Kalkine has a fully transformed New Avatar.

Company Overview: Rhipe Limited (rhipe), formerly FRR Corporation Limited, is engaged in the wholesale of subscription software licenses to various technology service provider resellers. In addition, the Company provides value added consulting and support to assist service provider resellers transition their own clients to cloud and subscription centric business environments. It provides cloud licensing and solutions for its software vendors across the Asia Pacific region. Its divisions are focused on cloud licensing (private, public and hybrid), cloud solutions (consulting services), and cloud operations (billing, provisioning, support, marketing). It offers Microsoft Indirect Cloud Solutions Program (CSP) program for Australia. Its program allows the Company to wholesale Microsoft's public cloud offerings, such as Office365, Azure and Enterprise Mobility Suite (EMS) to rhipe's reseller channel on a monthly subscription pay-as-you-use basis.

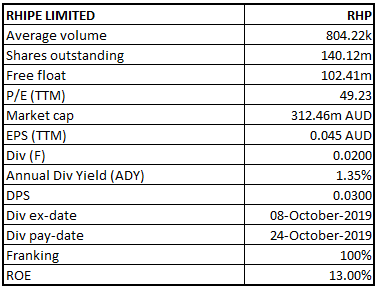

RHP Details

RHP Inks a Joint Venture Agreement in Japan: Rhipe Limited (ASX: RHP) is engaged in the sale and support of subscription software licenses to over 3,000 IT service provider resellers in the Asia Pacific region. Some of RHP’s key clients include Microsoft, VMWare, Citrix, Red Hat, Trend Micro, Veeam, Zimbra, and Symantec. During the financial year ended 30 June 2019, the company continued to invest in operations focused on the IT industry transition to the cloud business model. The period saw the integration of the company’s three business divisions including, Cloud Licensing, Cloud Solutions and Cloud Operations, to build an intellectual property in the form of Platform for Recurring Subscription Management (PRISM). During the year, the company reported a remarkable growth across all its key metrics. Revenue for the period stood at ~$48.36 million, representing an increase of 36% on prior corresponding year. Growth in revenue was driven by sales growth in the licensing business, along with the benefit arising out of a ‘strategic growth accelerator’ rebate received from a key software vendor. During the year, licensing revenue reported a growth rate of 34%. Reported EBITDA stood at $10.02 million, up 57% on prior corresponding period. Operating profit increased by 64% y-o-y, driven by robust growth in Licensing and Solutions businesses and management of the cost base. The trend continued in Q1FY20, with RHP witnessing decent growth across group sales and revenue.

One of the key recent developments in the business has been the joint venture agreement with Japan Business Systems Inc. for access into one of Microsoft’s largest markets with the cloud segment forecast to grow at a 3-year CAGR of 25%, starting from FY20. The company has so far completed the entity setup and capitalisation for the venture and has five staff in place, which is expected to grow in 2HFY20. The company estimates the cost associated with the joint venture to be $3.0 million in FY20.

Over a period of 5 years covering FY15 – FY19, the company reported sales CAGR of 24.5%, with FY15 and FY19 sales amounting to $105 million and $252.5 million. The highest growth in sales was reported in FY19 at 28.4%, followed by FY18, with a growth rate of 25.2%. In terms of value, FY19 sales witnessed a rise of $56 million as compared to $40 million in FY18, driven by the areas of the business which attracted material investments, notably the public cloud business with Microsoft CSP including Microsoft Officce365 and Azure. Sales of these products have witnessed remarkable uplift in FY18 and FY19, with a growth rate of 130% and 99%, respectively. Moreover, the company’s private cloud business also continued to grow during the period, predominantly in Asian operations. Local private cloud sales of Microsoft Licenses increased by 22% y-o-y. Apart from Microsoft, sales from other vendors have also reported decent growth with a y-o-y increase of ~19%, as compared to 15% in FY18.

Group Sales (Source: Company Reports)

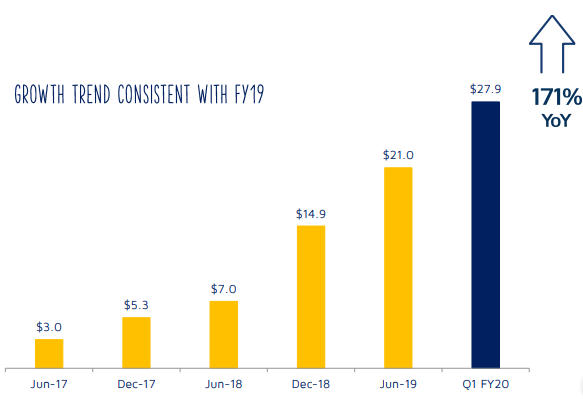

Q1FY20 Trading Update: During the quarter ended 30 September 2019, the company reported group sales amounting to $73.1 million, up 33% on prior corresponding period. Operating profit for the quarter came in at $2.9 million, up 6% on pcp. Microsoft CSP Azure Annual Run Rate (ARR) Sales reported a whopping increase of 171% on y-o-y basis, with sales amounting to $27.9 million.

