Kalkine has a fully transformed New Avatar.

Australia’s retail sector forms a significant portion of the country’s GDP and is a key factor in defining the overall economic growth. The retail industry of Australia that employs a large section of the society, has been on a wobbly ground since the outbreak of coronavirus. A series of unprecedented events due to COVID-19 over the past few months have been shaping up the retail turnover, with the most recent being a significant surge in sales, solely attributable to the ease of restrictions around the country.

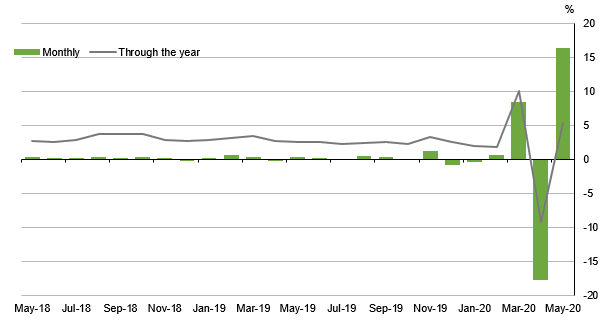

In May 2020, Australian retail sales rose significantly in comparison to April 2020. Pursuant to the Australian Government’s popular three-phased plan to ease the restrictions imposed across the country and a gradual re-opening of the economy, retail sales for May’20 went up by 16.3%. In absolute terms, the seasonally adjusted estimate for May stood at $4,038.4 million. Data provided by the Australian Bureau of Statistics (ABS) also emphasised that this was the largest seasonally adjusted month-on-month rise ever published in the 38 years of the Retail Trade survey.

According to the recent trends in the retail sector, many companies notified regarding the reopening of stores after staying offline for a long time. COVID-19 related factors, including government directives, health & safety of the staff, change in consumer behavior, increased operating costs, etc., compelled the retailers to announce complete or partial shutdown of stores. While some of the businesses turned towards online means of generating sales, other players that lacked digital capabilities and online infrastructure were seen bearing the brunt of the turmoil in the market.

Key Factors Driving the Sales: Reopening of stores, combined with increased consumer spending, has possibly been a major driver for retail sales. During the lockdown, a huge setback in retail sales was also due to the skepticism around physical purchase which has now begun to change after the country reported a negligible number of COVID-19 cases. The collective efforts of the Australian government and citizens have led the country to the recovery lane well before others.

Contributors to Increased Retail Sales in May: In May 2020, Food retailing witnessed an increase of 7.2% in comparison to the previous month, on the back of consumers purchasing additional food and beverage for home consumption. Turnover for Perishable and Non-Perishable goods increased by 7% and 3.8%, respectively. Turnover for all other products increased by 5.8% on April’20. In the household goods segment, all subgroups including furniture, electronic goods, houseware and textile goods, floor covering, etc., recorded a significant uplift in sales in comparison to April’20. Turnover in household goods retailing witnessed a rise of 30% in comparison to the prior corresponding month, i.e., May’19. Turnover in clothing, footwear and personal accessory retailing also witnessed large increases due to ease of restrictions. Month-on-month rise in clothing, footwear and personal accessory retailing was a whopping 100%. However, it went down over 20% in comparison to pcp. Similarly, sales from cafes, restaurants and takeaway food services increased by ~30% in comparison to April’20 but were 30% lower than the prior corresponding month.

Monthly Retail Trade (Source: Australian Bureau of Statistics)

Identifying the Pattern for Retail Sales in March & April: Surprisingly, the increase came in after a sharp plunge in retail sales for April 2020. As per ABS, seasonally adjusted estimates for retail trade went down by 17.7% in April, following a rise of 8.5% in March. This was a result of a reduction in panic buying by consumers which was a major driver for March retail sales. After the outbreak of coronavirus, consumers began stocking up essentials and were majorly inclined towards the purchase of food and hygiene products, shaping up the numbers for March. In the next wave of events, consumer behavior was characterized by reduced purchasing of food, clothing, household goods, etc. Restaurant services also suffered a downfall in April due to the impact of mandatory shutdown advised by the government. A significant number of retail businesses did not trade at all in April and some of them continued to operate through the online channel. These factors were collectively responsible for the steep fall in April.

