Kalkine has a fully transformed New Avatar.

.png)

2019 proved to be a great year for the Australian renewable energy industry, with over 2.2 GW of new large-scale renewable generation capacity added to the grid across 34 projects. This additional capacity represented investment amounting to $4.3 billion and the introduction of 4000 new jobs in the market. Large-scale solar energy comprised almost two-third of this new generation, while the wind sector reported the best year so far in terms of new capacity installed. The energy storage sector also picked pace, with more than 22,000 small-scale batteries installed in 2019, taking Australia’s household storage capacity beyond 1 GWh for the first time.

Composition of Renewable Energy Generation in 2019: 24% of the total electricity generation during the year came from renewable sources, with a record performance in the solar energy space, as the large, medium and rooftop sectors installed more capacity than ever before. The sector saw new capacity addition of 1416 MW during 2019. The wind sector marked its best year with the addition of 837 MW of capacity across 8 new wind farms and accounted for more than 35% of Australia’s renewable energy generation. Hydro power accounted for 25.7% of the total renewable energy generation and was impacted by drought conditions in eastern Australia and growth in other renewable energy sources..png)

Composition of Energy Generation in Australia (Source: Clean Energy Council)

.png)

Renewable Energy Penetration by States (Source: Clean Energy Council)

Significant Job Creation Potential: The renewable energy industry continued to employ a massive chunk of workers in the construction, operations and maintenance and solar rooftop installation functions. Various energy developers in Australia hire locals in the renewable energy industry as part of their social license obligations. However, the full potential for employment is yet to be realised as the industry continues to evolve. Globally, the industry currently employs around 11 million people, which is expected to rise to more than 35 million jobs by 2050. In Australia, the hydrogen industry has the potential for substantial job creation in the coming years.

Corporate Renewable PPAs to Offer Significant Prospects: As the country has met the Renewable Energy Target (RET), the corporate renewables PPA market will provide significant prospects for large-scale renewable energy in 2020. While Australia has a large pipeline of corporate renewable PPAs in development and negotiation, it has suffered a setback in terms of executing deals due to market and regulatory uncertainties such as federal election, grid connection delays and the potential for reductions in wholesale electricity prices. Therefore, to boost such transactions, it is very crucial for the concerned authorities to find a quick solution for the above-stated issues.

The position is not all roses, given the challenges with respect to investment. Worldwide investment in renewable energy was US$363.3 billion in 2019, slightly higher than the figure reported in 2018, with China being the largest investor in renewable energy at US$83.4 billion. As per the clean energy council’s report for 2020, the industry can be put down to growing pains as transmission investment has failed to keep pace with the rapid growth. The impact of this drawback was felt in the West Murray region of Victoria and New South Wales, where several wind and solar farms were forced to curtail their output to maintain grid stability, in 2019.

As per RBA’s research, investment in renewable energy has fallen sharply in 2019, which demonstrates a risky future for the sector. As per the CEO of the clean energy council, the lack of long-term energy policy will continue to disrupt further growth for largescale renewable energy investment. In 2019, the sector faced several challenges due to grid congestion, erratic transmission loss factors and system strength issues, which caused a slowdown in the transition to renewable energy. Such situations call for a quick resolution to restore momentum in the renewable energy space and ensure easy processing of investment for new projects in the rapidly growing industry. Nevertheless, the future of the industry remains bright, with a significant pipeline of renewable energy and energy storage projects and strong customer demand for rooftop solar and batteries. With the potential for massive job creation and the continuously increasing popularity across the globe, the renewable energy industry should be a priority for the Australian government while formulating the COVID-19 recovery plan.

Some of the key players in Australia’s renewable energy space have continued to deliver decent results against these challenges and have built a resilient portfolio of assets as a strong foundation against the current economic uncertainties. Let us have a detailed look at the performance of four energy businesses that appear to be at the forefront of deriving benefits out of the continuously evolving industry.

1. Contact Energy Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 4.09 Billion, Annual Dividend Yield: 6.19%)

High-Quality Renewable Assets to Support Long-term Growth: Contact Energy Limited (ASX: CEN) is a leading provider of electricity, natural gas, broadband, solar & renewable energy. In the recent monthly report for April 2020, the company reported mass market electricity and gas sales of 300 GWh for its Consumer business. Contracted Wholesale electricity sales totalled 548 GWh. In another announcement, the company updated that it has been confirmed as an essential business by the government, enabling continuity of operations. Performance in 1HFY20 was characterised by stronger hydro generation and higher wholesale prices. Despite the difficult operating conditions, the company’s high-quality renewable assets enable the board to declare a dividend of 16 cents per share.

