Kalkine has a fully transformed New Avatar.

Company Overview: Redbubble Ltd is an Australia-based company, which operates an independent designers' marketplace. For men, the Company offers T-Shirts, Classic T-Shirts, Tri-blend T-Shirts, Graphic T-Shirts, V-Neck, Long Sleeves, Tank Tops, Hoodies, Lightweight Hoodies, Sweatshirts and Lightweight Sweatshirts. For women, it offers T-Shirts, Chiffon Tops, Contrast Tanks, A-Line Dresses, Graphic T-Shirt Dresses, Fitted Scoops, Fitted V-Necks, Relaxed Fit, Tank Tops, Hoodies, Leggings, Scarves and Mini Skirts. For kids, the Company offers Kids T-Shirts, Baby T-Shirts and Baby One-Pieces. The Company also offers cases and skins, such as iPhone Cases, iPhone Wallets, Laptop Skins and Laptop Sleeves; stickers; wall art, such as Posters, Canvas Prints, Photographic Prints, Art Boards and Art Prints; home decor, such as Throw Pillows, Duvet Covers, Mugs and Clocks; stationery, such as Greeting Cards, Postcards and Calendars, and bags, such as tote bags, drawstring bags and studio pouches.

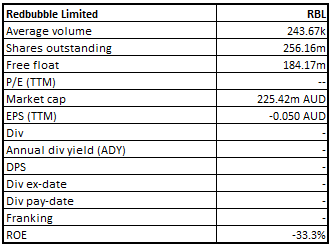

RBL Details

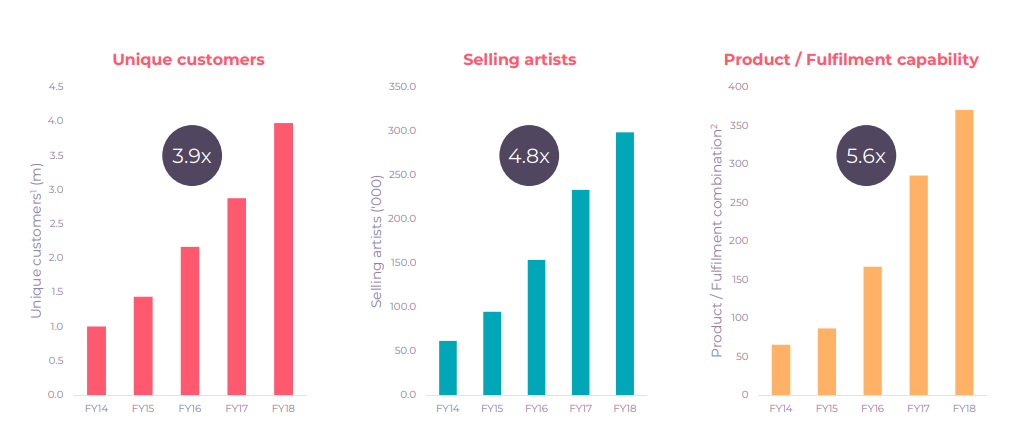

FY 2018 Results Aided by Robust Marketplace Dynamics: Redbubble Limited (ASX: RBL) happens to be a global online marketplace which is having the market capitalization of ~$225.42 million as of January 29, 2019. The company had been encountering strong growth with regards to the key financial metrics. Coming to the company’s management, Mr. Barry Newstead is the CEO (or Chief Executive Officer) and the Managing Director of Redbubble Limited. It had earlier published its results for FY 2018 and the company posted GTV or Gross Transaction Volume amounting to $231.3 million which reflects the YoY growth of 31.9%. The growth with regards to the top line in FY 2018 (especially second-half) was aided by the robust marketplace dynamics. During the same period, the company’s mobile GTV stood at $89.8 million which implies the YoY growth of 57.1% thanks to the performance of iOS App. Further, over the span of previous five years to FY 2018, the company encountered robust performance with respect to unique customers, selling artists as well as product/fulfilment capability.

