrease its production costs and accordingly achieved a 10% decrease in production costs per barrel during fiscal year of 2015 as compared to its pcp. STO also heavily cut its capital expenditure and reported a 54% decrease in FY15 against comparable previous year, and 8% lower than its estimated fiscal year of 2015 guidance (excluding capitalized interest). The group is seeking to build long-term contracts for its GLNG project as the project promises strong long term prospects.

Moreover, the heavy correction in the stock placed STO at attractive valuations and investors seeking for long term value stocks could consider adding Santos to their portfolio. The shares of Santos had recovered by 29.6% in the last four weeks (as of February 16, 2016) and we believe that the positive momentum in the stock would be witnessed in future. STO also has an outstanding dividend yield. Based on the foregoing, we reiterate our “BUY” recommendation on the stock at the current price of $3.29, ahead of its detailed full year results announcement to be made on February 19, 2016.

STO Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...