Kalkine has a fully transformed New Avatar.

Company Overview: ResMed Inc (ASX: RMD) is a health care company headquartered in San Diego, California, the United States. It provides innovative solutions for the treatment of the people at their home and helps them stay out of the hospital through an out-of-hospital software platform. It allows people to live a high-quality and healthier life. It provides medical devices such as sleep devices, respiratory care devices, masks, etc. which can be connected over the cloud. These devices transform care for people with problems such as COPD, sleep apnea, and other chronic problems. RMD is providing its products to people worldwide in more than 120 countries.The Company produces Continuous Positive Airway Pressure (CPAP), Variable Positive Airway Pressure (VPAP) and AutoSet systems for the titration and treatment of SDB.

.png)

Stocks’ Details

Synergies through acquisition – A growth Catalyst: In FY19, ResMed Inc (ASX: RMD) has acquired many companies and is named as America’s top 100 corporate citizens by Forbes and JUST Capital for the third time in a row. In the US, it is also ranked as 1 out of 32 “Health Care Equipment & Services” companies and 18 out of 890 large publicly traded companies. On 6 July 2018, RMD acquired 100% shares in Healthcarefirst for a total purchase consideration of US$126.3 million. Healthcarefirst is engaged in providing software solutions and services to hospice and home health agencies. The acquisition was funded by drawing on their existing credit facility. RMD recognized goodwill of US$125 million as a part of this acquisition. Healthcarefirst was acquired to support RMD’s on-going software solutions offered by its Brightree. During 2Q19, RMD acquired 100% shares in MatrixCare for a total purchase consideration of US$750.0 million. MatrixCare, a leader in software solutions across life plan communities, skilled nursing, senior living, and private duty. It also started the work with Verily to study the health and financial impacts of undiagnosed and untreated sleep apnea along with the development of software solutions to more efficiently diagnose, identify, treat and manage individuals with sleep apnea and other breathing-related sleep disorders. On 7 January 2019, RMD acquired a digital therapeutics company, Propeller Health (PPH), for US$225.0 million. PPH provides connected health solutions to people having problems like asthma and chronic obstructive pulmonary disease (COPD). During the period, it has also acquired a cloud-based SaaS provides, Apacheta Corporation,through Brightree. Hence, we presume that the formation of strategic alliance with several healthcare companies will provide overall growth of the company in years to come.

.png)

Acquisition with Propeller Health (Source: Company Reports)

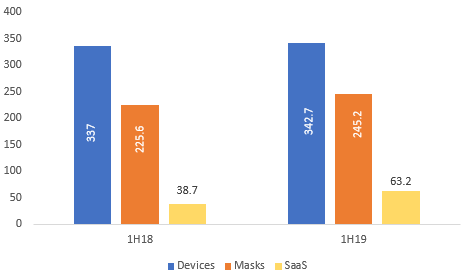

Decent Financial performance during 1H19: The company has recently announced its 1H19 results wherein it reported a revenue of US$1.239 million with a growth of 10% on prior corresponding period (pcp) attributable to strong sales of mask and devices product portfolios in the US, Canada, and Latin America with a growth of 9% on pcp and 1% growth on pcp in Europe, Asia, and other markets. The SaaS revenue also grew by 63% on pcp on account of synergies through the acquisition of Healthcarefirst and MatrixCare. The gross margin of the company was reported at 58.6% with a growth of 70 bps on pcp due to manufacturing and procurement efficiencies as well as acquisition synergies. This has resulted in a growth of 16% on pcp in Income from operations – US GAAP reported at US$301.2 million and a growth of 20% on pcp in Income from operations – Non-GAAP reported at US$338.1 million. It reported a net income of US$230.4 million with a growth of 141% on pcp on account of one-time transition tax recognized in the prior year quarter. Diluted earnings per share (EPS) came in at US$1.60 per share with a growth of 139% on pcp owing to the growth in net income. It reported a free cash flow of US$0.14 billion for 1H19. During 2Q19, RMD paid US$52.8 million as a dividend. RMD cash balance as on 31 December 2018 stood at US$149.47 million with net assets of US$1.956 billion.

Business Segment Breakup in millions (Source: Company Reports)

Dividend to be Paid in March 2019: RMD has declared a quarterly cash dividend payable on 14 March 2019 with a record date of 7 February 2019. For the RMD’s common stock trading on the NYSE, the shareholders will receive dividends in USD. Additionally, the shareholders of Chess Depositary Instruments (CDI) trading on the ASX will also receive a corresponding amount in AUD with an ex-dividend date of 6 February 2019 reflecting the 10:1 ratio between CDIs and NYSE shares, based on the exchange rate on the record date. The ASX’s settlement operating rules have granted a waiver to RMD for deferring the process of conversion between its common stock and CDI registers from 6 February 2019 through 7 February 2019 inclusive.

Ongoing petitions: In August and September 2018, RMD and Fisher & Paykel filed petitions against each other in the United States International Trade Commission for the exclusion of allegedly infringing products by the other. RMD is seeking removal of Fisher & Paykel’s Simplus, Eson, Eson 2 masks and Fisher & Paykel is seeking removal of RMD’s P10 Mask. The hearing for RMD’s case is set for 1 May 2019 and the scheduled date for a discussion is set for 4 March 2020 whereas the hearing for Fisher and Paykel is set for 24 June 2019 and the scheduled date for a discussion is set for 12 February 2020.