To conclude, the unprecedented volatility in the retail sector poses a challenge in determining a fixed set of factors that will drive the sales numbers, going forward. While optimism around increased consumer spending and subsequent rise in sales can be the signal for an uplift in sales, other factors such as a rising rate of unemployment, slowdown in wage growth, uncertainty regarding consumer behavior and potential impact of COVID-19 in the near-term cannot be ruled out. The above factors can weigh heavily on the positive drivers and may impact retail sales in the future. In light of the above factors, some of the retail companies have been performing fairly well, both operationally and financially, and have demonstrated resilience to the volatility in the market. Let us have a look at these stocks in detail:

1. Freedom Foods Group Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 1.02 Billion, Annual Dividend Yield: 1.49%)

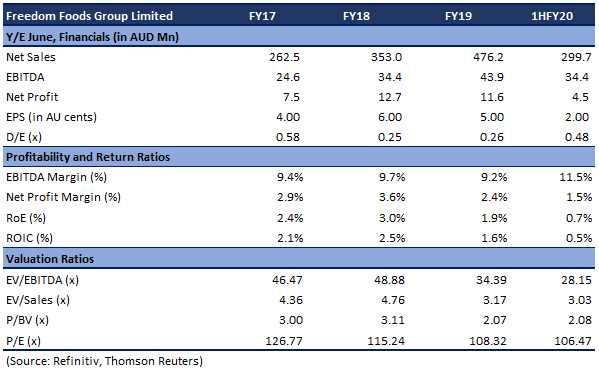

Material Cash Cost Savings Expected in FY21: Freedom Foods Group Limited (ASX: FNP) is engaged in the sourcing, selling, marketing, manufacturing, and distribution of specialty cereal, snacks, and dairy beverages. During 1HFY20, the company’s net sales and operating EBITDA went up by 32.6% and 55.6%, respectively, backed by growth across all key branded categories and channels. The period was also marked by growth in export markets, with exceptional revenue growth of 58% in SE Asia.

Outlook: For FY20, the company expected capital expenditure in the range of $120 million - $130 million. Throughout the pandemic, the supply of key raw materials and packaging inputs has remained stable. Moreover, the company also has a range of alternative suppliers to avoid any disruptions in the operations. The company has begun reshaping its operational footprint in response to the changing circumstances. For instance, the Shepparton operation has begun the transition by relocating external warehouse and logistics functions to an integrated on-site operation to facilitate further export growth. The above efforts are expected to result in material cash cost saving in FY21. In response to the COVID-19 pressures, the company cancelled its dividend and does not expect to pay a full-year dividend.

During March and April, the company experienced strong growth across the Australian retail grocery channel due to a shift in consumer spending. Sales from the channel normalised in May. After the ease of restrictions, the Out of Home Channel in Australia demonstrated signs of recovery, with great support for the key brands in the channel. Demand for nutritional ingredients such as Lactoferrin remained strong, with ~80% of the planned FY21 output already contracted.

Key Risks: The second half usually contributes 60% of full-year operating EBITDA of the company. However, performance in 2HFY20 will be impacted by the level of sales, impact of doubtful debts, an unrecovered higher seasonal milk pricing, and a changed sales mix from March to June. The uncertainty regarding the nature, scale and duration of the impact poses a risk on the company’s future performance. However, the company also highlighted that the adverse impact will be a result of the one-off charges related to the consolidation of external warehousing activities and a detailed review of product offerings.

