Company Overview: Resolute Mining Limited is engaged in gold mining, and prospecting and exploration for minerals. The Company operates through three segments: Ravenswood, Syama and Bibiani. It operates over two mines, the Syama gold mine in Africa and the Ravenswood gold mine in Australia. The Syama gold mine is approximately 30 kilometers from the Cote d'Ivoire border and over 300 kilometers southeast of the capital Bamako. The Ravenswood gold mine is approximately 95 kilometers south-west of Townsville and over 60 kilometers east of Charters Towers in north-east Queensland. Its key development focus is in Mali. It has a portfolio of open pit oxide resources located in various satellite pits to the north and south of the main Syama pit. In Ghana, it owns over 90% underground Bibiani Gold Project. It is exploring over 10,800 square kilometers of prospective tenure across two continents and holds Birimian age greenstone tenure in West Africa, with tenements across Mali, Ghana and Cote d'Ivoire.

.png)

RSG Details

FY19 Production Estimated At 400,000 oz with AISC of US$1,020/oz: Resolute Mining Limited (ASX: RSG) is a successful gold miner with more than 30 years of experience as an explorer, developer, and operator of gold mines in Australia and Africa, which have produced more than 8 million ounces of gold. It currently owns gold mines, namely, the Syama Gold mine in Mali, the Ravenswood Gold mine in Australia, the Bibiani Gold mine in Ghana, and the Mako Gold mine in Senegal. The company has changed its financial year end from 30 June to 31 December. Looking at the past performance, total revenue of the company has grown from $222.8 Mn in FY18 (six months to 31 December 2018) to $324.0 Mn in H1FY19, an increase of 45.42%. Bottom-line of the company has grown from a loss of $3.3 Mn in FY18 to profit of $35.7 Mn in H1FY19.

Total gold production for September’19 Quarter and Year-to-Date (till September 30) was reported at 103,201 oz at All-In Sustaining Cost (AISC) of A$1,759 per oz and 279,438 oz at an All-In Sustaining Cost of A$1,389 per oz, respectively. As per the revised production guidance for FY19, 400,000 ounces of gold has been estimated at AISC of US$1,020 per ounce as compared to the previous guidance of US$960 per ounce. Company’s total cash, bullion and listed investments for September’19 Quarter were reported at $179.0 Mn, as compared to $56.3 Mn in the previous quarter.

The company has established a portfolio of strategic investments in highly prospective, well managed African-focused gold exploration companies to provide a pipeline of future development opportunities. The company has delivered on important strategic goals for 2019 with listing on the London Stock Exchange, ramp-up of the Syama Underground Mine, and acquisition of Toro Gold. The company expects gold production for 2019 to come in at 400,000 ounces at all-In Sustaining Cost of US$1,020 per ounce with further growth and upside to come in 2020.

.png)

Quarterly Cash, Bullion and Investments Reconciliation (Source: Company Reports)

September’19 Quarter Key Highlights: Gold production for the quarter stood at 103,201 oz at an All-In Sustaining Cost (AISC) of US$1,202/oz. Gold sales for the period stood at 127,265 oz at an average gold price received of US$1,362/oz.

Mako mine delivered gold production of 44,191 oz at an AISC of US$716/oz in its first quarter under the ownership of RSG. Mako Gold Mine is the company’s tenth gold mine and high quality, strongly cashflow generative producing asset, which complements RSG’s existing portfolio of large-scale, long-life mines.

Syama sulphide circuit achieved daily recoveries above 85% target. The high recovery can be attributed to an improvement in sulphide floatation recoveries. Moreover, major commissioning milestone was achieved at the Syama mine with successful automation system acceptance for underground mine. Syama mine’s positive progress was balanced by unplanned roaster maintenance in September and detection of a crack in the roaster in October. It is expected that the roaster will be fully operational by December 2019. The total cost for the repair has been estimated at US$5 Mn, which is expected to be offset by operational cost savings from not operating the roaster during the repair period.

.png)

September’19 Quarter Key Operational Metrics (Source: Company Reports)

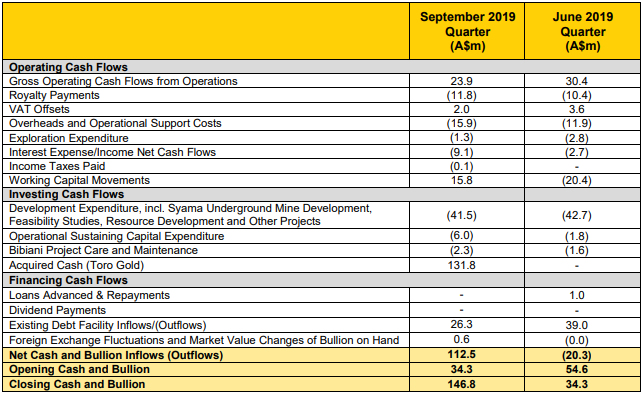

Cash on Hand at the end of Sep’19 Qtr Reported at $116.2 Mn: Company’s cash and bullion balance at the end of September’19 Quarter was reported at $146.8 Mn, as compared to $34.3 Mn in the previous quarter. Cash at the end of the quarter was reported at $116.2 Mn, as compared to $13.2 Mn in the previous quarter, and bullion at the end of the quarter was reported at $30.6 Mn as compared to $21.1 Mn in the previous quarter.