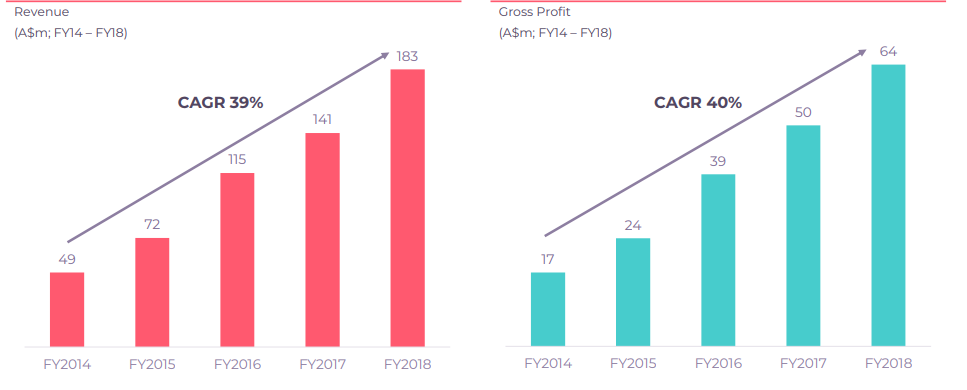

Over the five-year period to FY 2018 (FY2014-FY2018), the company had showcased robust growth of 39.26% (CAGR) with respect to the revenues which further strengthens the confidence in the company’s performance. Moreover, over the past five years to FY 2018, the company has been witnessing uptrend with regards to its revenues. However, the company had also witnessed a rise of 1.4% in FY 2018 in the EBITDA margin to -3.9%. Its operating margin also stood at -8.2% which implies the rise of 1.8%.

The company stated that broader marketplace is sensitive to the 3 global trends like the rise of sharing economy which supports artists in terms of sharing the creativity to the customer base on a global basis. The other two global trends happen to be a rise in consumer demand for the personalization as well as self-expression and the improvement with regards to the print-on-demand and manufacturing-on-demand technology’s capability.

Key Metrics (Source: Company Reports)

Improvement in Gross Profit Margin: Redbubble Limited ended FY 2018 with the growth of 32.2% in GTV on the YoY basis and the constant currency basis which happens to be according to the guidance. The company’s gross profit margin in the second half stood at 35.5% thanks to the scale as well as the improvement with regards to the unit economics. The company had incurred operating expenses amounting to $51 million in FY 2018 reflecting the rise of 19.3% on the YoY basis because of the company’s business scaling objectives. There has been robust momentum in the company’s revenues and gross profit thanks to the company’s focus towards scaling the business.

Growth in Revenues and Gross Profit (Source: Company Reports)

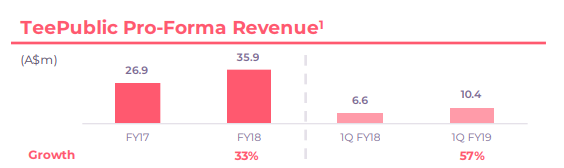

Insights on TeePublic Acquisition: Not so long ago, Redbubble Limited discussed the details related to the acquisition of TeePublic in the AGM 2018. The company stated that TeePublic would support the market presence of RBL as it would help in working with the more independent artists. There happens to be robust cultural as well as strategic alignment between the RBL and TeePublic and also there are opportunities for the synergies. The combination is expected to support in terms of market coverage as well as in improving the competitive positioning. It would also help in terms of joint competitive as well as supply chain positions with respect to the core markets of the United States. Moreover, the acquisition would also aid in creating the opportunities for the achievement of the operating leverage with the help of shared technology as well as investments. TeePublic also possesses a robust financial profile as the company posted pro-forma growth in the revenues of 33% in FY 2018 while in Q1 FY2019 the growth stood at 57% as compared to the Q1 FY2018. Moreover, TeePublic also works on the business model which possesses lower capital expenditure, consistent with RBL, and this would support in terms of the free cash flows. Talking about the financial impact, in FY 2019, RBL might witness growth in the revenues at a faster pace as well as it might witness increased gross margins because of TeePublic’s acquisition as TeePublic possesses attractive financial profile.

