Kalkine has a fully transformed New Avatar.

I. Sector Landscape and Outlook

After a dreadful March, investor sentiment was better in April and markets recovered strongly. Economies around the world have gradually started to lift respective virus containment measures.

Discretionary Retailers dampened by COVID-19, but relief is coming

Since COVID-19 has grappled Australia, the Retail Industry has seen massive disruptions as non-essential retailers closed stores forcibly. When one door closes, other opens; this came true for a lot of retailers as they took to the online route to make up for the lost sales, but people usually do not buy items like car through online channels.

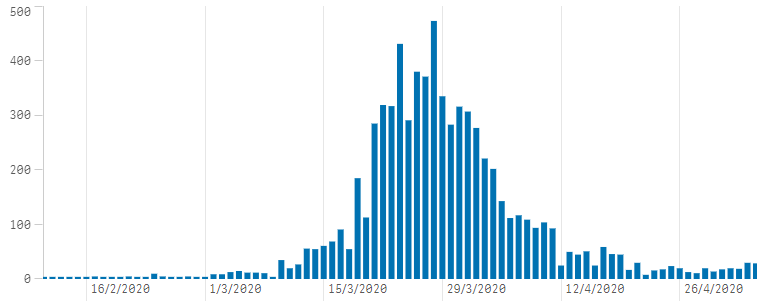

During late March, the Australian Government imposed measures to curb the spread of the virus, which has yielded positive results. As a validation to the efforts, the daily newly reported coronavirus cases have been coming down over the recent past. This has enabled the Government to consider easing restrictions just like New Zealand across the Tasman Sea.

Fig 1: Daily Reported Cases of COVID-19

Source: health.gov.au as of 5 May 2020

It is evident that the peak of the virus infection may have passed in Australia as daily number of cases are coming down over the past month. Recently, the Prime Minister and National Cabinet also noted that the measures have been largely successful in flattening the COVID-19 curve.

The National Cabinet will review the initial phase of removing baseline restrictions on 8 May 2020. The Australian Health Protection Principal Committee (AHPPC) set conditions before any removal of restrictions, of those restrictions – four are yet to be satisfied. The country is on the way to meet rest of the conditions, and the remaining four would be expedited by the States and the Federal Government.

More recently, the National Cabinet noted that testing and contact tracing are necessary conditions prior to any removal of baseline restrictions. And it agreed with NZ PM Jacinda Ardern to restart trans-Tasman travel.

The body has established a three-step framework, and States and Territories would be determining the course of each step. However, it was said that some health measures would continue to be enforced, including social distancing and international travel restrictions.

Record retail sales figures recently, firming up CPI and subdued discretionary spending

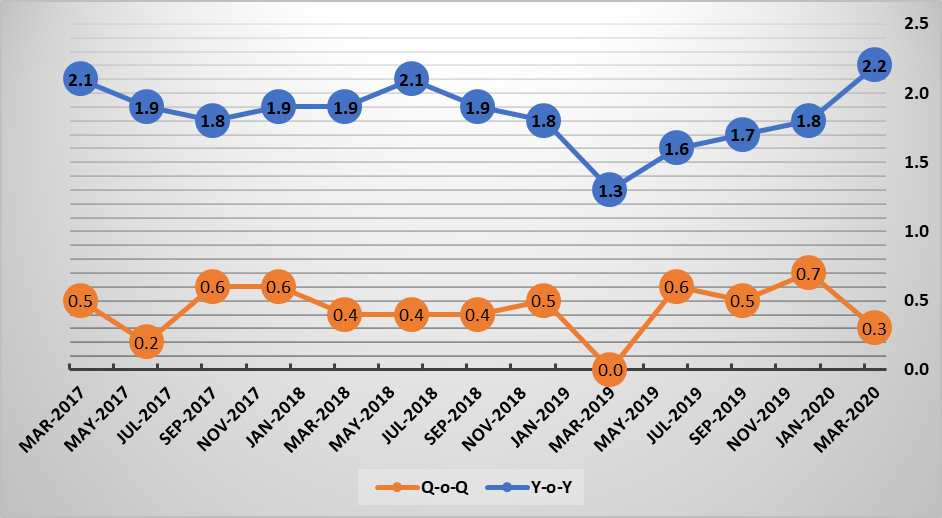

Latest CPI print suggested that CPI increased by 2.2% (y-o-y) in the March quarter, largely led by price increases in food, beverages, tobacco and health. Within discretionary retail categories, clothing and footwear group fell by 0.7% over the previous quarter, led by fall in women garments, but the category has recorded an increase of 2% over the year.

