Kalkine has a fully transformed New Avatar.

.png)

Unemployment across the world has remained a consequence of various controllable and non-controllable factors, including a rise in the number of people switching for jobs which match their capabilities better, workforce shifting to remote locations, new graduates currently in search of employment, job-seekers unable to find the desired roles, slowdown in the economy, etc.

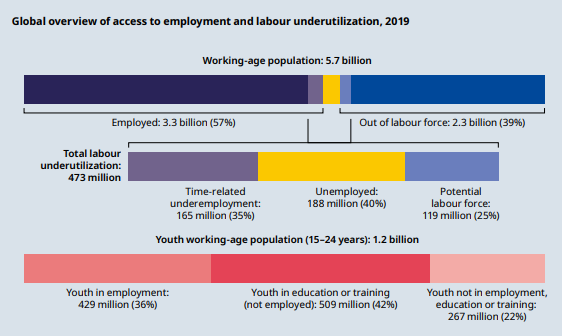

Unemployment Data (2019): As per the information provided by the International Labour Organisation (ILO), an estimated 188 million of the working-age population, i.e., 15 years and older, was unemployed in 2019. This represented around 5.4% of the global labour force, which was similar in comparison to the unemployment rate in 2018. In addition, around 165 million people were not being paid enough for the work and around 120 million had given up the search for work or had no access to the labour market.

The organisation projected that the number of unemployed may increase by around 2.5 million in 2020. ILO also conveyed about the uncertainty of the rate changing as per various economic, financial, and geopolitical risks, as and when they arise.

Unemployment Data (Source: ILOSTAT, ILO Modelled Estimates)

Unemployment Worsens in the Corona-Ridden Era: Due to the current economic downturn amid coronavirus outbreak, countries across the world have been facing multiple economic and social adversities. While the governments are taking steps to curb the spread of the virus and cope with the economic distress as much as possible, there has been a rising threat of the economies witnessing a situation similar to the Great Depression.

Businesses all over the world have come to a halt or are reducing the scale of operations due to increased pressure regarding safety and security of the workforce amid rising health concerns and a massive slowdown in demand. One of the major areas catching sight includes the rising unemployment rate, which has taken a spike due to the current economic situation.

As the situation worsened and countries saw no signs of near-term recovery, the governments issued directives to deal with the novel coronavirus which has taken a toll over economic health. Unemployment took a worse shape as demand worsened and corporates opted for cost-cutting measures. Individuals working across the travel, hospitality and the entertainment sectors were amongst the hardest hit segments, where companies stood down a large number of employees due to negligible revenue generation.

As per recent ILO estimates, nearly 24.7 million jobs can be lost due to the impact of COVID-19, which represents the worst-case scenario of global unemployment. However, considering the potential impact of an internationally-coordinated policy, it has also provided an estimate of the lower limit of unemployment, that stood at 5.3 million. Calculating the mid unemployment scenario led to an estimated loss of 13 million jobs, a substantial part of which will account for high-income countries. The above calculations were based on the 2019 figure of 188 million unemployed people.

Impact on Australia: As the Australian federal government responded to the global health crisis by announcing strict preventive measures, threat loomed over the economic well-being of businesses employing a large section of the population. As bans on travel were imposed, employees working with major airlines had to bear the brunt as they were compelled to take leave without pay. Virgin Australia and Qantas Airways, for instance, have resorted to salary cuts and temporary lay-off to cope with the economic turmoil. The tourism sector has also been on a halt as the incoming of tourists from China, that forms a large section of the tourist population visiting Australia, was completely banned. Other affected sectors include hospitality, retail, nightlife and entertainment.

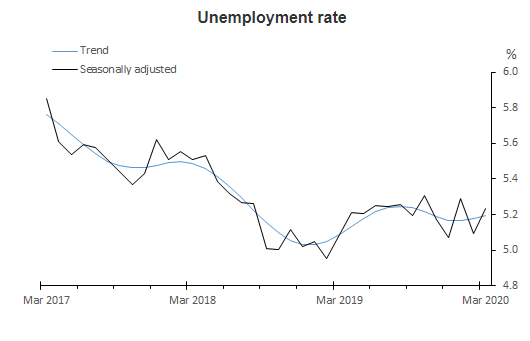

Unemployment Rate in Australia (Source: Australian Bureau of Statistics)