TeePublic Pro-Forma Revenue (Source: Company Reports)

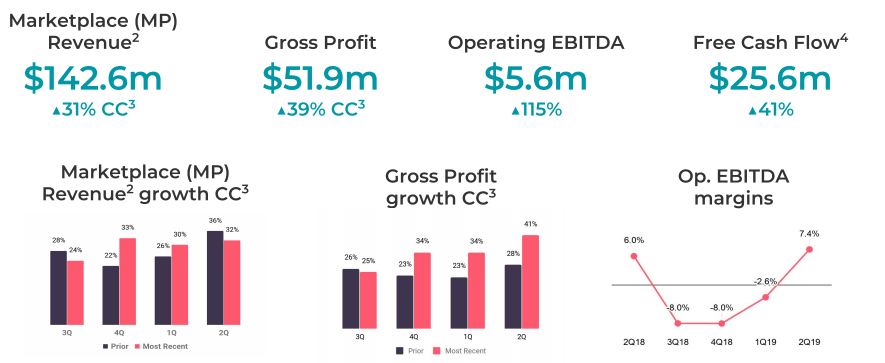

RBL Ends Half-Year of FY19 with Positive Operating EBITDA: Redbubble Group managed to post operating EBITDA amounting to $5.6 million while the FCF (or Free Cash Flow) amounted to $25.6 million in H1 FY2019 ending December 2018 and this builds confidence that the company might achieve the positive results for both the metrics in FY 2019. The company’s 1H FY 2019 results were supported by the member growth, TeePublic acquisition as well as improvement with regards to the margins. RBL, as well as TeePublic, happen to be seasonal businesses and the company had witnessed significant holidays in Q2. In the December 2018 quarter, the company witnessed receipts from the customers amounting to $120.3 million and its net cash from the operating activities amounted to $26.6 million.

In H1 FY 2019, the company’s gross margins witnessed the favourable momentum on the back of supply chain gains as well as strategic pricing, and the company had managed to maintain discipline with regards to operating expenses as well as it maintained efficiency with regards to paid marketing. The company’s gross profit margin stood at 36.4% which implies the YoY rise of 1.9%. In H1 FY 2019, the company posted marketplace revenues amounting to $142.6 million which implies the rise of 31% on the constant currency basis.

The company witnessed the robust performance in Q1 FY 2019 while in the Q2 FY 2019, the company posted weaker growth with regards to revenues because of the impact of Google algorithm on the organic search sales. However, the growth in the revenues got aided by revenue strength with respect to the paid channels and TeePublic’s inclusion for the months of November 2018 and December 2018. The company added that its operating costs stood in line with the anticipations as the company had worked towards controlling the costs.

RBL Financial Summary for H1 FY2019 (Source: Company Reports)

Drivers for Future: In FY 2019, Redbubble Limited would be working towards growing the customer base and it would remain focused on launching and selling products which the artists want to design as well as accepted by the customers. Moreover, the company would also be working towards further improving the relationships with authentic artists. As reflected by the company’s half-year to December 2018 update, the company has been carrying out activities which are targeting improvements with regards to core customer experiences to support the company in terms of organic search sales.

Redbubble Limited would also be witnessing the growth in the revenues with the help of content partnerships, pricing strategy work as well as roll out with regards to new products. In H2 FY2019, the company would be supported by its scale via better fulfilment costs. The company would also be focusing on growth with regards to the paid marketing. Finally, in FY 2019, the company is expected to post positive cash flow result as well as positive operating EBITDA on the back of aforesaid factors.

Stock Recommendation: On the daily chart of Redbubble Limited, Moving Average Convergence Divergence or MACD has been applied and default values were considered for the purposes. After carefully observing, it was noticed that the MACD line has crossed the signal line and is moving in the upward direction which reflects bullish momentum. Therefore, the stock might witness an uptrend. Also, Exponential Moving Average or EMA has been applied, and default values were used for the purposes. It was noticed that the stock price has crossed the EMA and is trending in the upward direction which also reflects that the stock might witness bullish momentum moving forward.

Fundamentally, the company is expected to benefit from the TeePublic’s acquisition. There are expectations that the company would post positive operating EBITDA as well as cash flow result in FY 2019 which looks attractive. However, the company’s net margins have witnessed a decline of 0.1% in FY 2018 on the YoY basis and stood at -5.5%; but these are expected to improve going forward. Talking about the company’s stock performance over the past few months, Redbubble’s stock delivered the return of -43.16% in the past 6 months. However, in the time span of the previous three months and one month, the stock posted the return of -39.52% and -5.38%, respectively. Given the backdrop of aforesaid facts and current trading scenario, we give a “Speculative Buy” recommendation on the stock at the current market price of A$1.015 per share (up 15.341% on January 29, 2019).

RBL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...