Furnishings, household equipment and services category recorded an increase of 0.8% over the previous quarter, led by 3.4% increase in household non-durables. Over the past one year, the category has seen an increase of 2.2%, primarily driven by childcare.

Fig 2: Yearly and Quarterly Change in CPI (%)

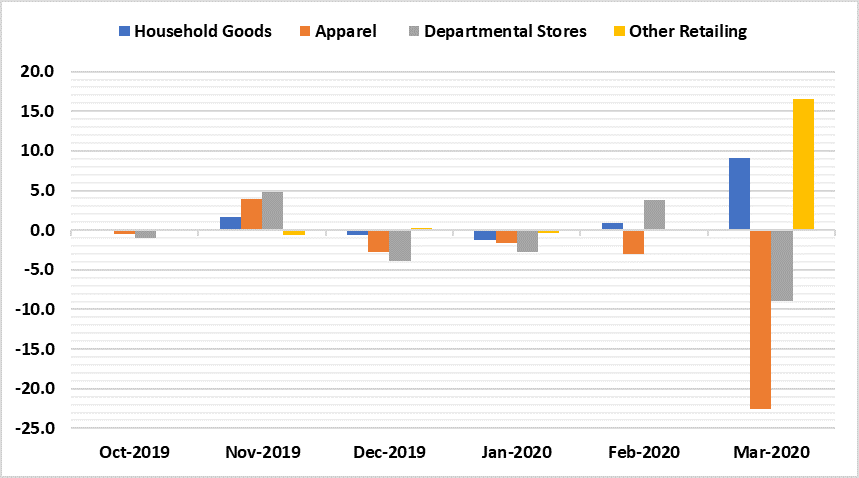

Despite an overall jump in retail sales in March, most of the discretionary retail categories suffered pain during the month, largely due to the inability to trade normally amid social distancing measures. However, some relief is likely to arrive gradually as State Governments are set to roll out softer restrictions soon.

In March, the abnormal jump in the retail trade were attributed to panic buying as people rushed to buy food, household goods, and stay-at-home items. During the month, on a seasonally adjusted terms, food retailing was up 24.1%, households goods retailing recorded an increase of 9.1%, and other retailing was up 16.6%, which includes items like pharmaceuticals, toiletry goods, cosmetics etc.

Fig 3: Discretionary Retail Monthly Change (%)

Source: ABS

On the flip side during the month, the sales in the Apparel and personal accessories were down 22.6%, and departmental stores suffered a fall of 8.9%, all on a seasonally adjusted term.

With such numbers coming to the fore it is quite evident that the attention on government actions would be called for. Let us scan through the steps taken by the government authorities to navigate through tough times.

Policymakers have helped to cushion the blow

The Reserve Bank of Australia has pumped a lot of liquidity into the system and has taken measures to lower the funding costs of the businesses. A range of measures have been floated by the Government to enable funding access for the businesses.

Among the most significant measures, JobKeeper Subsidy is helping businesses to pay their employees, and businesses must have seen a contraction in turnover of 30% (turnover below $1 billion) or 50% (turnover above $1 billion) to avail the benefit; this scheme has provided substantial relief as wage bills form a significant part of operating expenses in retail industry. Since the scheme was announced, some of the discretionary retail stocks have recovered from the March lows.

The State Governments have also introduced various schemes to support the beleaguered businesses due to COVID with measures ranging from payroll tax to rental reliefs to landlords. Most of the Government owned properties have introduced rental relief measures for the tenants.

Over to the consumer side, the Governments have been paying a range of grants to eligible citizens, and Australian households also have an option to draw down around $20k from superannuation funds due to COVID-19 led hardships.

Recently, the Australian Prudential Regulation Authority (APRA) has noted that $1.3 billion was paid to members by super funds with an average benefit of $8k in the first week of the scheme.