Outlook: The company is focused on delivering on its transformation programme and aims to control costs, while capturing value from scale efficiencies. It is actively engaged in delivering a reduction in carbon footprints of its commercial and industrial customers, by providing low-carbon, reliable electricity. The company has a growing customer base and is expecting decarbonisation-driven demand momentum from its long-term, 13MW, renewable energy agreement. For FY20, the company is expecting to deliver a total dividend of 39 NZ cents per share, in line with FY19..png)

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative).png)

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

.png)

A-VIX vs CEN (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company corrected by 20.94% in the last 3 months and is currently trading below the average of its 52-week trading range of $4.320 - $8.450. During FY19, the company enhanced the quality of its generation assets and improved its balance sheet strength, which will provide significant flexibility across the platform. The stock price was impacted by the spike in market volatility during March and declined at a sharp rate. Since then, it has been on a recovery spree and has shown stable movements recently in response to a relative improvement in market volatility. We have valued the stock using EV/EBITDA multiple based illustrative relative valuation method and arrived at a target price with low double-digit upside (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $5.73, up 0.526% on 18th May 2020.

2. Infigen Energy Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 538.74 Million, Annual Dividend Yield: 3.6%)

Renewable Energy Generation Sales up in April’20: Infigen Energy Limited (ASX: IFN) generates renewable energy from its owned wind farms in New South Wales (NSW), South Australia (SA) and Western Australia (WA). Infigen also sources renewable energy from third-party renewable projects under its ‘Capital Lite’ strategy. The company recently provided an update on the monthly production for April 2020, wherein, production generated from Owned Renewable Energy Assets increased by 6% to 147GWh. On a YTD basis, production increased by 10% to 1,598GWh. Production sold from these assets also increased for both the periods, by 8% and 10%, respectively. Total renewable energy generation sold increased by 12%. During the third quarter ended 31st March 2020, the company reported net revenue amounting to $54.3 million, up 17% on pcp.

Outlook: The company has a strategy to provide Australian commercial and industrial customers with clean energy under firm contracts, backed by its fleet of owned and contracted wind farms, a portfolio of fast-start firming assets and excellent capabilities across the energy market. With a strong financial position, the company aims to take advantage of opportunities as and when the market normalises. Despite the challenges in the renewable energy space, the company is confident about surviving a prolonged period of market disruption with its two credit facilities, including, the Corporate Facility (secured against six owned wind assets and the SA Battery) and the Bodangora Project Finance Facility (secured against the Bodangora wind farm)..png)

Valuation Methodology: P/E Multiple Based Relative Valuation (Illustrative).png)

P/E Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

.png)

A-VIX vs IFN (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company corrected by 21.28% in the last 3 months and is currently trading close to the average of its 52-week trading range of $0.365 - $0.810. In FY20, the company expects to sell ~1.9TWh of renewable energy generation, with asset operating costs estimated between $50-55 million and business operating costs at $25 million. It has a proactive contracting strategy for electricity and Large-scale Generation Certificate (LGCs) which will provide support against the uncertain economic conditions. While the stock price could not escape the turmoil in the market due to COVID-19, it seems to be on a relatively stable ground on the back of a resilient business with a robust financial position. We have valued the stock using a P/E multiple based illustrative relative valuation method and arrived at a target price with low double-digit upside (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $0.560, up 0.901% on 18th May 2020.

3. AGL Energy Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 10.38 Billion, Annual Dividend Yield: 6.7%)

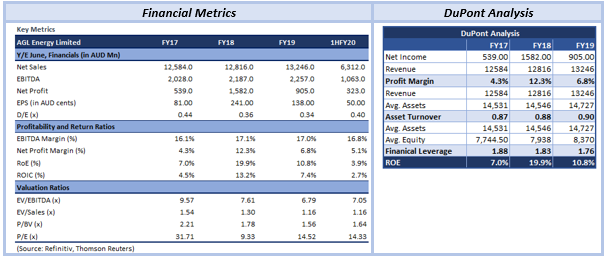

Strong Balance Sheet and Significant Liquidity: AGL Energy Limited (ASX: AGL) is engaged in the operation of energy businesses and investments, including energy generation, gas storage, and the sale of electricity and gas to residential, business and wholesale customers. The company’s operated electricity generation portfolio spans thermal generation as well as renewables and storage, comprising ~20% of the total generation capacity within the National Electricity Market. During the six months ended 31st December 2019, the company reported statutory profit after tax amounting to $323 million, up 11% on pcp and statutory earnings per share of 49.7 cents, up 12% on pcp. During the period, the company declared an interim dividend of 47 cents per share, with a payout ratio of 75% of underlying profit after tax.