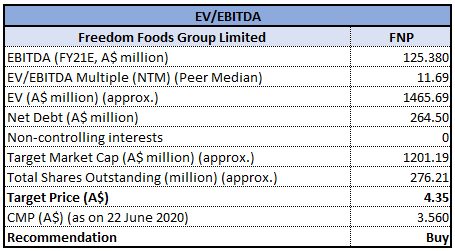

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

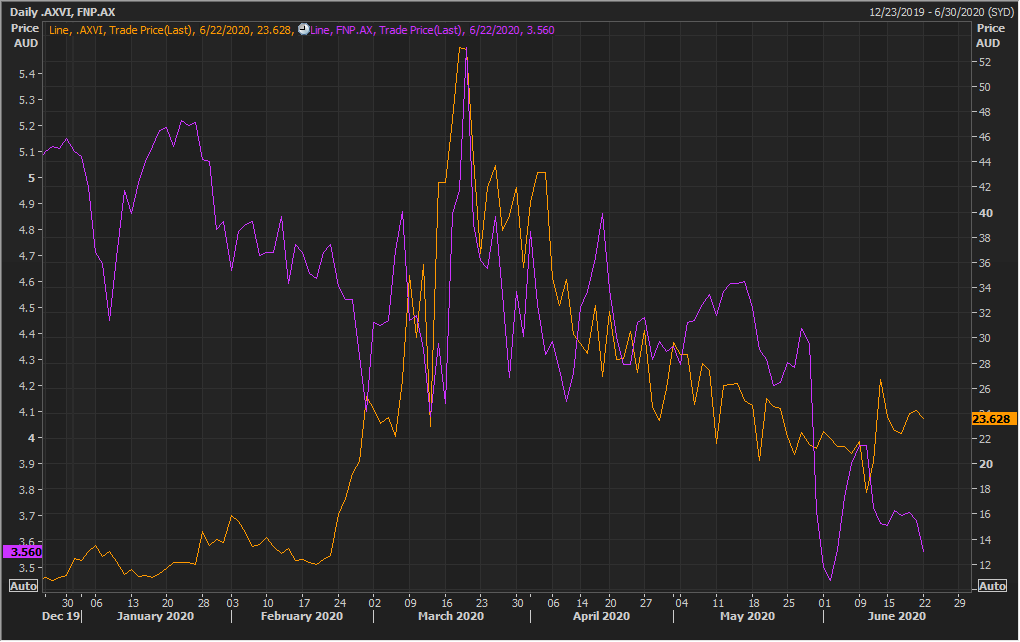

A-VIX vs FNP (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: In the last six months, the stock has corrected by 29.64% on ASX and is currently inclined towards its 52-week low price of $3.41. Amid the current uncertain environment, demand in the retail grocery channels continued to grow in SE Asia, a key strategic growth market for the company. Despite significant market volatility in March, the stock demonstrated resilience and has shown favorable movements in recent months. This was partially due to the continued demand for the company’s products. The business has proved to be immune to the market turmoil because of the continuity of operations on account of being an essential service provider. We have valued the stock using the EV/EBITDA multiple based illustrative relative valuation method and arrived at a target price with a low double-digit upside in percentage terms. Hence, we give a “Buy” recommendation on the stock at the current market price of $3.56, down 3.261% on 22nd June 2020.

2. Treasury Wine Estates Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 7.71 Billion, Annual Dividend Yield: 3.74%)

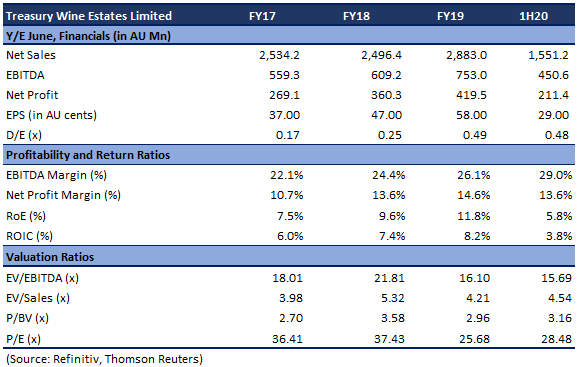

TWE Ready to Ride the Growth Wave: Treasury Wine Estates Limited (ASX: TWE) is an international wine business with a portfolio of luxury, premium and commercial wines. During 1H20, TWE continued to deliver growth in earnings with an increase of 6% in EBITS to $366.7 million. In the same time span, NPAT of the company went up by 5% to $229.2 million, and EPS was up by 5% to 31.9 cents per share. This was mainly due to the premiumization strategy of the company, which continued to drive operating performance across all regions.

Outlook: The company seems well-positioned to navigate to a stronger endpoint once the COVID-19 pandemic subsides. Diversified end markets of the company along with increasing opportunities will result in the growth of its iconic brand portfolio across all markets. With a continued focus on accelerating premiumization, TWE retains a portfolio of compelling brand propositions across all price points. The company has strengthened its business model and is ensuring long-term success.

The company is pursuing a range of initiatives to reduce its cost base and is focused on accelerating its strategy to maximize potential gains. The company is closely working with its partners to resume operations. It saw strong momentum for the portfolio through e-commerce channels, and the performance of the portfolio has been skewed towards the lower margin Commercial and Masstige portfolios. Overall levels in the liquor retailing have been optimistic owing to easing of restrictions imposed on bars, clubs, and events.

