Kalkine has a fully transformed New Avatar.

Company Overview: rhipe Limited (rhipe), formerly FRR Corporation Limited, is engaged in the wholesale of subscription software licenses to various technology service provider resellers. In addition, the Company provides value added consulting and support to assist service provider resellers transition their own clients to cloud and subscription centric business environments. It provides cloud licensing and solutions for its software vendors across the Asia Pacific region. Its divisions are focused on cloud licensing (private, public and hybrid), cloud solutions (consulting services), and cloud operations (billing, provisioning, support, marketing). It offers Microsoft Indirect Cloud Solutions Program (CSP) program for Australia. Its program allows the Company to wholesale Microsoft's public cloud offerings, such as Office365, Azure and Enterprise Mobility Suite (EMS) to rhipe's reseller channel on a monthly subscription pay-as-you-use basis.

.png)

RHP Details

Microsoft Continues to be the Largest Contributor to Growth: Rhipe Limited (ASX: RHP) is engaged in the provision of subscription software licenses to IT service provider resellers in the Asia Pacific region. The company is one of the leading providers of monthly Pay-As-You-Go (PAYG) cloud software license subscriptions and has established strong momentum in the market. The company’s Platform for Recurring Subscription Management (PRISM) is used by multiple software vendors, including Microsoft, Citrix, Symantec, VMWare, etc., to boost the consumption of their cloud license programs, cloud provisioning, billing and reporting for data centres, and managing end-user customer licenses. During the year, the company was focused on aligning its business operations with the transitions happening in the IT industry. The business comprises of three key divisions – Cloud Licensing, Cloud Solutions, and Cloud Operations, and possesses its own intellectual property in the form of PRISM, described above.

As the company added the public cloud business on its platform in FY16, it was appointed as an Indirect Cloud Solutions Provider (CSP) to Microsoft, for sourcing resellers for the latter’s key public cloud products, including Microsoft Office 365 and Microsoft Azure. Growth in FY19 was supported by sales across the above-mentioned products, with Office 365 sales increasing by ~80% and Azure sales growing by ~190%. Total licensing sales from the products accounted for 60% of the sales growth in FY19. By October 2019, monthly consumption of office365 seats increased to more than 516,000 seats, representing a year over year increase of 63%. In addition to the public cloud, the private cloud business has also been a contributor to growth. Private cloud licensing witnessed a y-o-y growth of 8% in sales across all markets..png)

Microsoft CSP O365 Seat Count (Source: Company Reports)

The company also expanded its solutions business, which provides value-added services through a consulting team. During the year, the company acquired Dynamics Business IT Solutions Pty Ltd to provide additional services to its reseller partners. The company’s support team comprised of around 135 employees at the end of FY19, as compared to 80 employees as on 30 June 2018.

While Microsoft accounted for a major chunk of the company’s licensing sales in FY19, the company will continue to invest in other vendors that have delivered higher sales growth in FY19, as compared to the prior corresponding year. Moreover, the company is also looking forward to investing and expanding its current portfolio of software vendors, for additional sales opportunities. The company is also focused on continuously refining the strategy concerning its consulting team, to be specially aligned with the products delivering promising results.

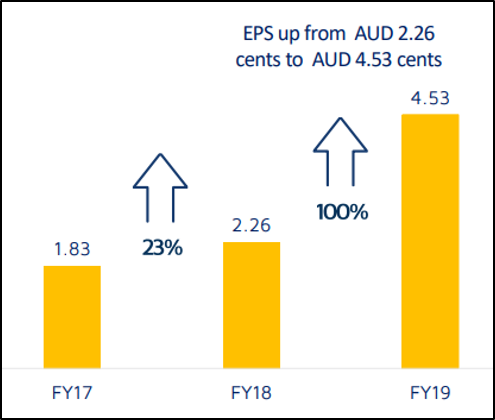

Over the four years covering FY15-FY19, the company reported sales CAGR of ~24.5%, with FY15 and FY19 sales amounting to $105 million and $252.5 million, respectively. Over the two years covering FY17–FY19, the company delivered substantial growth in shareholder returns, giving an EPS CAGR of 57.3%, with FY17 and FY19 EPS of 1.83 cents and 4.53 cents, respectively.

