Kalkine has a fully transformed New Avatar.

Company Overview: Reliance Worldwide Corporation Limited (ASX: RWC) is one of the leading manufacturers of water delivery, control and optimization systems for the modern built environment in Australia. The company creates and innovates plumbing products for commercial, residential, and industrial applications and has distinctive end-to-end meter to fixture and floor to ceiling plumbing solutions, which target the repair, renovation, service, new construction and remodel markets. RWC manufactures and distributes products that disrupt and transform traditional plumbing methods by aiming to make the end user’s job quicker and easier and is one the leading manufacturers in the world of brass Push-to-Connect plumbing fittings..png)

RWC Details

.png)

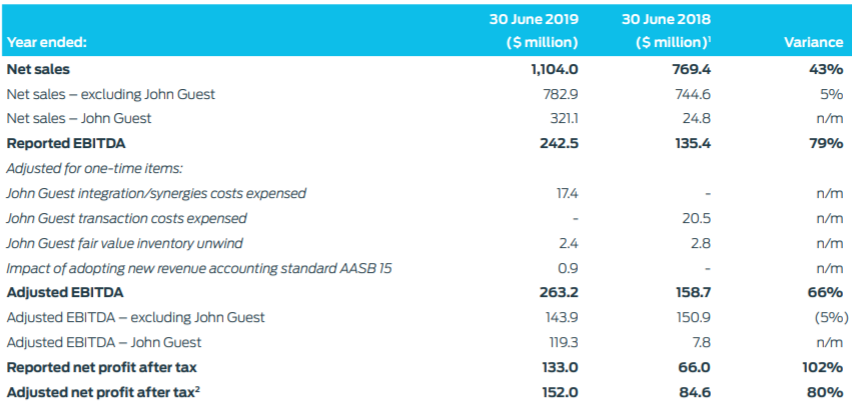

Record Revenue and Sound Balance Sheet: Reliance Worldwide Corporation Limited (ASX: RWC) is engaged in the design, manufacture and supply of water flow and control products and solutions for the plumbing industry. As on 27 April 2020, the market capitalization of the company stood at ~$1.86 billion. During FY19, the company well progressed in bedding down the significant acquisition of the John Guest group. With the addition of John Guest, RWC is much more robust and diverse group of businesses and reported record revenue of $1,104.0 million, reflecting an increase of 43% on the previous year. During the year, operating earnings were up by 79% to $243 million, and NPAT witnessed an increase of 102% to $133 million. This resulted in an increase of 38% in earnings per share. The company continues to finance its activities conservatively to maintain a sound balance sheet. During the year, the company reported an increase in net debt to $427 million, reflecting growth in business activities, including capital expenditure and working capital changes. The decent financial and operational performance enabled the Board to declare a fully franked dividend of 9.0 cents per share, representing a payout ratio of 53% of net profit after tax. The company is also delivering on business opportunities and is targeting additional prospects. RWC is at the forefront and is gaining traction. It has developed the platform for a smart plumbing system that will ultimately lay across its full product offering, from the meter to fixture and floor to ceiling. Over the span of 4 years from FY15 to FY19, the company witnessed a CAGR of 25.03% in revenue and a CAGR of 27.47% in gross profit. This reflects the company’s ability to leverage additional volume through new channels and existing distribution base.

The company has recently released its interim results for the period ending 31 December 2019 wherein it reported strong core businesses and positive growth rates and strong cash generation despite challenging market backdrop. It also made continued improvement in driving operational performance.

The company is optimistic about the future of the core businesses and is expecting growth opportunities from new products. RWC is achieving ongoing above market growth rates for its core Speedfit business in the UK and SharkBite PTC fittings in North America. It intends to invest in various capabilities in the coming year ranging from development and commercialization of the new products, improvement in operational performances and core group capabilities.