Government Intervenes with a Rescue Package: Unemployment in Australia rose to 5.2% in the month of March, up in comparison to the previous month’s rate of 5.1%. However, the company is yet to see the full impact of COVID-19 on the job market. The above estimates issued by the Australian Bureau of Statistics are an early indicator of the impact from coronavirus outbreak, which will reflect better in the April figures. To keep the unemployment level under control, the government came up with a JobKeeper program in the form of a monetary stimulus package to prevent the situation from spiralling out of control. In response to the crisis, the Australian government has announced a stimulus package worth $130 billion, to protect jobs in the country. Under the package, the government will be paying a fortnightly amount of $1,500 to employers, to curb the adverse impact of COVID-19 related tensions on the job market.

While unemployment rose across the businesses witnessing a slowdown in demand, few sectors faced difficulties in matching the supply and services to the rising demand. For instance, the mere possibility of nationwide shutdown led the households to panic buy essential items for survival, such as food and grocery items and sanitary products. Lately, supermarkets and grocery stores have been seeing a rise in demand for essential household other items and are taking steps to match the supply with the sudden spike in demand. The demand for drivers, nurses, aged care service providers, etc., has been on a rise despite the economic turmoil as essential services remained open. Hence, there is still a section of the corporate world that is offering relief in the form of job creation while the wider job market bears the brunt of the deadly coronavirus. With this scenario, Kalkine is featuring few stocks that have seen a surge in demand for hiring workforce, or have illustrated stability in the prevailing uncertain environment.

(1) BHP Group Limited (Recommendation: Buy, Potential Upside: Lower Double-Digit)

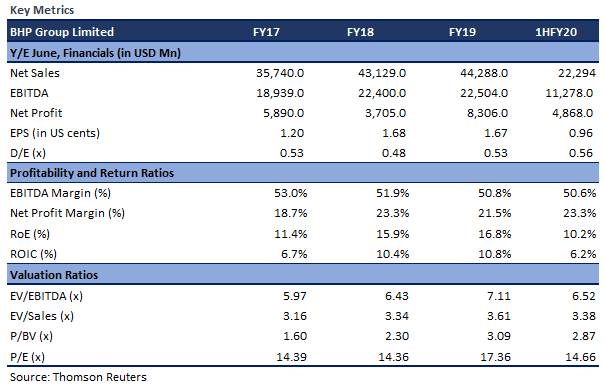

Strong Balance Sheet Position: BHP Group Limited (ASX: BHP) is one of the top producers of major commodities, including iron ore, metallurgical coal and copper. During the half year ended 31st December 2019, the company reported underlying EBITDA amounting to US$12.1 billion, representing an increase of 15% on the prior corresponding period. Free cash flow for the period amounted to US$ 3.7 billion. Over a decade, the company has depicted a stable operating performance, with solid free cash flow generation. With a strong balance sheet and disciplined adherence to capital allocation, the company has managed to maintain a minimum payout ratio of 50%. On 24th March 2020, the company paid an ordinary dividend of US$0.65 per share.

Guidance: For FY20, capital and exploration expenditures are expected to be less than US$8 billion on a cash basis. Petroleum production is expected in the range of 110 – 116 MMboe, with exploration expenditure estimated at US$0.7 billion. Copper and Iron ore production is estimated in the range of 1,705 – 1,820 MMboe and 242 – 253 MMboe, respectively.

While the job market has been under huge distress as businesses begin to lay-off employees or offer leave without pay due to temporary halt in operations, BHP Group Limited took the road towards expansion by hiring around 1500 workers to scale up its mining operations. This represents a great move for the organisation, as well as the Australian economy, as the company supports increase in commodity exports despite the economic fallout. Moreover, some workers of the group have also migrated to their state of work after restrictions imposed on interstate travel.