Shareholder Returns (Source: Company Reports)

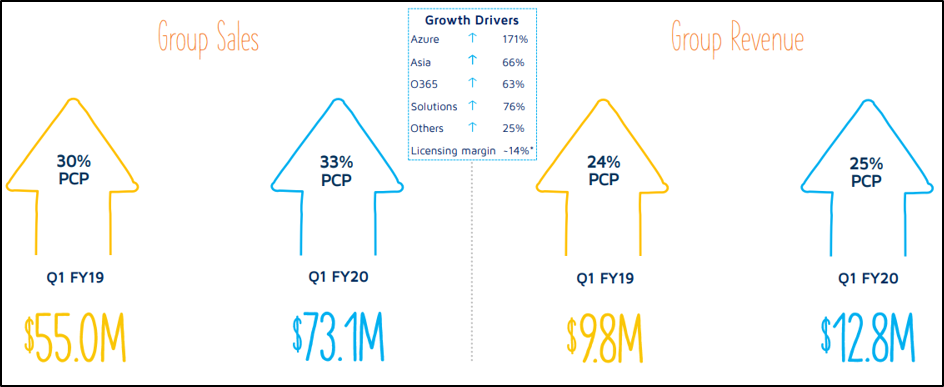

Q1FY20 Details: During the quarter ended 30 September 2019, group sales amounted to $73.1 million, up 33% on the prior corresponding period sales of $55.0 million. Group revenue for the quarter came in at $12.8 million, depicting 25% growth on prior corresponding quarter revenue of $9.8 million. Growth drivers in the descending order comprise – (a) Azure sales, that grew by 171% y-o-y, (b) Solutions business, delivering a growth of 76%, (c) Asia sales, that witnessed an increase of 66% on pcp, (d) O365 sales, up 63% on pcp, and (e) other businesses, that reported a growth rate of 25%.

Q1FY20 Results Highlights (Source: Company Reports)

Japan Joint Venture: The company entered into a joint venture agreement with Japan Business Systems Inc., to form rhipe Japan. The entity is jointly owned by rhipe and JBS, with percentage holdings of 80% and 20%, respectively. Since Japan is one of Microsoft’s largest markets, the JV provides RHP with significant headroom for growth. As per an announcement released in October 2019, rhipe Japan has already been appointed as an Indirect Cloud Solutions Provider by Microsoft Japan, as a result of significant growth delivered by the company between FY17 and FY19. In FY20, the company expects to invest an amount of ~$3 million in the joint venture, that will be allocated for delivering marketing, systems and enablement services to boost the growth of Microsoft Cloud Subscriptions across SMEs and expanding the JV’s workforce.

FY19 Highlights: During the year ended 30 June 2019, the company reported sales growth of 28%. The company has depicted a brilliant growth trajectory with continued upward movement in sales since FY15. Group revenue for the year amounted to $48.4 million, up 36% on pcp revenue of $35.6 million. Group operating profits improved significantly in comparison to FY18, to $12.8 million, up 65% on pcp. At the end of the year, the company had a cash balance of $25.5 million, representing an increase of $2.8 million on the previous year, after the distribution of dividends, continued investment in PRISM, and the acquisition of DBITS. To support the strong performance across the licensing business, the company incurred additional operating expenses of $6.6 million in comparison to the previous year, representing a y-o-y increase of 25%. The increase was driven by investment in front-office headcount to support strong sales and revenue growth.

As highlighted earlier, the company delivered a strong performance in FY19, especially on the back of robust licensing sales growth from Microsoft’s products. As a result, the company also formed a JV in Japan, that forms one of the largest markets for Microsoft, to boost sales and revenue growth in the future. Japan displays significant growth potential, with the cloud segment expected to grow at a 3- year CAGR of 25%. Apart from Microsoft, the company ensures that other vendors on the platform do not go unnoticed and has continued to make investments to drive further growth.

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 45.62% of the total shareholding. Tutus McDonagh Pty. Ltd. held the maximum number of shares with a percentage holding of 17.07%, followed by First Sentier Investors with a holding of 5.63%.

.png)

Top Ten Shareholders (Source: Thomson Reuters)