Over the last one year, the policy interest rates have fallen by cumulative of 1.25%, which had helped to fuel the recovery in the housing market, amongst other things. As the lagged impact of rate cuts on consumer spending was pegged to be visible, the COVID-19 led implications have suppressed these possibilities.

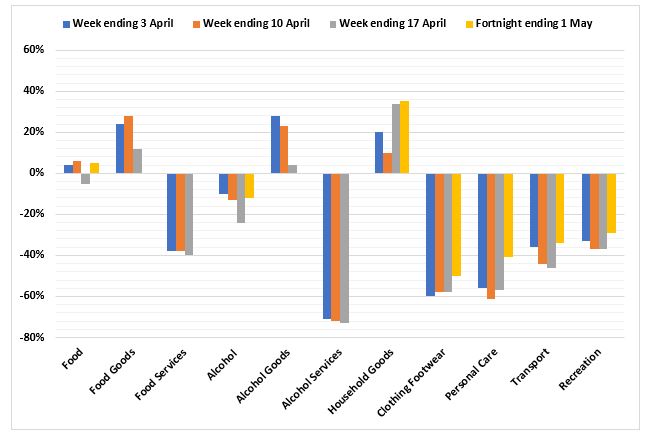

Commonwealth Bank card spending insights are suggesting sharp falls across the discretionary retail categories, including apparel, recreation, and personal care. However, the latest data suggests that spending momentum has improved over the last fortnight.

Fig 4: Commonwealth Bank Card Spending Data (Y-o-Y)

Source: Commonwealth Bank Website

Discretionary Retailers have faced detrimental consequences, but resilient businesses will likely consolidate positions..

As store closures intensified across the country and the world, the cash flows of retailers have seen an exogenous shock. Some businesses also tapped investors for additional capital to strengthen the balance sheet. But many businesses did not even raise capital, which reflects the soundness of the capital management policies.

Although policymakers have introduced substantial measures to cushion the blow for businesses, but casualties and damage are inevitable for some businesses that would allow resilient businesses to gain additional market share, thus consolidating their positions. Cash preservation efforts have been discernible as companies stranded employees, deferred dividends and non-essential capex.

Retail players to leverage on the Recovery Story

With the recovery in the horizon, some non-discretionary and discretionary players would benefit. For example: Speciality players such the auto component suppliers could benefit. During the month of April, the auto industry recorded a fall of 48.5% in new vehicle sales, thanks to COVID-19. However, the demand for spare parts and after sale service is likely to go up as people might prefer the personal mode of transportation over public transport to follow social distancing.

The easing of restrictions across the country should see momentum pick up for retailers as households slowly get back to meeting their necessities.

II. Investment Theme and Stocks under Discussion (SUL, MTS, HVN, LOV and APE)

After understanding the sector, let us now look at five retailers listed on the ASX. The price potential of the companies under discussion has been analysed based on ‘Discounted Cash Flow’ methods.

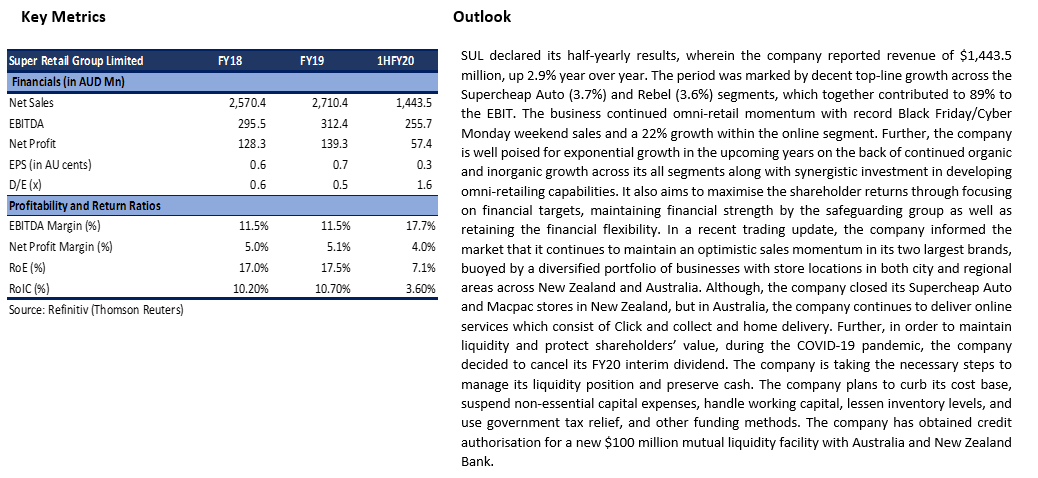

1. ASX: SUL (SUPER RETAIL GROUP LIMITED)

(Recommendation: Buy, Potential Upside: Low Double Digit, Mcap: A$ 1.22 Billion)

Super Retail Group Limited is engaged in operating specialty retail stores in the automotive, tools, leisure and sports categories.