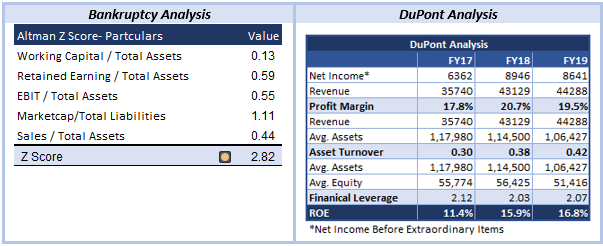

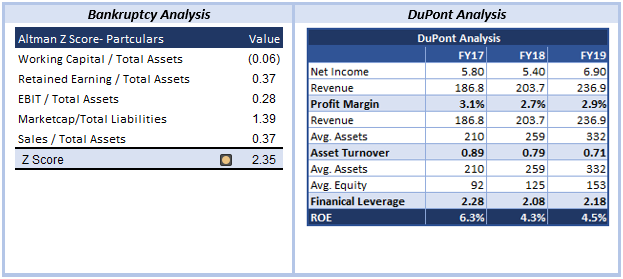

Bankruptcy and DuPont Analysis:

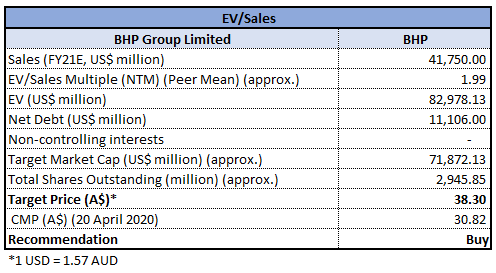

Valuation Methodology: EV/Sales multiple based relative valuation method (Illustrative)

EV/Sales Multiple Based Relative Valuation Method (Source: Thomson Reuters)