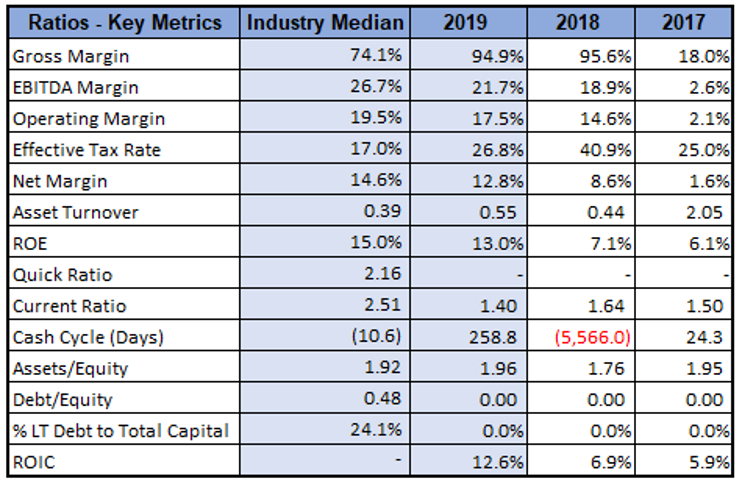

Key Metrics: In FY19, the company had a gross margin and EBITDA margin of 94.9% and 21.7%, respectively. While the gross margin stood substantially above the industry gross margin of 74.1%, EBITDA margin stood ahead of the previous year’s margin of 18.9%, depicting decent fundamentals. Net margin for the period came in at 12.8%, higher than the prior corresponding year margin of 8.6%, depicting improved profitability. Over the period covering FY17 – FY19, the company had zero debt, representing consistent financial stability in the business.

Key Metrics (Source: Thomson Reuters)

Outlook: The company has been delivering strong results and has continued the momentum into Q1 FY20, which reported decent growth in sales and revenue. In FY20, the company expects to report an operating profit amounting to $16 million, excluding the modification in market conditions or any geographical or vendor expansion initiatives. Including the forecasted cost of Japan JV during the year, operating profit for FY20 is expected to be $13 million. The company considers Japan to be a reservoir of returns for shareholders, comprising 5 times the number of small and medium businesses in Australia. However, the new market will require continuous focus and investment to be able to contribute to the company’s financial well-being.

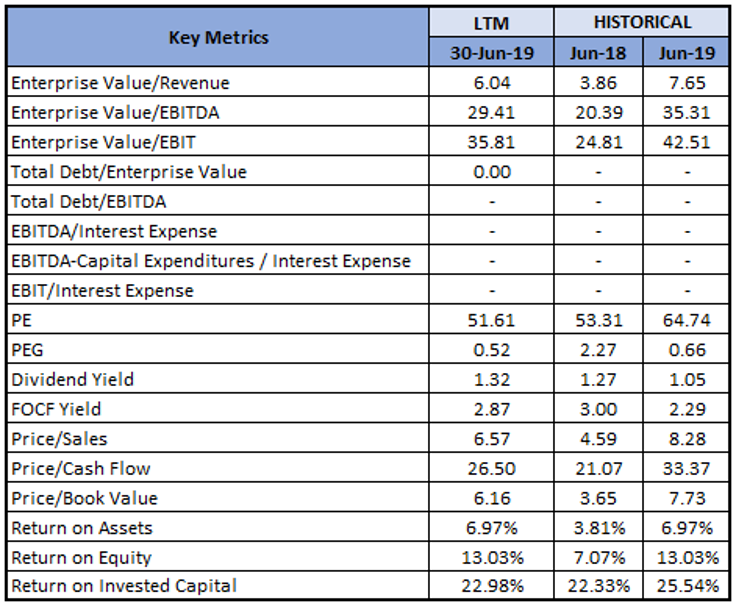

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies: EV/Sales Multiple Approach:.png)

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company delivered positive YTD returns of 10.68%. Currently, the stock is trading slightly below the average of its 52-weeks low and high of $1.285 and $3.120, respectively, indicating a decent opportunity for accumulation. During FY19, the company reported significant sales growth across Microsoft’s O365 and Azure products, with the momentum continuing in Q1 FY20. Despite several cash payments in the form of additional investment for PRISM, dividend distribution, etc., the company managed to increase its cash balance at the end of the period, keeping the business well-funded for future growth initiatives. The JV in Japan was a major initiative with respect to growth opportunities in terms of being one of Microsoft’s key markets and enhanced access to small and medium businesses as compared to Australia. We have valued the stock using EV/Sales based relative valuation method and for the purpose, we have considered the peer group - Superloop Ltd (ASX: SLC), Data#3 Ltd (ASX: DTL), and NEXTDC Ltd (ASX: NXT). As a result, we have arrived at a target price offering an upside of lower double-digit in percentage terms. Considering the robust sales performance in FY19, Q1FY20 trading update, enhanced business opportunities from the newly formed joint venture, decent cash position, and current trading levels, we recommend a “Buy” rating on the stock at a current market price of $2.190, down 3.947% on 24 January 2020.

RHP Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...