Kalkine has a fully transformed New Avatar.

Company Overview: ReadyTech Holdings Limited is an Australia-based company, which is focused on developing education software. Its segments include Education segment and Employment segment. It offers a range of products for Education, such as JR Plus, VETtrak, A2E and My Profiling. Its products for Employment includes HR3, Aussiepay and ePayroll. Its products for Pathways includes JR Live, JR Active, JR Gov and Esher House. JR Live platform for job active and DES programs enabling caseworkers to match job seekers with vacancies, manage work placements, provide post-placement support (PPS) and track job outcomes. JR Active platform is integrated with Government systems and helps support career advice, administer training contracts and incentives to employers, monitor apprentices and provide business intelligence tools to inform decision making. VETtrak software offers short message service (SMS) for small to medium-sized private VET providers.

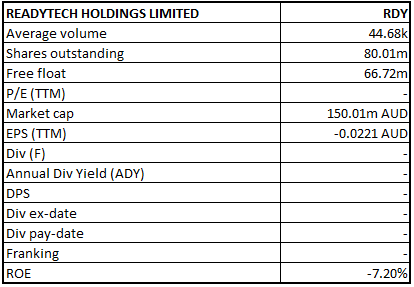

RDY Details

Continued Growth in Average Revenue Per Client: ReadyTech Holdings Limited (ASX: RDY) is primarily engaged in the provision of software-as-a-services (SaaS) for the education and employment sectors. Under education, the company provides a student management system to vocational education and training, international and English language, and higher education providers. Employment services provided by the company, include payroll and employee management solutions from cloud-based technology to the outsourcing of human resource function. The company was listed on ASX on 17 April 2019. In FY19, the company witnessed a growth of 13.5% in pro-forma revenue on FY18, which was ahead of the prospectus forecast. EBITDA and NPATA for the year outperformed the prospectus forecasts during the year. The period was also characterised by a number of client wins on the back of improved product quality, tailored to client requirements. During the year, the company continued to invest in research & development to drive further innovation. The period saw an increase in the average revenue per client and higher client revenue retention rates that speak volumes about the value being offered to customers.

Going forward, the company will continue to explore opportunities in the form of acquisitions, development or partnership that will help contribute to growth in core markets. The company expects both pro-forma revenue and EBITDA for the calendar year 2019 to report a double-digit growth as compared to prior corresponding period. As per the management, strong prospects for growth across both segments promise a brighter future for ReadyTech Holdings Limited.

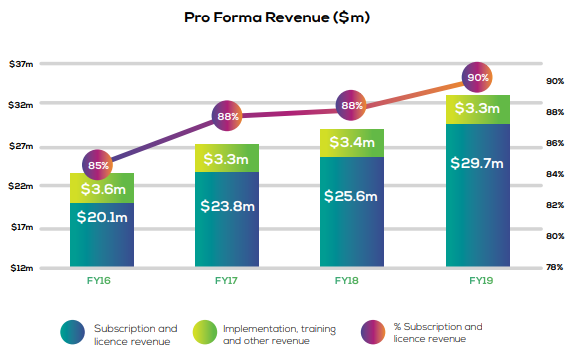

Since FY16, the company has seen a continuous upward movement in pro-forma revenue, with the majority of the revenue derived from subscription and license fees in the last four years. In FY16, the company reported total pro-forma revenue amounting to $23.7 million, out of which subscription and license revenue amounted to $20.1 million, representing 85% of the total revenue. The share went up by 3% in FY17 and FY18 to 88%. In FY19, pro-forma revenue amounted to $33 million, out of which 90% comprised of subscription and license revenue. Over the period covering FY16 to FY19, the company’s pro-forma revenue has reported a CAGR of 11.7%, with the highest y-o-y growth reported in FY17 at 14.3%.

Pro-Forma Revenue (Source: Company Reports)

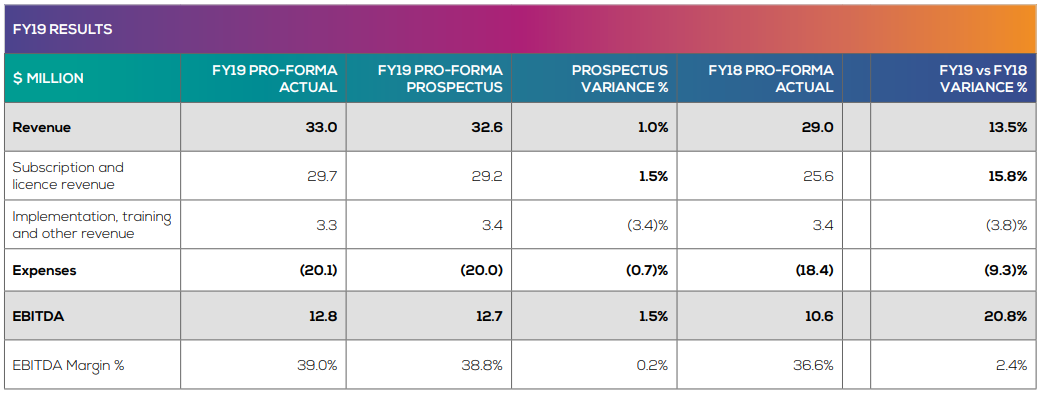

Financial Highlights for the Year Ended 30 June 2019: During the year, the company generated pro-forma revenue amounting to $33.0 million, up 13.5% on the previous year and exceeding the prospectus forecast by 1%. Revenue growth during the year was driven by a combination of new client wins and increased sales to existing customers. Pro-forma EBITDA for the year was reported at $12.8 million, representing a rise of 20.8% on prior corresponding period. Pro-forma EBITDA also exceeded the prospectus guidance by 1.5%. Average revenue per client stood at $8.9k, representing an increase of 12% on FY18. During the year, the company reported a statutory loss after tax amounting to $1.5 million, mainly attributable to costs related to initial public offering. Cash flow from operations for the year increased by 40.4% to $12.5 million. Client revenue retention rate for the year stood at 96%, and operating cashflow conversion ratio stood at 98%.

