Kalkine has a fully transformed New Avatar.

Company Overview: Reece Limited (ASX: REH) is a leading supplier of plumbing, bathroom, heating, ventilation, waterworks, air conditioning and refrigeration products with operations in Australia, New Zealand and the US. The segments of the group are based on the geographical operations of the business and comprise Australia and New Zealand (ANZ) and the United States of America (USA). Reece Limited supplies customers in the trade, retail, professional and commercial markets. The Reece Group in Australia and New Zealand will continue to focus on investing in people, products, technology, and customer service. In the US, the focus is on developing the long-term strategy and culture and positioning the US business to benefit from the growth opportunities in the Sun-Belt region.

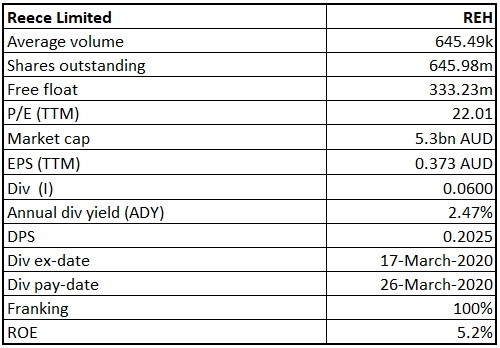

REH Details

Record Revenue and Strong Balance Sheet: Reece Limited (ASX: REH) is a leading supplier of plumbing, bathroom, heating, ventilation, waterworks, air conditioning and refrigeration products with operations in Australia, New Zealand, and the US. As on 11 May 2020, the market capitalization of the company stood at ~$5.3 billion. 2019 has been a year of strength for the company as it explored new growth opportunities. During FY19, the company achieved record sales revenue of $5,464 million, up by 103% on the prior year including a full 12-month contribution from MORSCO. In the same time span, normalized earnings before interest, tax, depreciation, and amortization improved by 38% to $522 million and normalized net operating profit after tax witnessed an increase of 6% to $238 million. Over the span of 4 years from FY15 to FY19, the company witnessed a CAGR of 27.23% in revenue and a CAGR of 22.28% in gross profit. This indicates the continued decent performance of the company in a slowing environment. The decent financial and operational performance enabled the Board to declare a fully franked dividend of 14.25 cents per share for the second half of the year, bringing the total dividend to 20.25 cents for FY19. Driven by a strong culture, deep experience and focus on the customer, REH has built on a leading market position and has grown into new market segments. The company remains focused on its Australian business and continue to invest in the people, products, technology, and customer service it is known for. The company has also reported a strong and healthy balance sheet which gives the company confidence to pay down the debt facility used to acquire MORSCO.

The company has also released its interim results for the period ending 31 December 2019, wherein it reported record results in its next chapter. The company has laid the foundations for its business through the expansion in the US and via competitive advantage in Australia and New Zealand through investment in technology and innovation.

The integration of the company with MORSCO continues to be on track as per the company’s planning, with a focus on developing the long-term strategy and culture and positioning the US business to take full advantage of the growth in the Sun-Belt region. The company has drawn strength from its underlying business model, and as the Australian market entered a more challenging market domestically, REH continued to focus on helping its customers to flourish in a slower economic environment.

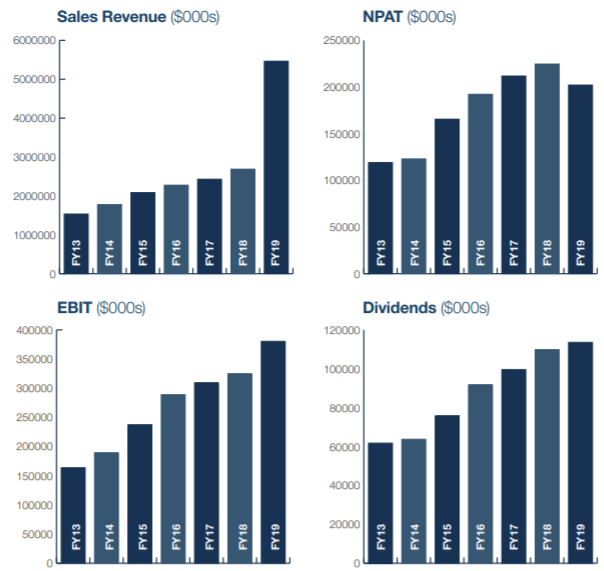

FY19 Financial Highlights (Source: Company Reports)