FY19 Financial Highlights (Source: Company Reports)

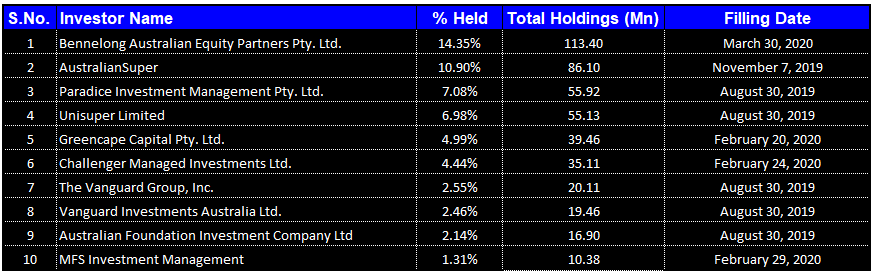

Details of Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of Reliance Worldwide Corporation Limited. Bennelong Australian Equity Partners Pty. Ltd. is the largest shareholder in the company, with a percentage holding of 14.35%.

Top 10 Shareholders (Source: Thomson Reuters)

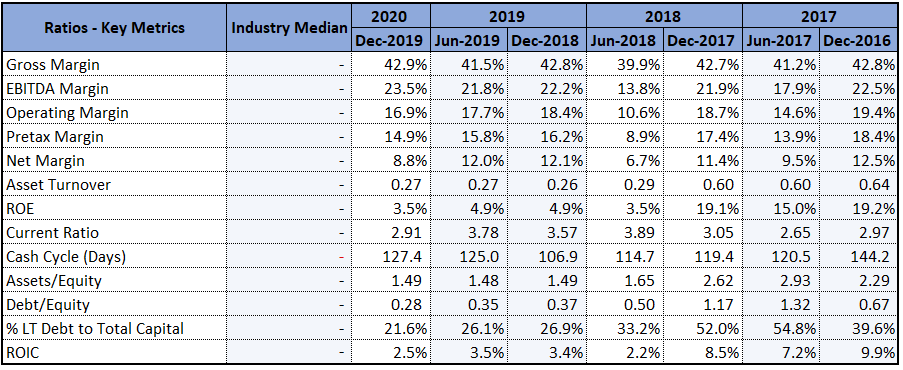

Increased Profitability and Financially Stable Balance Sheet: During 1H20, gross margin of the company witnessed an improvement over the previous half and stood at 42.9% from 41.5% in 2H19. In the same time span, net margin of the company was 8.8%, up from 6.7% in 2H19. The improvement in the gross and net margin indicates that the company is managing its costs well and is capable of converting its revenue into profits. During the half-year, EBITDA margin of the company stood at 23.5% as compared to the previous half margin of 21.8%, indicating increased profitability. In the same time span, Return on Equity of the company was 3.5%, and current ratio stood at 2.91x. During 1H20, Assets/Equity ratio of the company stood at 1.49x, down from 2.62x in 1H18 and Debt/Equity ratio witnessed a decline from 1.17x to 0.28x. This indicates that the business is financed with a more significant proportion of investor funding and a small amount of debt, resulting in a financially stable balance sheet.

Key Margins (Source: Thomson Reuters)

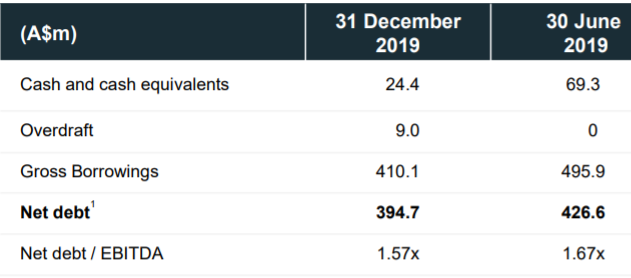

Cost Reduction Benefits and Strong Balance Sheet: The company has recently announced results for the six months ended 31 December 2019 wherein it reported an increase of 5% in net sales to $569.3 million. The growth rate was significantly influenced by currency translation effects. In the same time span, the company reported EBITDA of $126.3 million and NPAT of $50.1 million. During the half-year, RWC continued to realize synergies of $12.3 million from John Guest and is on track to exceed $30 million on a run rate basis by the end of FY2020. The company made continued improvement in various aspects and procured initiatives, delivering $1.5 million in cost reduction benefits and strong g cash generation from operating activities to $112.8 million, up by 163% on the pcp. The company also reported a strong balance sheet with a reduction of $31.9 million in net debt to $394.7 million. It also reported reduced leverage with Net Debt/EBITDA ratio down to 1.57x from 1.67 times. The company continued to invest in new product development and commercialization and is confident in the potential for the long-term success of these new products.