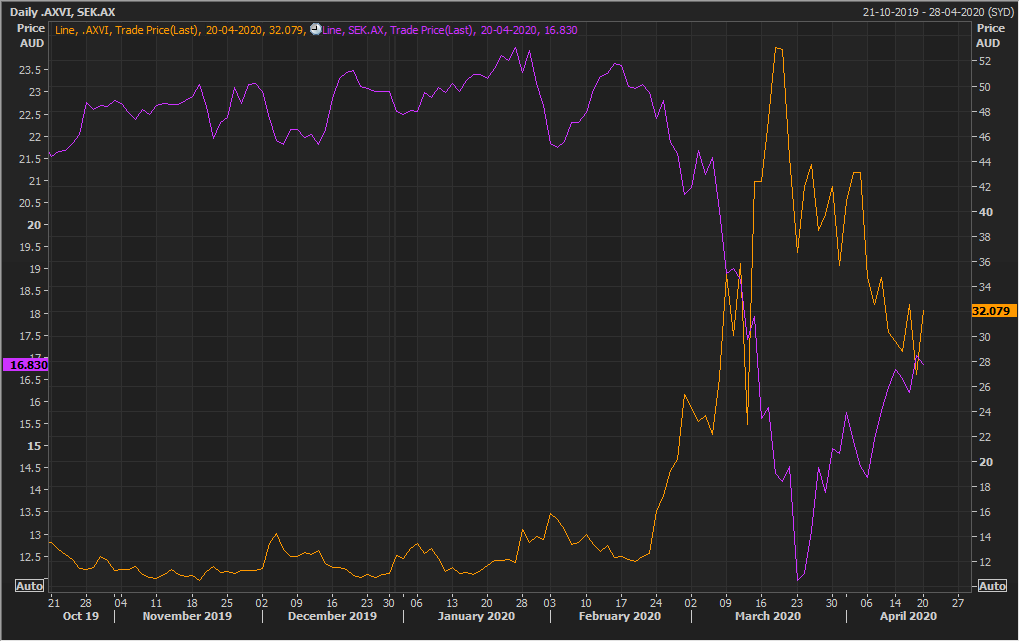

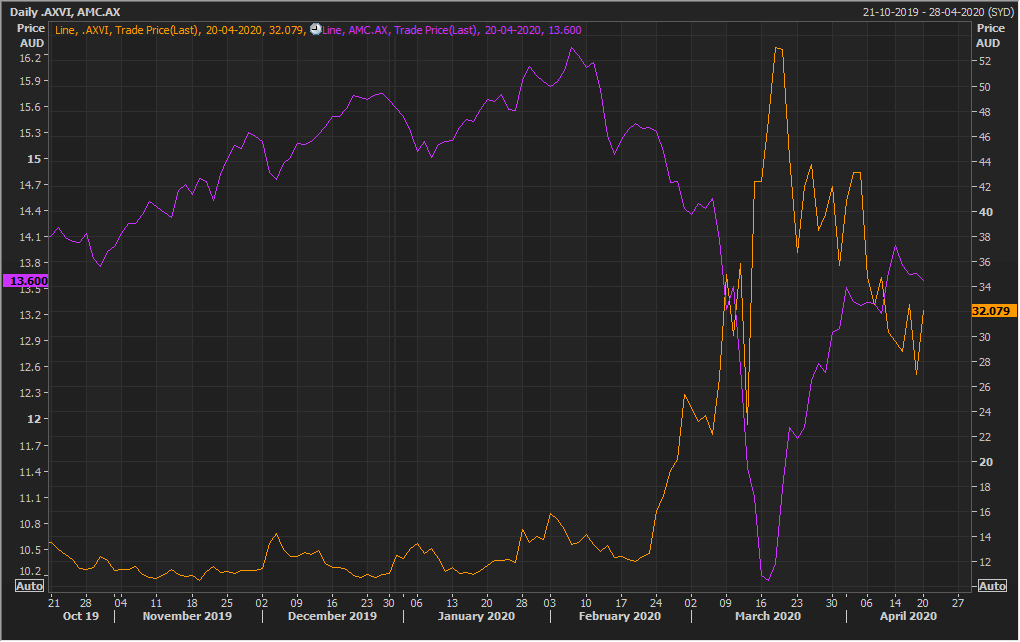

A-VIX vs BHP (Source: Thomson Reuters)

Stock Recommendation: The stock of the company gave positive returns of 10.88% in the past one month. The company has a strong foundation for long-term growth with world-class assets across the best commodities, underpinned by its Capital Allocation Framework. The company aims to place itself as the sector’s best operator and targets to deliver leading financial returns and social value. The company has generated strong operating cash flows over the past few years, which are further utilised to progress attractive growth projects, pay down debt and deliver shareholder returns. As market volatility spiked in March, the stock reacted by a downfall due to the market-wide impact of COVID-19 related factors. In the above chart, we can see that as the market stabilised a bit, the stock price also depicted a quick recovery through an upward movement. Henceforth, we can say that the reaction of the stock price can be considered as a reflection of a decent potential amid the current economic crisis. The company, with its long-term growth strategy and a disciplined approach with respect to doing business, is capable of surviving the current economic downturn. We have valued the stock using EV/Sales multiple based illustrative relative valuation method and arrived at a target price of lower double-digit upside (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $30.820, down 1.471% on 20th April 2020.

2. SEEK Limited (Recommendation: Buy, Potential Upside: Lower Double-Digit)

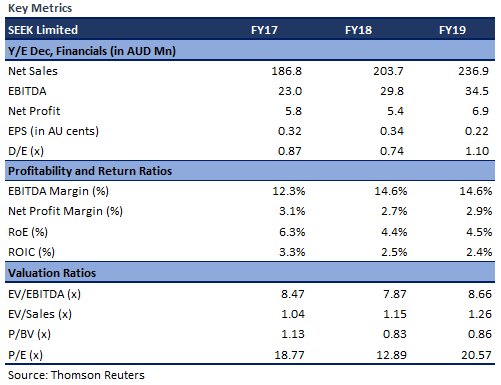

Long-term Outlook Remains Stable: SEEK Limited (ASX: SEK) is a company that matches job seekers with employment opportunities. The company has a presence in 18 countries, employing over 11,000 employees across all locations.

Business Update: Up to the end of February, i.e., the first 8 months of FY20, the SEEK Group excluding Zhaopin, delivered performance in line with expectations. However, the company started witnessing an increasing rate of billing declines during March due to government restrictions in response to COVID-19. Under an illustrative example of FY20 performance based on high-level assumptions, the company expects FY20 revenue and EBITDA to be approximately $1,600 million and $410 million, respectively. However, the company does not intend this to be a guidance or guarantee of future performance.

Outlook: The company has recently updated that it has been experiencing a growing impact of the coronavirus outbreak across its operations. When the outbreak was largely confined to China, the company did not expect any material impact on its operations and issued FY20 guidance based on that assumption. The company is now seeing a direct impact of the virus on its operations, due to which it has withdrawn its previous expectations for the employment businesses. To manage its cashflows, the company has deferred the payment of FY20 interim dividend until 23rd July 2020. The company is focused on both cash preservation and evolving its business models to meet customer needs in the challenging environment.