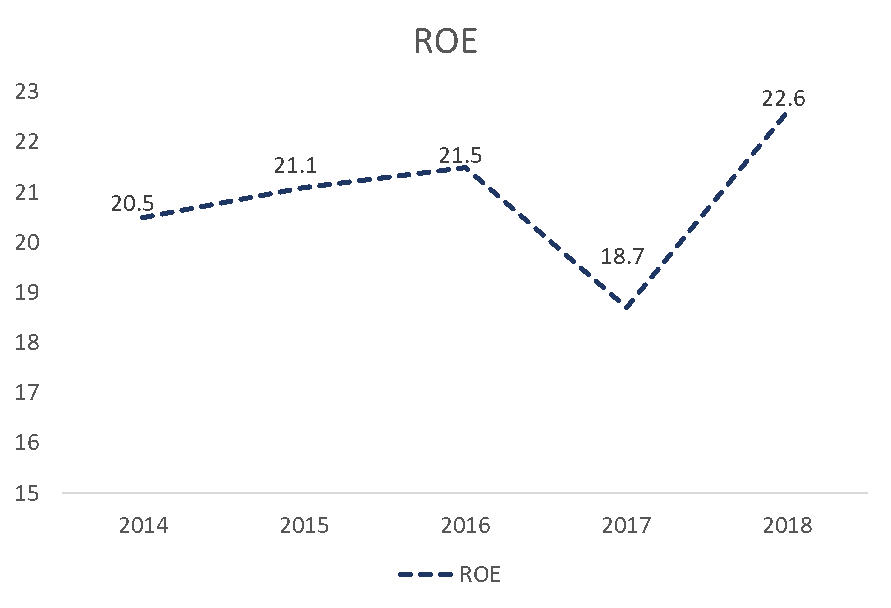

Higher than industry margins: During 2Q19, RMD has reported higher than industry margins showing that the company is generating more profit than most of its peers. The EBITDA margin stood at 30.4% as compared to the industry median of 17.3%. It reported an operating margin of 24.1% as compared to the industry median of 10.9%. Further, the net margin was also higher than the industry median as it stood at 19.2% as compared to the industry median of 6.0%. RMD is able to utilize its assets more efficiently than its peers as it reported a higher than industry asset turnover ratio of 0.19x in 2Q19 as compared to the industry median of 0.17x. Similarly, RMD is generating better returns for its shareholders than its peers as the company reported ROE of 6.5% in 2Q19 as compared to the industry median of 2.0%. It has a favourable capital structure with a debt to equity ratio of 0.61x (in 2Q19). Further, RMD is able to convert its stock to cash more efficiently as it has a better than industry cash conversion cycle of 129.6 days as compared to the industry median of 156 days.

From the valuation standpoint, it has a lower than industry Price/Cash Flow multiple as it reported a multiple of 29.4x as compared to the healthcare industry median of 32.6x. This represents that the stock is undervalued and has a high potential to rise from the cash flow perspective. RMD has approx. 1.42 billion shares outstanding with the market cap of circa $18.68 billion as on 04 February 2019. It has an annual dividend yield of 1.07% with 0% franking. It has a beta of 0.57x (5Y Monthly) showing that the stock has a direct relationship with respect to the index. Further, it is trading at P/E multiple of 43.83x.

RoE Trend (Source: Company Reports)

Stock Recommendation: Over the past few years, the stock had been in an uptrend and has generated a positive return of 5.13% during the last year. But the stock went down by 12.04% the day when the company released its 1H19 results (from A$16.45 on 24 January 2019 to A$14.47 on 25 January 2019) and the effect continued till the next trading session in which the stock further fell by 10.44% (from A$14.47 on 25 January 2019 to A$12.96 on 29 January 2019) leading to a total decline of 21.22% on account of the 1H19 results. The market was estimating a better result and the company was unable to match the industry estimates due to which there was a sudden dip as the global expansion and growth prospects raised certain concerns across investors. This led to the breach of its support level of A$14.00. It is currently trading at A$12.98 with a dip of 0.992% or A$0.13 during the day’s trade (at the close of the market on 04 February 2019). The technical chart, specifically the candlestick chart, shows major gaps in the candles during these two trading sessions which is expected to be filled soon. Even the Relative Strength Index (RSI) is visible in a highly oversold position and the price is currently positioned on the lower band of the Bollinger® band. All these depict a bullish indication.

Meanwhile, RMD stock has fallen by 18.27% during the last month as on 01 February 2019. The company’s stock is trading at its new support level of A$12.96 and has a resistance at around A$16.05 level. With the title under America’s top 100 corporate citizens by Forbes and JUST Capital listing, a rank of 1 out of 32 “Health Care Equipment & Services" companies, significant synergistic acquisition of Healthcarefirst, MatrixCare, and Propeller Health till date in FY19, decent financial results of 1H19 (although lower than the industry estimates), dividend to be paid on 14 March 2019, higher than industry margins, better returns than its peers, favourable capital structure and other fundamentals, and bullish indication through charts, we have a “Buy” recommendation on the stock at the current price of A$12.980.

.png)

RMD Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...