As on September 30, 2019, RSG’s total borrowings stood at A$528 Mn, which comprised US$150 Mn revolving credit facility, acquisition bridge facility of US$130 Mn provided by Taurus, US$58 Mn Mako project loan provided by Taurus, and the net balance of the company’s unsecured overdraft facility with BDM and in-country receivables.

RSG intends to refinance the Toro Gold debt facilities provided by Taurus by paying down the facilities with the significant cash reserves within the Toro Gold capital structure, augmented by an expansion of the company’s existing low cost syndicated revolving credit facility. Completion of the refinance facility will enable the company to simplify its capital structure and complete retirement of both the acquisition bridge and project loans held by Taurus.

Quarterly Cash Flow Statement (Source: Company Reports)

Hedging Position: During the September’19 Quarter, the company hedged 30,000 oz of gold at an average price of US$1,519/oz and was also engaged in some shorter dated hedging.

On September 30, 2019, RSG had an estimated recoverable gold in circuit inventory of 75,311 oz with a market value of ~A$166 Mn. Gold in circuit inventory increased by around 8,000 oz on the previous quarter, mainly due to the Syama roaster being offline during the period, resulting into build-up of available concentrate stocks. The majority of the gold in circuit inventory comprises carbon enriched concentrates stockpiled at Syama.

.png)

Committed Hedging Forward Sales in A$ and US$ (Source: Company Reports)

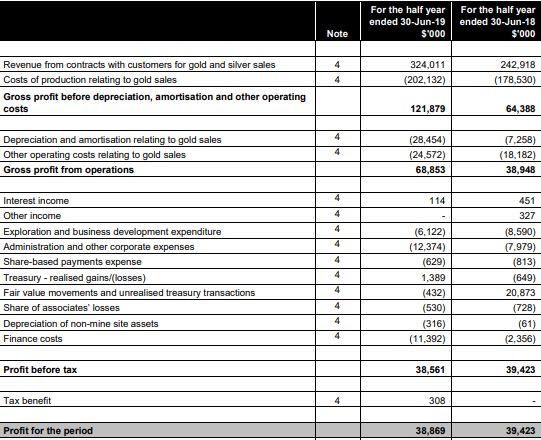

H1FY19 Key Highlights for the period ended June 30, 2019: Revenue from gold and silver sales for the period was reported at A$324 Mn, as compared to A$243 Mn in the previous corresponding period. Gross profit from operations for the period was reported at A$69 Mn, as compared to A$39 Mn in the previous corresponding period. Earnings before interest, tax, depreciation and amortization for the period was reported at A$78 Mn, as compared to A$29 Mn in the previous corresponding period. Net profit after tax for the period was reported at A$39 Mn, in-line with the previous corresponding period. RSG produced 176,237 ounces of gold at an All-In Sustaining Cost of US$828/oz, with total gold sales of 176,294 oz at an average realised gold price of US$1,275/oz.

Cash flow from operating activities was reported at A$95 Mn, an increase of 79% on the previous corresponding period. Total investment in exploration and evaluation was reported at A$6.5 Mn. On June 30, 2019, company’s cash, bullion and investments stood at A$56 Mn, while its borrowings (net of in-country receivables) were reported at A$198 Mn.

H1FY19 Income Statement (Source: Company Reports)

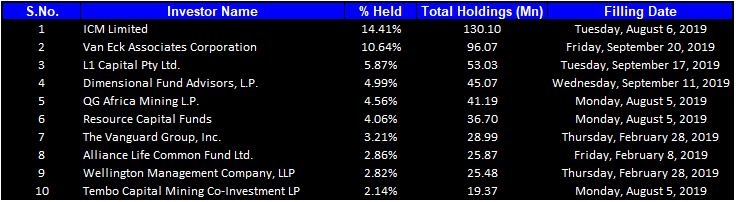

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 55.57% of the total shareholding. ICM Limited and Van Eck Associates Corporation hold maximum interest in the company at 14.41% and 10.64%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