The management of the company believes that as the current economic pain subsides, job creation will be at the core of recovery, which represents a good opportunity for the business to facilitate the economic recovery process in all its markets through its excellent capabilities and evolving business models. Therefore, with the objective of long-term value creation and ensuring strong long-term business fundamentals, it is expected that the sun will shine brighter on SEK’s business as soon as the recovery begins.

Bankruptcy and DuPont Analysis:

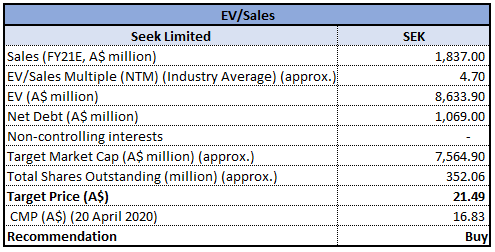

Valuation Methodology: EV/Sales multiple based relative valuation method (Illustrative)

EV/Sales multiple based relative valuation method (Source: Thomson Reuters)

A-VIX vs SEK (Source: Thomson Reuters)

Stock Recommendation: The stock of the company gave positive returns of 7.37% in the past 1 month. While the near-term economic challenges are ought to shake short-term profitability, the company is confident about delivering on its long-term aspirations. It has been taking the required measures to ensure strong liquidity, some of them including, a substantial reduction in discretionary costs, reduction in capital outflows, and deferment of dividend. The stock price tumbled down as market volatility increased in the wake of coronavirus outbreak. However, with the most recent spikes in the market volatility, as depicted in the above chart, the stock has shown some recovery, which can be attributed to the company’s business model and the corrective measures taken to maintain stability across its operations. To reiterate, the company has a strong liquidity position, with a business that will witness high demand as soon as the economy embarks on the journey of recovery. We have valued the stock using EV/Sales based illustrative relative valuation method and arrived at a target price of low double-digit growth (in % terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $16.83, down 1.232% on 20th April 2020.

3. Amcor Plc (Recommendation: Buy, Potential Upside: Lower Double-Digit)

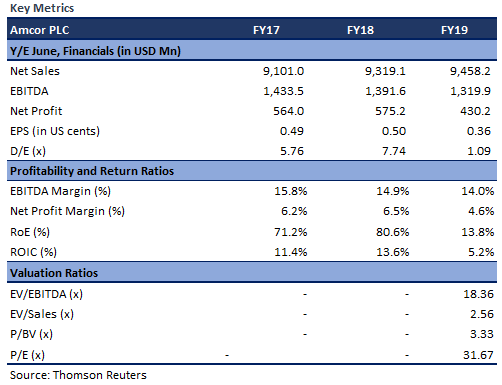

Bemis Acquisition Places AMC as a Global Leader in Packaging: Amcor Plc (ASX: AMC) is a global packaging company employing around 50k people across more than 40 countries. During the six months ended 31st December 2019, the company reported net sales amounting to US$6,183.8 million, up 36% from US$4,545.6 million reported in the prior corresponding period. Gross profit stood at US$1,164 million, up from US$844.6 million in the pcp. Net income also increased to US$255.8 million, from US$242.1 million reported in the prior corresponding half.

Outlook: In June 2019, the company completed the acquisition of Bemis Company, Inc, a global manufacturer of flexible packaging products based in the US. The acquisition places Amcor as a global leader in consumer packaging with a global footprint in key regions of Europe, Asia Pacific, North America, and Latin America. The company is progressing on the Bemis Integration Plan, which is expected to be completed by the end of fiscal year 2022. Total Plan pre-tax integration costs are expected around US$200 million.

While supply chains across businesses have been impacted due to restrictions imposed by the government, the company stands strong with its supply chains being largely local, reducing the reliance on complex international trade. Moreover, the company serves customers in stable and defensive categories of food and healthcare, which are resilient to economic volatility. Henceforth, the risk to employment and the overall performance remains minimal in light of a resilient business model.