Valuation

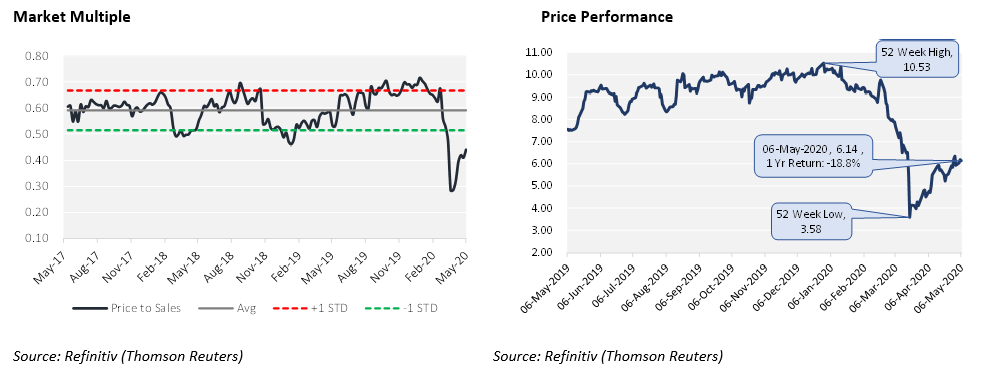

The group’s stores in Australia are operational; however, there is lesser footfall as the people are staying indoors, which is partly offset by online channels. The group is witnessing robust demand for essential items such as portable gas and fuels, batteries, refrigeration equipment, hygiene product etc. Despite a decent first half, we believe FY20 full-year sales to decline and expect it to pick gradually from FY21 onwards. Our illustrative valuation model suggests that stock has a potential upside of ~17% on 6 May 2020 closing price. The Stock is offering a dividend yield of ~11.6% as on 6 May 2020..png)

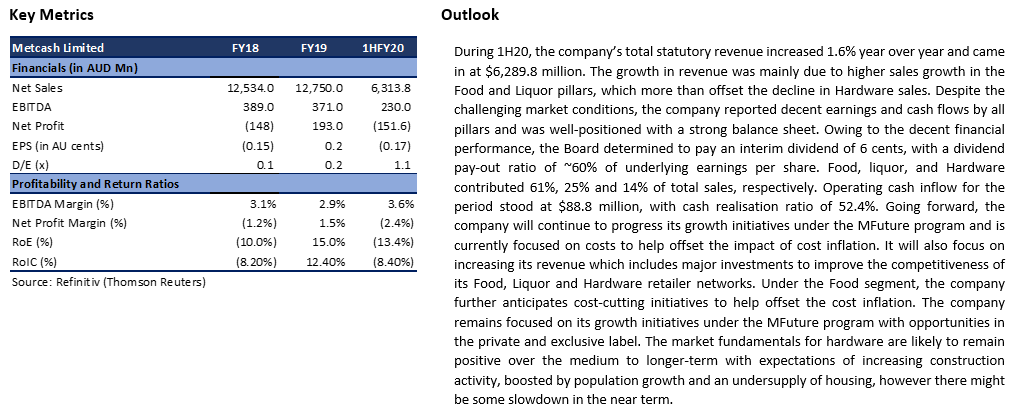

2. ASX: MTS (METCASH LIMITED)

(Recommendation: Buy, Potential Upside: Low Double Digit, Mcap: A$ 2.48 Billion)

Metcash Limited is a supplier or a wholesaler to individual retailers in liquor, food, grocery, hardware, and automotive businesses.