Outlook: For FY20, the company expects underlying profit after tax between $780 million - $860 million, maintained despite an increase in customer’s bad debt expense and other unanticipated operating costs arising from COVID-19 lockdown. The above guidance is subject to no further deterioration in market conditions or regulatory impacts on operations. The company has a strong balance sheet and significant liquidity, with ~$1 billion in cash and undrawn facilities. Despite the uncertainty, the company has reported growth in customer metrics by over 28,000 since 31st December 2019, with the lowest churn level in over 4 years amid continued active market conditions. The above factors have strengthened the resilience of the business in uncertain economic and market conditions.

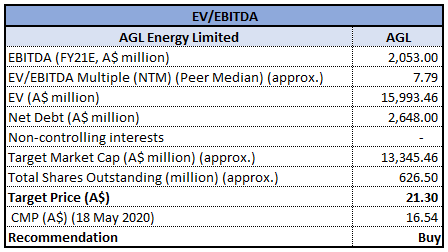

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

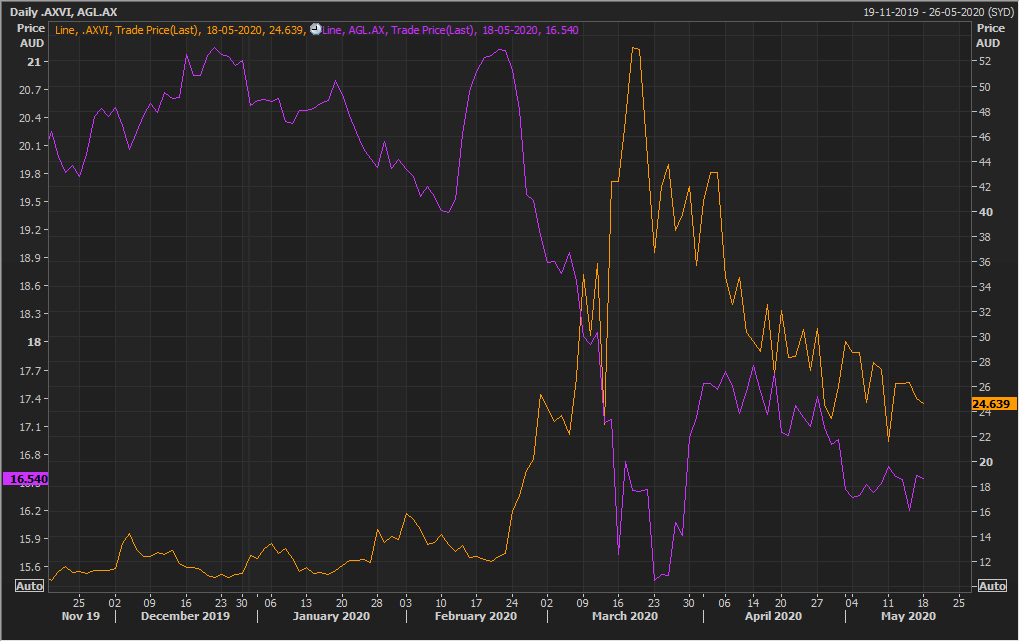

A-VIX vs AGL (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company corrected by 20.68% in the last 3 months and is currently inclined towards its 52-week low level of $15.15. The company is managing well through the current crisis with its strong financial position and the resilience in demand, with essential service cash flows relatively resilient to economic cycles. The stock of the company is gradually recovering from a steep fall after investors resorted to panic selling due to a market fallout. Considering the company’s strong financial position and an optimistic outlook, the stock seems attractive at current levels and can help in maximising wealth over the long term. We have valued the stock using EV/EBITDA multiple based illustrative relative valuation method and arrived at a target price with low double-digit upside (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $16.54, down 0.181% on 18th May 2020.

4. Infratil Limited (Recommendation: Hold, Potential Upside: Low Double-Digit)

(M-cap: A$ 2.87 Billion, Annual Dividend Yield: 3.33%)

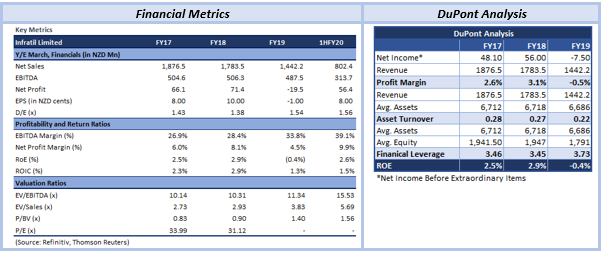

Resilient Portfolio of Energy Generation Assets: Infratil Limited (ASX: IFT) owns renewable energy, airport, data & connectivity and social infrastructure businesses in growth sectors. During the half year ended 30th September 2019, the company reported operating revenue amounting to NZ$802.4 million, up from NZ$736.2 million reported in the prior corresponding year. The increase depicted a full period production contribution from Tilt’s Salt Creek and the impact of higher average spot prices in New Zealand for Trustpower. Net profit after tax came in at NZ$88.1 million. The company has been a regular provider of ordinary dividends since 2013 and declared an interim dividend of 6.25 NZ cents per share.