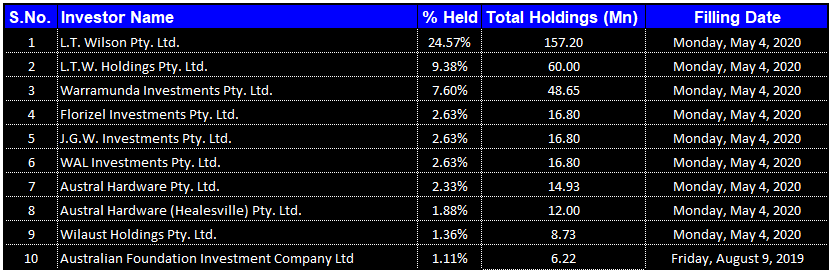

Details of Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of Reece Limited. L.T. Wilson Pty. Ltd. is the largest shareholder in the company, with a percentage holding of 24.57%.

Top 10 Shareholders (Source: Refinitiv, Thomson Reuters)

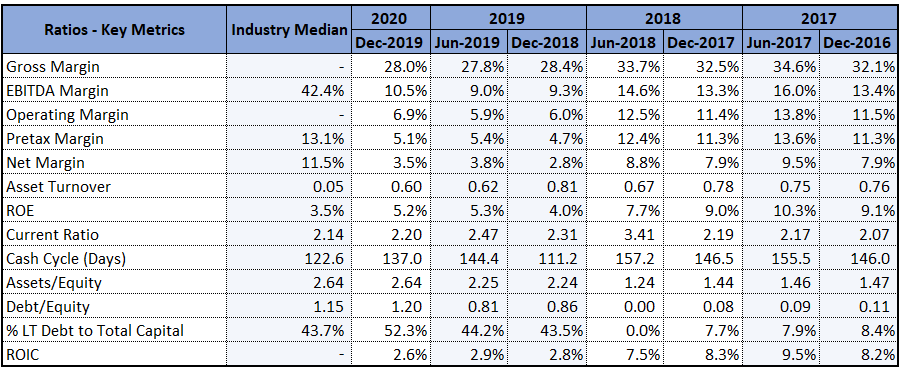

Increased Profitability and Returns to Shareholders: During 1H20, gross margin of the company witnessed a slight improvement over the previous half and stood at 28%, up from 27.8% in 2H19. In the same time span, net margin of the company saw an increase over the previous year and stood at 3.5%, up from 2.8% in 1H19. The improvement in gross and net margins of the company indicates that the company is well managing its costs and is capable of converting its revenue into profits. During the half year, EBITDA margin of the company went up to 10.5% from 9% in 2H19, indicating increased profitability. In the same time span, Return on Equity of the company stood at 5.2%, higher than the industry median of 3.5%. This indicates that the company is well managing the capital of its shareholders and is capable of generating profits internally. During the half year ended 31 December 2019, current ratio of the company was 2.2x, slightly higher than the industry median of 2.14x. This shows that the company is liquid enough to pay off its current liabilities using its current assets. In the same time span, assets/equity ratio of the company was in line with the industry median and stood at 2.64x with debt/equity ratio of 1.20x.