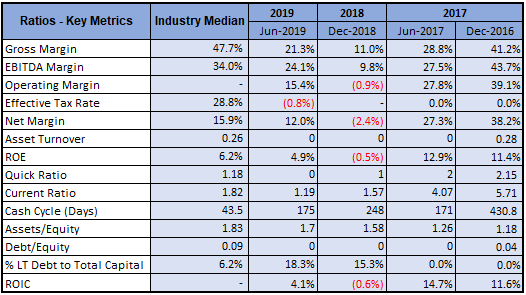

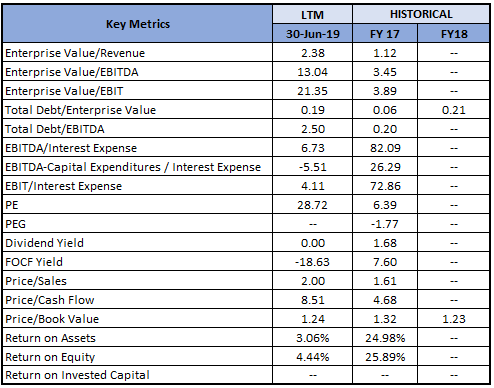

A Quick Look at Key Metrics: Gross margin, EBITDA margin and net margin for H1FY19 stood at 21.3%, 24.1% and 12.0%, better than FY18 result of 11.0%, 9.8%, and -2.4%, respectively, which implies that the company is improving on its profitability margins. Its ROE for H1FY19 stood at 4.9%, better than FY18 result of -0.5%, which implies that the company generated better returns for its shareholders.

Key Metrics (Source: Thomson Reuters)

Key Risks: The company is vulnerable to certain risks such as changes to commodity prices, cash flow and credit risk, fraud and corruption, risks associated with projects across diverse jurisdictions and operating environments.

Changes in Accounting Period: The Group has changed its financial year end from 30 June to 31 December, as a part of the process of seeking a listing on the London Stock Exchange (LSE), and to synchronise the consolidation of Resolute’s African subsidiary companies’ accounts. The financial period for Resolute Mining is now a 12-month financial year, commencing on 1 January and ending on 31 December.

What to Expect: The Company is working hard to offset the lost production from the roaster downtime and, therefore, have not made any change to its existing FY19 gold production guidance, which is expected to be 400,000 ounces of gold. Lost production due to roaster shutdowns adversely affected unit costs for the Syama sulphide circuit for the September’19 Quarter and is expected to affect December’19 Quarter. Consequently, Group’s All-In Sustaining Cost for FY19 is expected to be US$1,020 per ounce as compared to the previous guidance of US$960 per ounce.

The Company is determined to complete the ramp-up of the Syama Underground mine in December’19 Quarter, and to deliver strong positive operating performance for the full year from its mines i.e., Syama, Mako and Ravenswood.

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

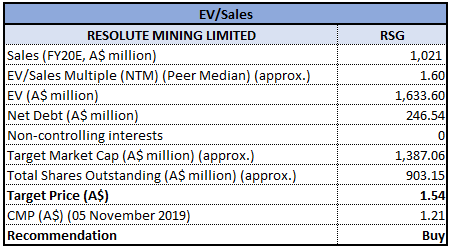

Method 1: EV/Sales Multiple Approach (NTM):

EV/Sales Multiple Approach (Source: Thomson Reuters)

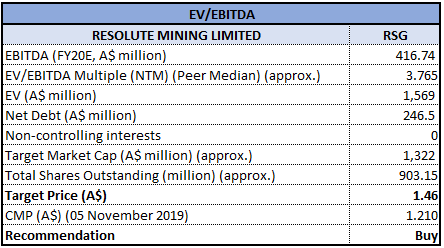

Method 2: EV/EBITDA Multiple Approach (NTM):

EV/EBITDA Multiple Approach (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: At the current market price of $1.210, the stock is presently trading below the average of its 52-week high and low of $2.12 and $0.910, respectively, therefore, proffering an opportunity for accumulation. Company’s top-line and bottom-line for the first half of FY19 improved as compared to FY18 (six months). Despite certain challenges in the Septembe’19 Quarter, the company is determined to be a low-cost, multi-mine African-focused producer and is continuously evaluating a range of growth opportunities. With the successful implementation of Toro Gold, RSG is expected to focus on portfolio enhancing opportunities. Moreover, the company has maintained decent liquidity position at the end of the September’19 quarter, which is expected to help it in pouring funds in its ongoing projects. Looking at the business prospects over the long-term, we have valued the stock using two relative valuation methods, i.e., EV/Sales and EV/EBITDA multiples, and arrived at a target price of lower double-digit growth (in % term). Hence, we give a “Buy” recommendation on the stock at the current market price of A$1.210 per share, down 3.586% as on November 05, 2019.

RSG Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...