Valuation

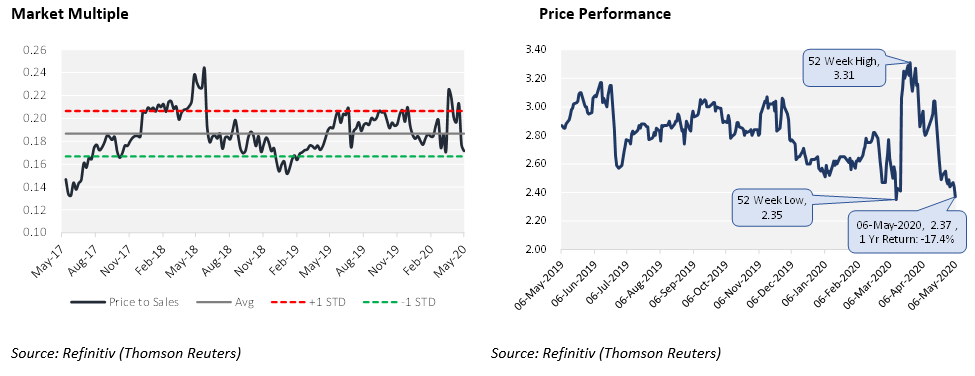

We believe the group’s revenue to surge in FY20 as the group’s witnessed a significant jump in demand for the food products as the people were in panic buying mode. The revenue is expected to decline in FY21 as the situation is likely to be back to normal. We believe margin to remain under pressure in the near term owing to the higher cost associated with hygiene and other safety measures. Our illustrative valuation model suggests that stock has a potential upside of ~16% on 6 May 2020 closing price. The Stock is offering a dividend yield of ~7.8% as on 6 May 2020..png)

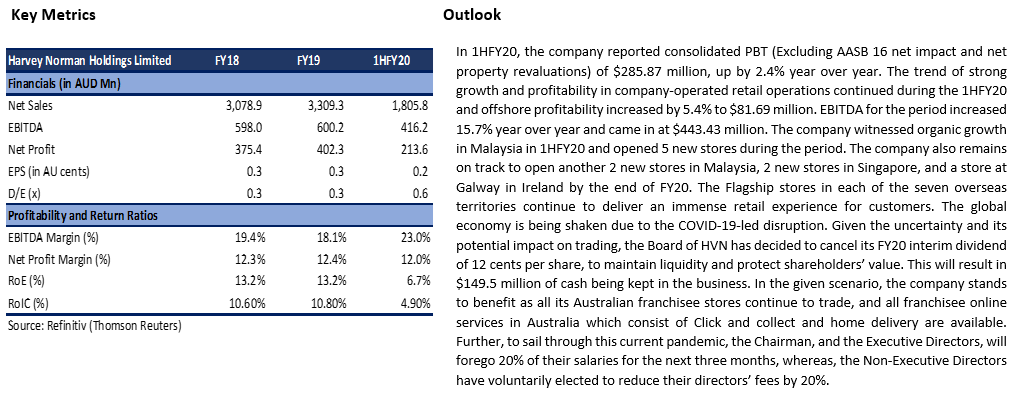

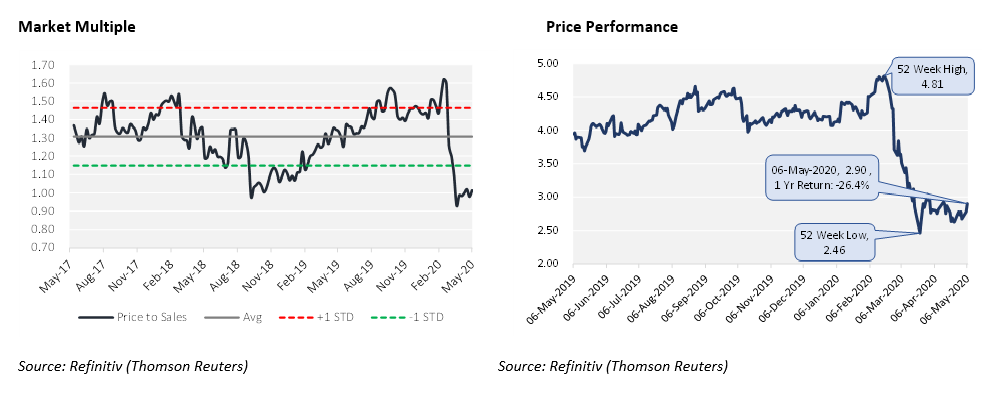

3. ASX: HVN (HARVEY NORMAN HOLDINGS LIMITED)

(Recommendation: Buy, Potential Upside: Low Double Digit, Mcap: A$ 3.26 Billion)

Harvey Norman Holdings Limited is an Australia based company with principal activities of property, digital enterprise, integrated retail, and franchise.