Key Risks: Recent droughts, heat and fires in Australia and other climatic changes have posed some challenges with respect to the harvest of the Australian vintage. The company relies on several key partners to support delivery. However, the restrictions imposed by the government may impact the production levels. The recovery in consumer patterns may remain subdued, impacting the financial performance.

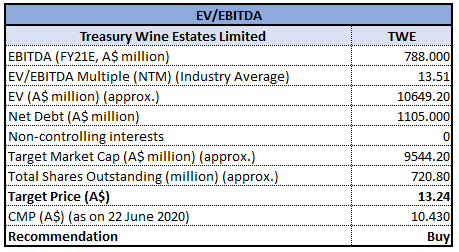

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

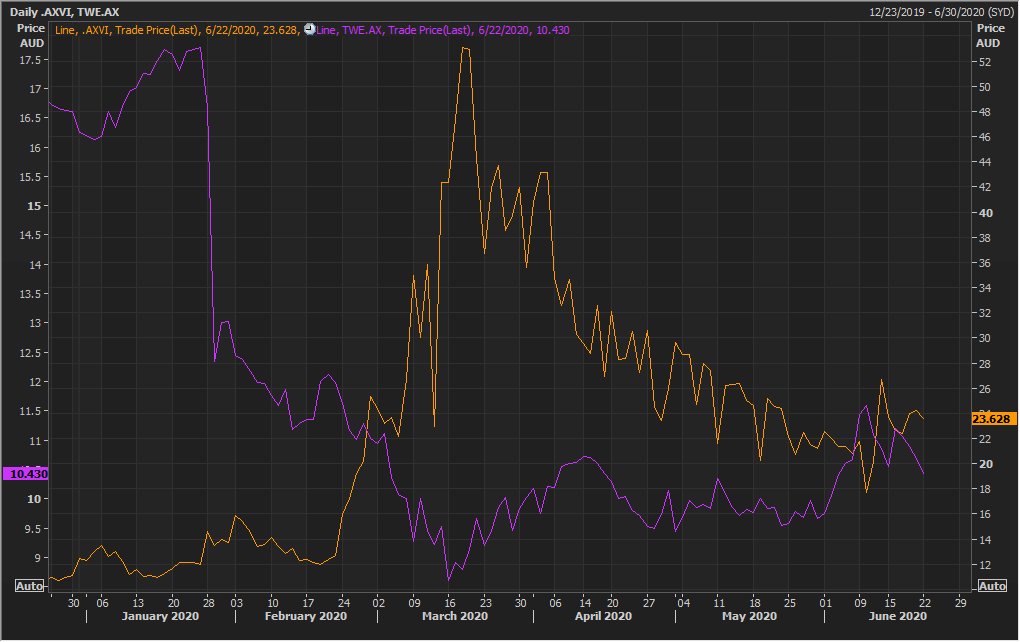

A-VIX vs TWE (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: In the last six months, the stock has corrected by 36.37% on ASX and is currently inclined towards its 52-week low price of $8.4. TWE continued to deliver sustainable, margin accretive growth despite the setback in the markets due to the global pandemic. It maintains a flexible and efficient capital structure that is consistent with an investment-grade profile, including a stable and well-diversified debt maturity. After the market depicted high volatility due to the outbreak of coronavirus, the stock price witnessed the shockwaves due to disruptions to the business. However, it has gradually started to recover as per the latest movements. According to the recent sales trends, the demand for liquor is recovering, which will be a key factor driving the stock, going forward. We have valued the stock using the EV/EBITDA multiple based illustrative relative valuation method and arrived at a target price with a low double-digit upside in percentage terms. Hence, we give a “Buy” recommendation on the stock at the current market price of $10.43, down 2.432% on 22nd June 2020.