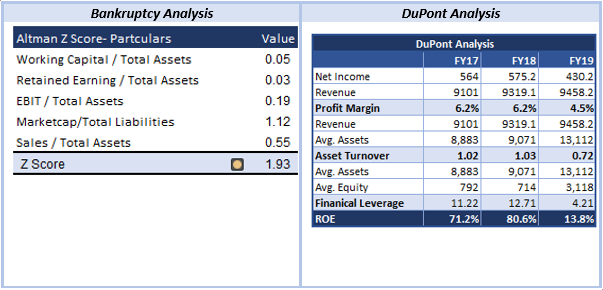

Bankruptcy and DuPont Analysis:

Valuation Methodology: EV/Sales multiple based relative valuation method (Illustrative)

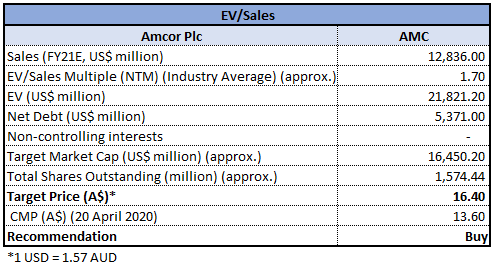

EV/Sales Multiple Based Relative Valuation Method (Source: Thomson Reuters)

A-VIX vs AMC (Source: Thomson Reuters)

Stock Recommendation: The stock of the company gave positive returns of ~34.81% in the past 1 month. The company is now placed as a global leader in the packaging business and possesses excellent research and development capabilities, that can help drive the business forward. The company is targeting for pre-tax synergies of ~US$180 million from the acquisition of Bemis by the end of fiscal year 2022. Initially, the stock price slumped as a result of a spike in market volatility, which is justified as the market witnessed massive panic selling as COVID-19 shock waves were felt in Australia. However, the stock price has recovered fairly after the drop, which speaks volumes about the strength of the business. We have valued the stock using EV/Sales based illustrative relative valuation method and arrived at a target price with an upside of low double digit in percentage terms. Hence, we give a “Buy” recommendation on the stock at the current market price of $13.60, down 0.512% on 20th April 2020.

4. Woolworths Group Limited (Recommendation: Hold, Potential Upside: High Single-Digit)

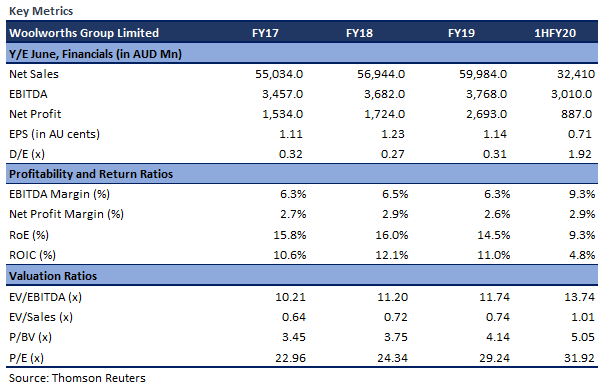

Demand on a Rise: Woolworths Group Limited (ASX: WOW) is primarily engaged in the operation of supermarkets and stores, providing a wide variety of products. During the 27 weeks ended 5th January 2020, the company reported sales from continuing operations amounting to $32,410 million, representing an increase of 6% on the pcp. Group online sales increased by 31.6% and stood at $1,650 million. NPAT from continuing operations came in at $979 million, up 15.7% on the prior corresponding half. Overall, the company delivered sales and earnings growth across all divisions despite a volatile trading environment.

Outlook: Due to the government regulations in relation to COVID-19, the company has closed its Hotels business and is trying to accommodate team members to other businesses of the Group, which remain functional as they are considered as essential services for the community. In fact, the company has seen a spike in demand across its retail business as consumers resorted to panic buying. The company has been working continuously with its suppliers and logistics partners to improve the flow of products into stores. Therefore, on the back of a strong balance sheet, strength of the ANZ food supply chains and a rise in demand, the business is setting the stage for future growth.

As per recent news articles, the company has decided to hire around 20,000 workers to better serve the increase in demand across its stores and scale up its home delivery operations. This is a key highlight of the business’ potential to serve its stakeholders better at the time of crisis, when other businesses are laying-off at a large scale to slash costs. While the existing team members have been relocated to other businesses of the Group, the company is also hiring employees of Qantas Airways, who are currently on leave without pay.