Valuation

We expect the group’s revenue to decline in FY20 as some of the group’s global stores are closed owing to COVID-19 outbreak. However, an uptick in the revenue is expected in the second half of 2020 as the Governments’ across the globe are expected to ease the lockdown and allow the stores to operate. Our illustrative valuation model suggests that stock has a potential upside of ~19% on 6 May 2020 closing price.The Stock is offering a dividend yield of ~10.3% as on 6 May 2020.

.png)

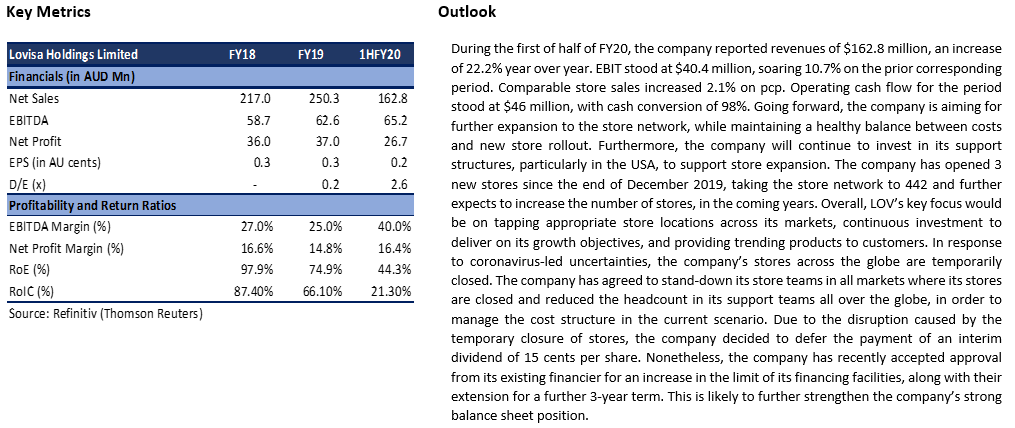

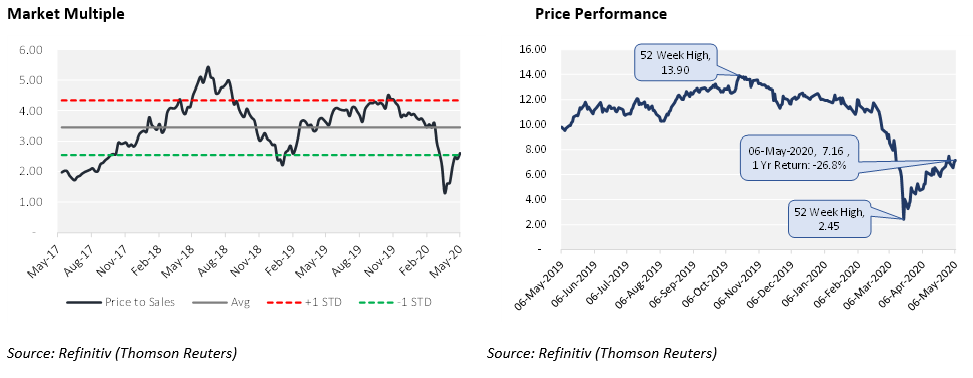

4. ASX: LOV (LOVISA HOLDINGS LIMITED)

(Recommendation: Hold, Potential Upside: Low Double Digit, Mcap: A$ 751.1 Million)

Lovisa Holdings Limited engages in the retail sale of fashion jewellery and other accessories, through a network of retail and franchise stores.