3. Harvey Norman Holdings Limited (Recommendation: Hold, Potential Upside: Low Double-Digit)

(M-cap: A$ 4.37 Billion, Annual Dividend Yield: 9.4%)

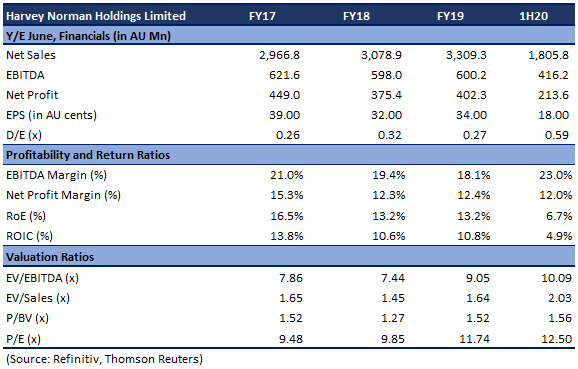

Continued Trend of Growth and Profitability: Harvey Norman Holdings Limited (ASX: HVN) is engaged in the integrated retail, franchise, property entity, and digital system including the sale of furniture, bedding, computers, etc. During 1H20, the company witnessed a continued trend of growth and profitability in its retail operations with a rise of 5.4% in profitability offshore to $81.69 million. In the same time span, a decrease in net property revaluation increment resulted in a decline in profit before tax to $301.15 million. HVN delivered organic growth in Malaysia and with the opening of 5 new stores. The company’s balance sheet continues to prove its strength, anchored by real property assets and a solid working capital position.

Outlook: With record low interest rates and the momentum built up in the residential property market, HVN places a positive long-term outlook. The increased spending on infrastructure and a brighter outlook for the resources sector further adds to the growth opportunities.

The company’s brands have serviced the essential needs of customers despite the uncertain times due to the outbreak of COVID-19. Aggregated Sales for FY20 on the YTD basis to 31st May 2020 saw an increase of 7.4%. The positive effect in aggregated franchisee sales from July 2019 to May 2020 was mainly due to the recommencement of the online sales and appreciation in currencies including Euro, New Zealand Dollar, the UK Pound, etc. Despite the uncertainty surrounding the spread of Covid-19, the company saw an increase in total sales in New Zealand, Ireland, Croatia, and Malaysia.

Key Risks: There are several factors that may pose a risk to the achievement of business strategies. A decline in the commercial property sector may result in the softening of property asset values. It also exposed to the counterparty risks from the service providers. The company maintains a competitive position but is exposed to the current uncertain macroeconomic environment.

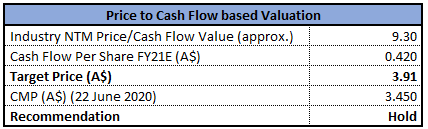

Valuation Methodology: P/CF Multiple Based Relative Valuation (Illustrative)