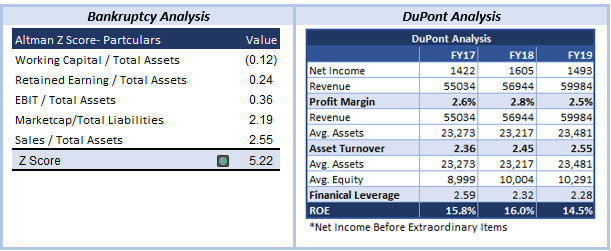

Bankruptcy and DuPont Analysis:

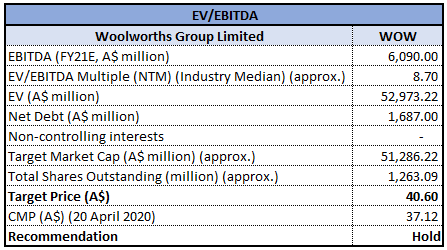

Valuation Methodology: EV/EBITDA multiple based relative valuation method (Illustrative)

EV/EBITDA Multiple Based Relative Valuation Method (Source: Thomson Reuters)

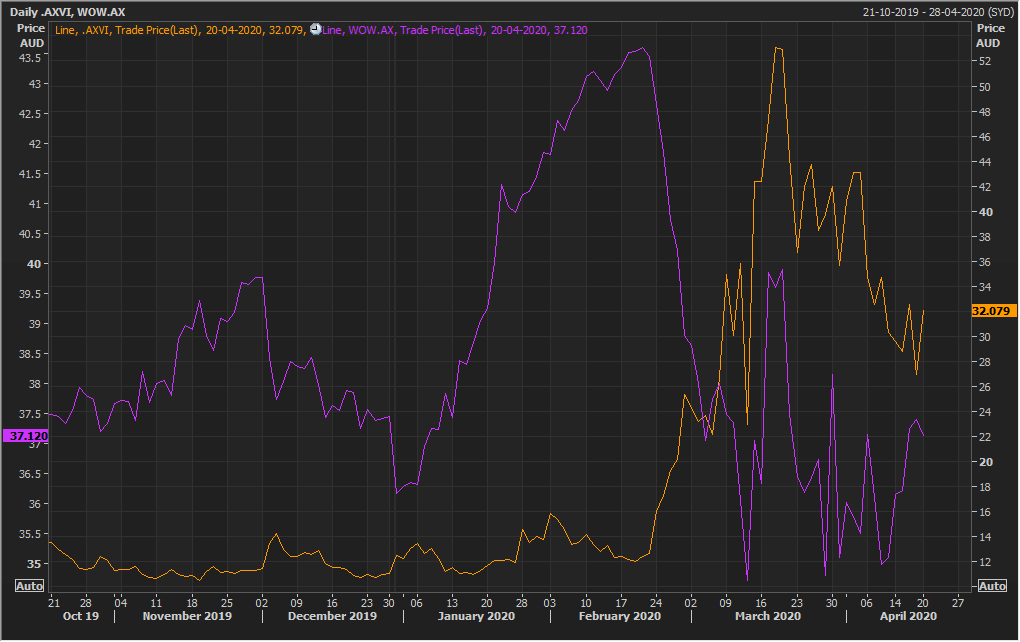

A-VIX vs WOW (Source: Thomson Reuters)

Stock Recommendation: The stock of the company corrected by 6.15% in the past one month. While the company has not been able to provide details on the impact of COVID-19 on performance, due to significant uncertainty with respect to sales and changing patterns in demand, it stands strong with a robust balance sheet, with access to liquidity and funding. The company is backed by its lenders which provide for significant headroom in available facilities. From the chart above, it can be inferred that the stock price has reacted positively to market volatility, as the spike in the market led to a similar movement in the price. This can be attributed to the strength of the business, along with the rising demand for essential products, which will support the top-line growth, going forward. We have valued the stock using EV/EBITDA based illustrative relative valuation method and arrived at a target price with high single-digit upside (in percentage terms). Hence, we give a “Hold” recommendation on the stock at the current market price of $37.12, down 0.749% on 20th April 2020.(1).JPG)

Comparative Price Chart (Source: Thomson Reuters)

Note:

Altman’s Z-Score Model:

(1) When Z-Score<1.81 than it is in Distress Zone

(2) When Z-Score is between 1.81 and 2.99 than it is in Grey Zone

(3) When Z-Score > 2.99 than it is in Safe Zone

The above relative valuation implies a target price incorporating the key positive factors driving the business and indicate long term potential of the stock. Prices, however, remain subject to any short-term movements due to the impact of coronavirus on the business fundamentals.

All the recommendations and the calculations are based on the closing price of 20 April 2020. The financial information has been retrieved from the respective company’s website and Thomson Reuters.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...