Valuation

The group reported a decent number in the first half and was on track to replicate the same performance in the second half. However, a temporary closure of all the stores amid COVID-19 outbreaks is going to take a toll on the financials. We expect the group’s revenue to decline in FY20 and expect the margins to remain under pressure in the near term. Although the growth in revenue is likely to rebound, we would like to stay on side-line by the time there is no clarity on the store opening. Hence, we maintain our Hold stance on the stock. Our illustrative valuation model suggests that stock has a potential upside of ~10% on 6 May 2020 closing price. The Stock is offering a dividend yield of ~6% as on 6 May 2020..png)

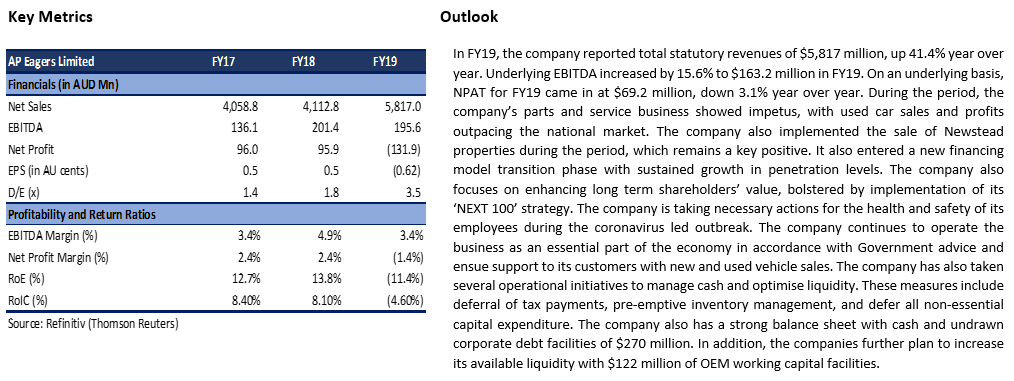

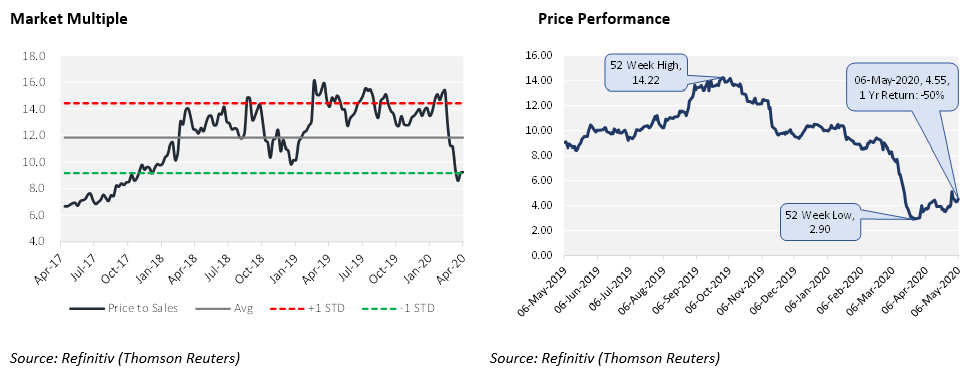

5. ASX: APE (AP EAGERS LIMITED)

(Recommendation: Watch, Potential Upside: Low Double Digit, Mcap: A$ 3.26 Billion)

AP Eagers Limited is among the largest automotive retailers in Australia, which is involved in the business of supplying new and used cars, trucks and buses, and associated products and services.

Valuation

The group’s revenue growth to remain elevated in FY20 as the year will mark the full-year contribution of Automotive Group Holdings (AHG) in the group’s revenue. The group acquired AHG’s full ownership in August 2019. If we exclude AHG’s contribution, the group’s revenue is expected to decline owing to the turmoil in automobiles demand. Recent car sales data shows a decline of ~49% in April 2019. The group has reduced its workforce significantly and put the remaining staff on the temporary roster. We do not see any respite in demand for automobiles in the near term as an expected uptick in unemployment is going to take a toll on the demand. Hence, we maintain our Watch stance on the stock. Our illustrative valuation model suggests that stock has a potential upside of ~9% on 6 May 2020 closing price. The Stock is offering a dividend yield of ~7.9% as on 6 May 2020..png)

Note: All the recommendations and the calculations are based on the closing price of 6 May 2020. The financial information has been retrieved from the respective company’s website and Refinitiv (Thomson Reuters). All the recommendations are valid on 7 May 2020 price as well.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...