Key Margins (Source: Refinitiv, Thomson Reuters)

Expansion in Global Footprint and Decent Increase in NPAT: During 1H20, the company has achieved record sales revenue of $2,962 million, representing an increase of 9% on the prior corresponding period. In the same time span, normalized EBITDA was up by 1% to $263 million from $260 million in 1H19, and normalized NPAT grew by 7% to $113 million from $106 million in 1H19. During the half-year, the company continued to deliver customized service by providing quality products and building strong relationships and expertise, and by investing in innovation and technology. During the half-year, MORSCO sales revenue was up by 19% to $1,496 million. The business is developing its new store approach, which will ultimately guide the long-term approach for the network across the growing Sun-Belt region. During the first half of FY20, ANZ footprint expanded with the addition of five new branches, bringing the total to 639. The Board has declared a fully franked interim dividend of 6 cents per share, which was paid on 26 March 2020.

1H20 Financial Highlights (Source: Company Reports)

Completion of Retail Entitlement Offer and SPP: The company has successfully completed the retail component of its fully underwritten pro rata accelerated non-renounceable entitlement offer. The completion of the retail component and the SPP represents approximately $647 million equity raising. Proceeds from the equity raising will be used to enhance balance sheet flexibility, support the business during the current macro-economic uncertainty and materially increase liquidity and reduce net debt. The company has recently announced changes to its leadership structure to accelerate its long-term growth strategy. As per the changes, the Reece Group Leadership Team will consist of a Group CFO, CEO US, and CEO ANZ. As a part of these changes, the leadership team will look to leverage synergies across both regions and accelerate the long-term strategy of the company.

Future Expectations and Growth Opportunities: Despite the slowdown in Australian headwind, the company continues to deliver strong results and long-term value as a global company. The MORSCO integration is on track, and the company is focusing on developing the long-term strategy and culture and positioning the US business to take full advantage of growth in the Sun-Belt region. REH has also centered its presence in New Zealand, providing customers with a stronger and more wide-reaching offering, essential to long-term success and growth in the country.

The company is leveraging its industry leading technology, expertise, and service across the Reece group to build market share. REH has introduced the Reece Service Standards and online customer tool and has quickly adapted and championed the transformation. The company is providing consistent, quality experience across all branches. It is focusing on pursuing its operating strategy to create shareholder value.

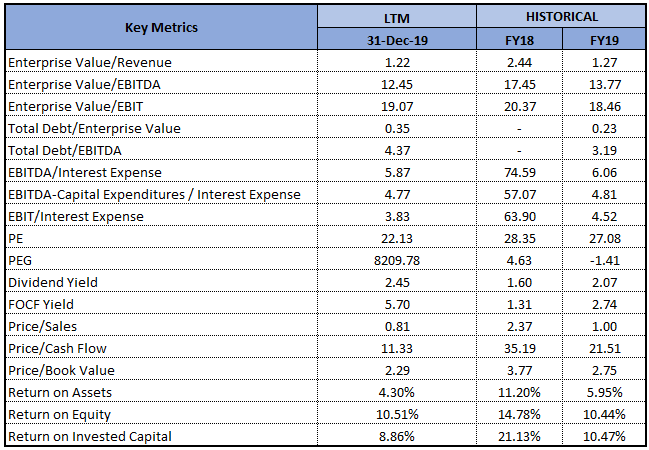

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

Valuation Methodology: EV/Sales Multiple Based Relative Valuation Approach (Illustrative).png)

EV/Sales Multiple Based Relative Valuation Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of REH is trading close to its 52-weeks’ low level of $7.7, proffering a decent opportunity for accumulation. The company is maintaining its competitive advantage and is developing a new store approach. It has started delivering customized service and is building strong relationships with its customers. The company has built its liquidity levels and is managing risks to set itself for success in the long term. The recent equity raise will enable the company to navigate through current market uncertainties from a position of strength. Considering the trading levels, decent liquidity levels and positive long-term outlook, we have valued the stock using EV/Sales multiple based relative valuation approach and have arrived at a target upside of higher single-digit (in percentage terms). Hence, we recommend a ‘Buy’ rating on the stock at the current market price of $8.37, up by 1.949% on 11 May 2020..png)

REH Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...