Microsoft CSP Azure ARR Sales (Source: Company Reports)

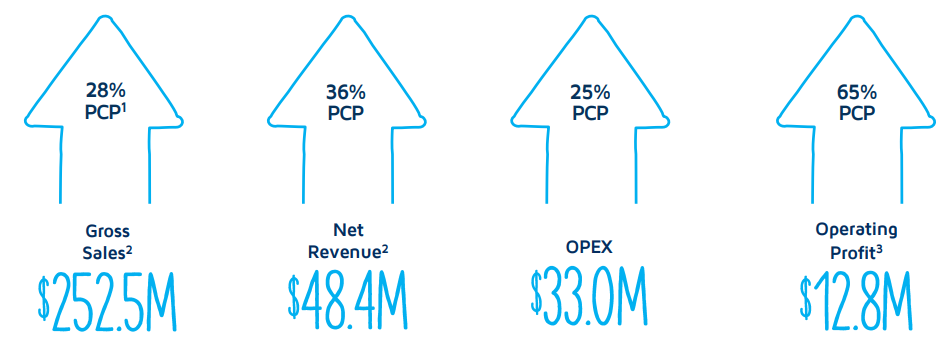

FY19 Financial Highlights: During the year ended 30 June 2019, group sales amounted to $252.5 million, up 28% on prior corresponding period. Net revenue came in at $48.4 million, up by 36% over revenue reported in prior corresponding period (pcp). Operating expenditure for the year stood at $33.0 million, representing an increase of 25% on pcp. Operating profit stood at $12.8 million, up 65% on the previous year. Reported EBITDA and profit after tax came in at $10.0 million and $6.2 million, representing growth of 56% and 103%, respectively.

FY19 Key Metrics (Source: Company Reports)

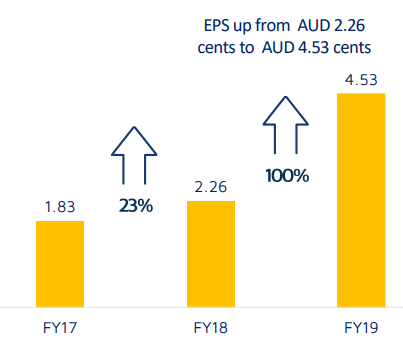

During the year, the company declared a fully franked final dividend of AUD 2 cents per share, paid on 24 October 2019. The period also saw a buyback of 1.7 million shares at a value of $2.1 million and an average price of $1.19 per share. In FY19, earnings per share went up by ~100%, with FY18 and FY19 EPS amounting to 2.26 cents and 4.53 cents, respectively. This represented a significant improvement in shareholder returns when compared with the growth rate of 23% in FY18.

Shareholder Returns (Source: Company Reports)

Acquisitions: In February 2019, the company acquired Dynamic Business IT Solutions (DBITS), in order to broaden the services offered to its ecosystem of resellers and to further enhance its expertise in Microsoft software offerings. In August 2019, the company acquired 100% capital of Network2Share Pty Limited, which developed a user-friendly encryption product, SmartEncrypt, which was to be bundled with Microsoft Office365, Microsoft Azure, and other vendor software licenses to enhance the customer experience. Recently, the company has entered into a joint venture agreement with Japan Business Systems Inc., to launch its indirect business in Japan.

As the business moves forward, the company has provided a strategy revolving around four major business factors including, partner, customers, people and culture. To expand its geographical footprints, the company is looking forward to cement and grow partner of choice market position along with continued expansion in other APAC markets. It is also looking forward to expanding its portfolio of solutions with innovative, subscription-based cloud and software solutions. To offer technical support for new vendors and partners, the company is aiming at continuous expansion across value-added services including, marketing-as-a-Service, Support-as-a-Service and Consulting-as-a-Service. Moreover, it is striving to provide a greater digital experience to customers.

Shareholding Update: The company recently updated that the voting power of Mitsubishi UFJ Financial Group, Inc. increased from 6.45% to 7.47%. The company also announced an increase in the voting power of First Sentier Investors Holdings Pty Limited, from 6.45% to 7.69%.

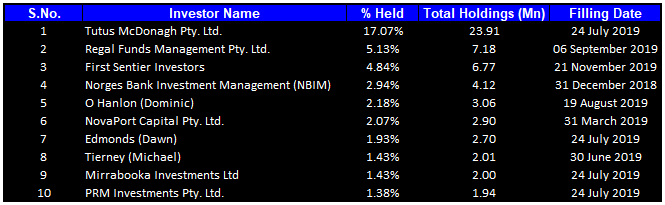

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 40.39% of the total shareholding. Tutus McDonagh Pty. Ltd. held the maximum number of shares with a percentage holding of 17.07%, followed by Regal Funds Management Pty. Ltd. with a holding of 5.13%.