P/CF Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

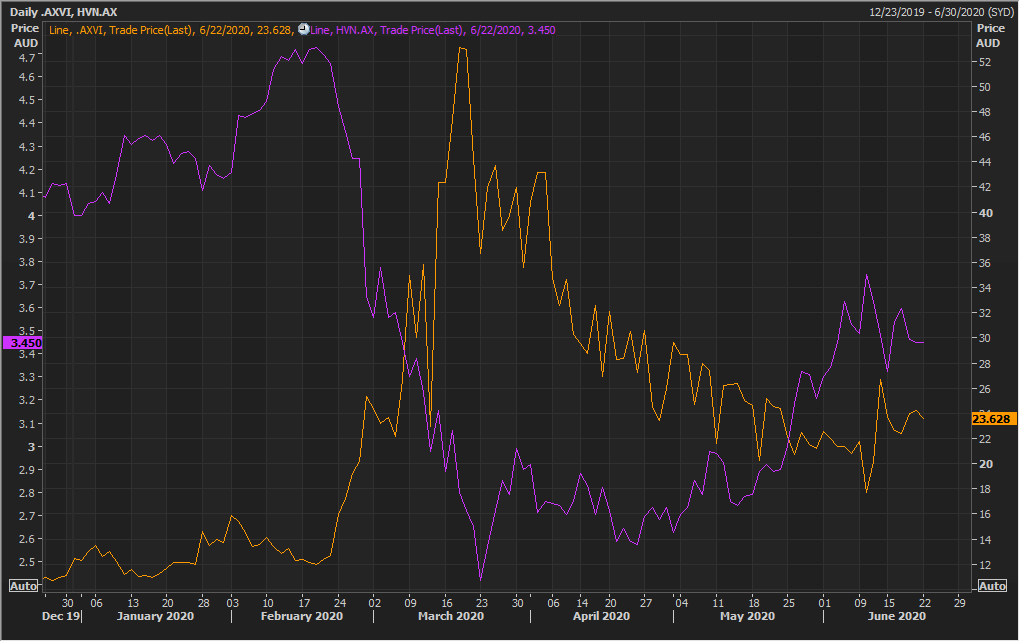

A-VIX vs HVN (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: In the last six months, the stock has corrected by 15.22% on ASX and is currently trading slightly above the average of its 52-week trading range of $2.285 - $4.787. Despite the gloomy environment from the onset of COVID-19, HVN is well-placed for growth. It is growing its international footprint and is on track for expansion opportunities. The stock of Harvey Norman Holdings has demonstrated decent recovery after the COVID-19 led market crisis, as the company continued to serve the essential needs of customers. The company has a loyal customer base, sticking to it even during uncertain times and will help to drive sales during this period of recovery. We have valued the stock using the P/CF multiple based illustrative relative valuation method and arrived at a target price with low double-digit upside in percentage terms. Hence, we give a “Hold” recommendation on the stock at the current market price of $3.45, down 1.709% on 22nd June 2020.

4. Adairs Limited (Recommendation: Hold, Potential Upside: Low Double-Digit)

(M-cap: A$ 390.57 Million, Annual Dividend Yield: 6.49%)

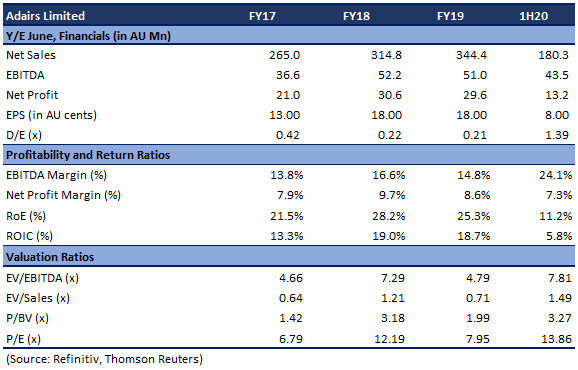

Record Sales and Profit: Adairs Limited (ASX: ADH) is a specialty retailer of home furnishings and homewares in Australia and New Zealand, through both retail stores and online channels. During 1H20, sales of the company went up by 8.6% to $178.9 million and online sales witnessed an increase of 31.6% to $31.6 million. In the same time span, the company reported an increase of 9% in gross profit to $109.3 million. This was mainly due to the benefits from a coordinated program of sourcing and pricing initiatives, combined with a focus on reduced depth of markdowns.

Outlook: The company has acknowledged the elevated level of uncertainty which may persist for the medium term and has provided guidance for FY20 and expects group sales to be in the range of $385-390 million. Management is focused on ensuring that the business is well-positioned to respond to the associated risks and opportunities.

According to a recent trading update by the company, all Adairs stores which were closed due to the restrictions imposed by the Government have now re-opened. Since the re-opening, the company has seen strong sales across both the store network and online channel and reported an increase of 27.4% in LFL sales in the span of 24 weeks to 14 June 2020. While stores were closed, the company’s Australian online businesses remained fully operational and reported a significant increase of 221% in online sales.

Key Risks: The performance of the company is influenced by a variety of economic and business conditions, including consumer spending, inflation, interest and exchange rates, access to debt and capital markets and government policies. Many of the company’s products are discretionary goods where consumer preferences and tastes can change quickly. An overestimation in demand could adversely affect its financial performance. The current macroeconomic environment may reduce the demand for ADH’s products, thereby reducing product sales.