1H20 Debt Metrics (Source: Company Reports)

Segment Performance: The basic revenue driver of the business continues to be the repair, maintenance and remodel sectors in North America and the UK. During 1H20, the company witnessed a growth of over 7.2% in net sales in the region of the Americas to $346.8 million. This was reflective of more typical cyclical and seasonal trading patterns. In the same time span, net sales in the Asia Pacific saw a decline of 3.4% to $125.4 million mainly due to weaker sales into the new housing construction in the Australian market and the expansion of production capacity in the USA. During 1H20, net sales in EMEA were broadly in line with the previous year and stood at $173.6 million with an increase of 18.1% in EBITDA to $52.3 million.

Future Expectations and Growth Opportunities: RWC has solid core businesses in its most crucial and important markets of the USA, Australia, and UK. The company has a strong and robust balance sheet with diverse business across end users, geographic reach, product, channels, raw materials and technology. It has decent fundamentals and has an ability to grow the business ahead of the market. The company is focusing on its core customers and is recalibrating its approach to new products and solutions. RWC will continue to engage in opportunities to drive further efficiency enhancements and to optimize manufacturing footprint.

The company continues to closely monitor the manufacturing volumes for meeting the sales demand. Given the rapidly changing COVID-19 situation, RWC maintains a global supply chain and robust inventory positions and is confident in its ability to service customer needs. The company has significant funding lines to manage its working capital and cash flow requirements.

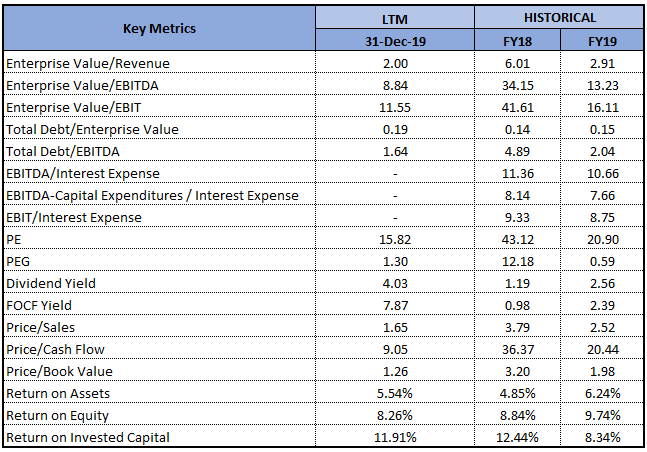

Key Valuation Metrics (Source: Thomson Reuters)

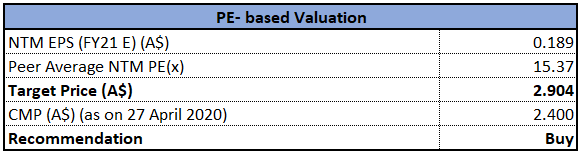

Valuation Methodology: Price to Earnings multiple based relative valuation approach (Illustrative)

Price to Earnings multiple based relative valuation approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of RWC gave a return of 35.63% in the past one month and is trading close to its 52-weeks’ low level of $1.630. This offers a decent opportunity for accumulation. The company has decent fundamentals and hence is expected to deliver strong earnings and a platform for growth. RWC is looking to fully leverage its relationships with end users in the UK and have real opportunities further expand into residential new construction, commercial pipe fittings and commercial valves. Considering the trading levels, decent returns in the past one month, decent fundamentals and positive outlook, we have valued the stock using the price to earnings multiple based relative valuation approach and have arrived at a target price offering an upside of lower double-digit (in percentage terms). Hence, we recommend a ‘Buy’ rating on the stock at the current market price of $2.40, up by 1.695% on 27 April 2020.

RWC Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...