Top Ten Shareholders (Source: Thomson Reuters)

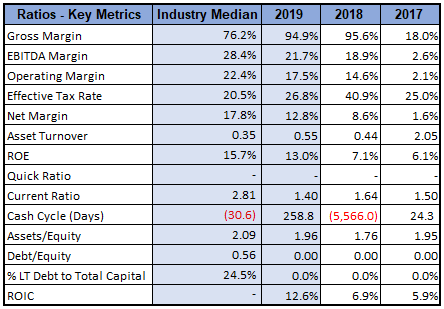

Key Metrics: During the year ended 30 June 2019, the company had a gross margin of 94.9%, higher than the industry median of 76.2%. The margin also stood higher in comparison to the prior corresponding year’s gross margin of 95.6%. EBITDA margin for FY19 stood at 21.7%, higher than 18.9% in FY18. Net margin of the company also stood better than prior corresponding year at 12.8%. During the year, the company did not report any debt. The company’s debt-to-equity ratio was zero as compared to the industry median of 0.56x, representing greater financial stability in comparison to peers.

Key Metrics (Source: Thomson Reuters)

Outlook: Going forward, the company will continue to nurture its relationship with key software and technological partners on the platform. It will continue to explore opportunities for expansion into its key markets including, Australia, New Zealand, Singapore, Thailand, Malaysia, etc. In addition, the company is also looking to expand its presence in the Japanese market and has taken a huge step forward in the form of a joint venture agreement, which will boost earnings growth in FY20. The deal is an 80:20 relationship between the parties, with RHP holding 80% of the capital. Japan represents an excellent opportunity for the business being one of Microsoft’s largest markets. Moreover, the SME market in Japan is estimated to be 5.0x size of the Australia market. In FY20, the company expects to report an operating profit of $16 million, excluding any changes in market conditions or major expansion initiatives. Including the estimated Japan JV cost of $3.0 million, operating profit is expected to be ~$13 million.

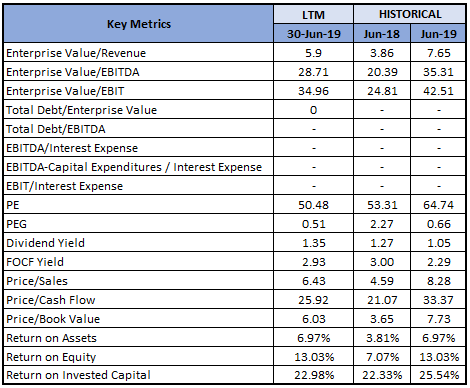

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

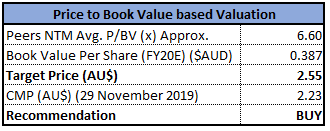

Method 1: Price/Book Value Multiple Approach

Price/Book Value Based Valuation (Source: Thomson Reuters)

Method 2: Price/Cash Flow Multiple Approach:

.png)

Price/Cash Flow Based Valuation (Source: Thomson Reuters)

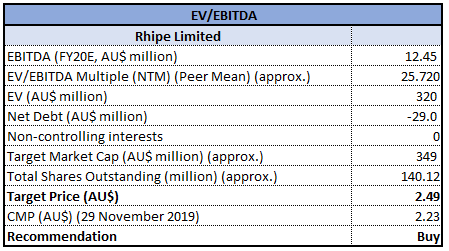

Method 3: EV/EBITDA Multiple Approach:

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock of the company generated negative returns of 21.75% and 12.55% over a period of one month and three months, respectively. In FY19, the company continued to deliver decent growth across key financial metrics. The company reported growth across geographies, products and licensing programs throughout FY19. Cash at the end of the year amounted to $25.5 million, up by $3 million despite a share buyback of $2.1 million, dividend payment of $2.7 million and a cash payment of $3 million for the acquisition of Dynamics Business IT Solutions Pty Ltd. As per the trading update for Q1FY20, the company continued its growth trajectory and even reported a key achievement by signing a JV agreement in Japan. Considering the financial performance in FY19, recent acquisitions for business development, growth strategy and a decent operating profit guidance for FY20, we have valued the stock using three relative valuation methods, i.e., Price/Book Value Multiple, Price/Cash Flow Multiple and EV/EBITDA Multiple, and arrived at the target price of lower double-digit growth (in % term). Hence, we recommend a “Buy” rating on the stock at the current market price of $2.230 on 29 November 2019.

RHP Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...