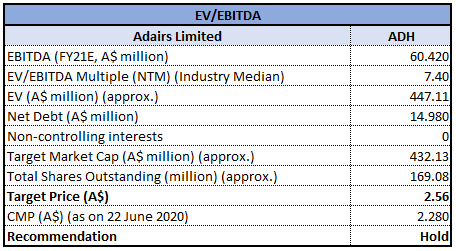

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

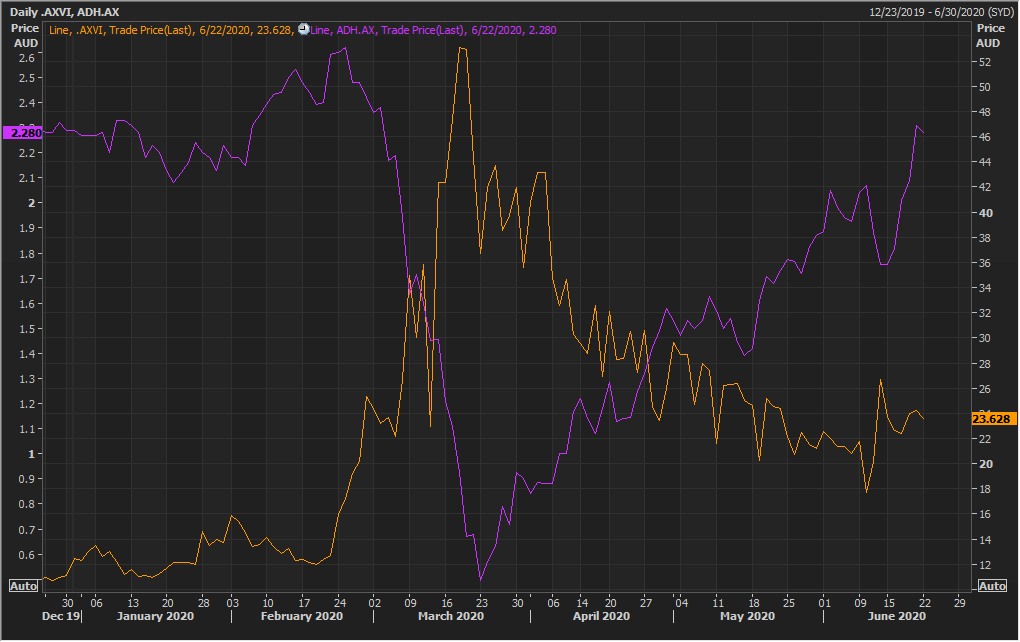

A-VIX vs ADH (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: In the last one month, the stock gave positive returns of 43.48% and is currently inclined towards its 52-week high price of $2.74. The company retains a strong balance sheet with significant headroom within banking covenants. It has taken pro-active measures to mitigate the impact of the COVID-19 crisis with a focus on maintaining the financial position of the business. The COVID-19 led market fallout and the impact on the stock price is now an old story for Adairs Limited. The success of the business and a remarkable online channel is reflected in the speedy recovery, as shown in the chart above. Moreover, reopening of stores and the recent trading update represent a potential tailwind for the company. We have valued the stock using the EV/EBITDA multiple based illustrative relative valuation method and arrived at a target price with a low double-digit upside in percentage terms. Hence, we give a “Hold” recommendation on the stock at the current market price of $2.28, down 1.299% on 22nd June 2020.

.jpg)

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Note:

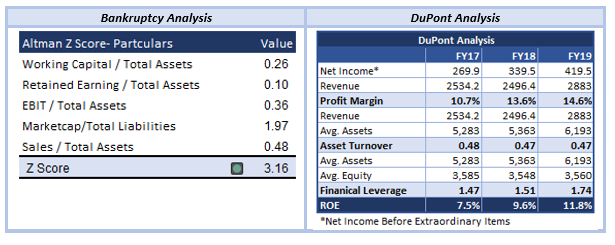

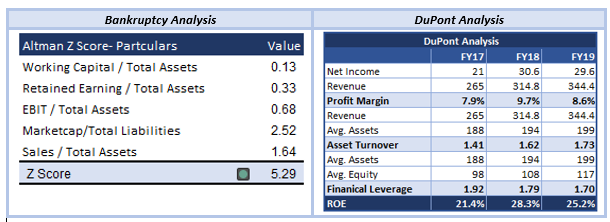

Altman’s Z-Score Model:

(1) When Z-Score <1.81 then it is in Distress Zone

(2) When Z-Score is between 1.81 and 2.99 then it is in Grey Zone

(3) When Z-Score > 2.99 then it is in Safe Zone

The above relative valuation implies a target price incorporating the key positive factors driving the business and indicate long term potential of the stock. Prices, however, remain subject to any short-term movements due to the impact of coronavirus on the business fundamentals.

All the recommendations and the calculations are based on the closing price of 22 June 2020. The financial information has been retrieved from the respective company’s website and Thomson Reuters.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...