Outlook: All the portfolio entities are actively managing the crisis and are managing cashflows and discretionary operating expenses and capital expenditure, to mitigate the risks associated. The company has undertaken a significant capital investment in CDC Data Centres, Tilt Renewables and Longroad Energy, which is on track to be income-generating in FY21. On 29th May 2020, the company will be releasing FY20 results for the period ended 31st March 2020.

Over the last 24 months, the company’s investments have been focused on its renewable energy and data & connectivity platforms, which have strengthened its position to deal with any possible adversities in the market. On the other hand, its resilient portfolio will help in deriving the best benefits out of the opportunities that arise in the future. For FY20, the company expects EBITDAF to be between $550 - $560 million, as compared to $575 - $615 million earlier, reflecting the accounting treatment of partial Longroad sales.

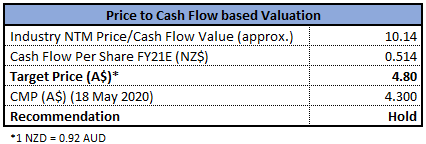

Valuation Methodology:P/CF Multiple Based Relative Valuation (Illustrative)

P/CF Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

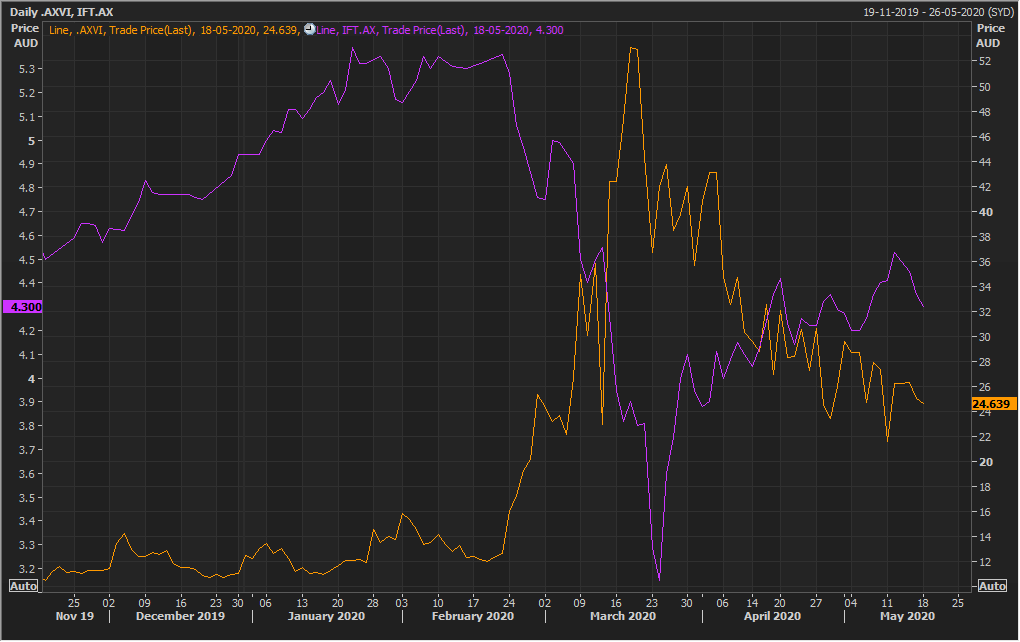

A-VIX vs IFT (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company corrected by 18.23% in the last 3 months and is currently trading above the average of its 52-week low and high level of $3.150 and $5.400, respectively. While the impact of COVID-19 on future performance is unclear, the company has a diversified portfolio of energy generation assets, weighted towards renewable energy generation, which will help it sail through a sustained slowdown in economic activity. The stock of the company has demonstrated remarkable resilience to market volatility, with recovery within no time on the back of a robust business supported by an excellent portfolio of assets. We have valued the stock using a P/CF multiple based illustrative relative valuation method and arrived at a target price with low double-digit upside (in percentage terms). Hence, we give a “Hold” recommendation on the stock at the current market price of $4.30, down 1.149% on 18th May 2020.

.png)

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...