FY19 Results (Source: Company Reports)

Education Segment Results: Revenue for the segment was in-line with the prospectus at $20.0 million, up 12.0% on the previous year. Growth was driven by greater per client spend and strong client wins across the company’s platform. EBITDA for the segment stood at $8.1 million as compared to prior corresponding period EBITDA of $7.1 million. EBITDA margin for FY18 and FY19 stood at 40% and 41%, respectively, reflecting an improved financial position.

Employment Segment Results: Revenue for the employment segment was reported at $13.0 million, up 15% on prior corresponding year. Growth in the segment was aided by a strong new client growth and increased spending from existing clients. EBITDA was reported at $6.2 million as compared to $5.1 million in the previous year. EBITDA margin for the segment went up from 45% in FY18 to 48% in FY19.

Going forward, the company expects revenue to grow with a solid new business pipeline in place for both the Employment and Education segments. The business has performed in-line with expectations for the first 8 weeks in FY20 and enjoys strong growth prospects for growth. Under the Education segment, it is eyeing the largest providers of tertiary education with its advanced, enterprise SaaS product and has a strong pipeline of interest, following recent wins like the University of Queensland. Things have also been unfolding in favour of the Employment segment, with increased interest from larger employers that seek a trusted managed service or software payroll and HR administration solutions.

Recent Updates:

(a) Notice of AGM: The company recently updated that the 2019 Annual General Meeting will be held on 20 November 2019.

(b) Change in Director’s Interest: As per another recent announcement, Tom Matthews, director of the company, acquired 26,315 ordinary shares for a total consideration of $49,242.51 on account of on-market trade.

(c) Acquisition: The company recently completed the acquisition of two leading payroll and workforce management software and services businesses, Zambion and WageLink. The acquisition involved a combined payment of $12 million for both the businesses and strengthened the company’s presence in the employment segment. Zambion was acquired for an initial upfront payment of $4.2 million and a deferred payment of $6.3 million, subject to recurring revenue targets being met. Out of the deferred consideration, $4.5 million is expected to be paid in H2FY20. WageLink was acquired for a consideration of $1.6 million. Both the transactions were completed on 09 October 2019 and are expected to deliver revenue and EBITDA of approximately $700,000 and $200,000, respectively, in addition to prospectus targets for CY19.

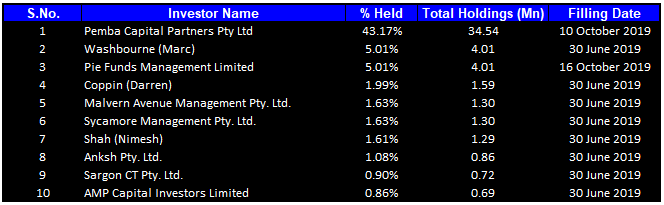

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 62.88% of the total shareholding. Pemba Capital Partners Pty Ltd is the entity, holding maximum shares in the company at 43.17%. Washbourne (Marc) and Pie Funds Management Limited are the second largest shareholders, with a percentage holding of 5.01% each.

Top Ten Shareholders (Source: Thomson Reuters)

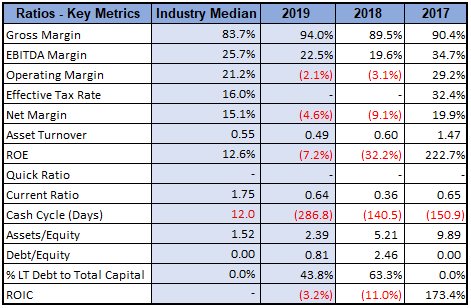

Key Metrics: During the year ended 30 June 2019, the company had a gross margin of 94.0%, which is higher than the industry median of 83.7%. The margin also increased in comparison to FY18 gross margin of 89.5%. EBITDA margin for FY19 was reported at 22.5%, higher than prior corresponding year margin of 19.6%. In FY19, the company had a current ratio of 0.64x as compared to the current ratio of 0.36x in FY18, representing an improved position to meet short-term obligations of the business. The company’s debt to equity ratio went down signifcantly in comparison to prior corresponding year. Debt/Equity ratio for FY19 and FY18 stood at 0.81x and 2.46x, respectively.

Key Metrics (Source: Thomson Reuters)

What to Expect: As per the guidance provided, pro-forma revenue for CY19 is estimated at $35.1 million, representing a yoy growth of 14% in comparison to prior corresponding year. Pro-forma EBITDA for the year is expected to be $14.6 million, representing a yoy growth of 28% on CY18. Going forward, the company will continue to assess complementary technologies and customer bases to spread its wings further. Its new business pipeline across both the education and employment segments is expected to drive revenue growth in the coming years.

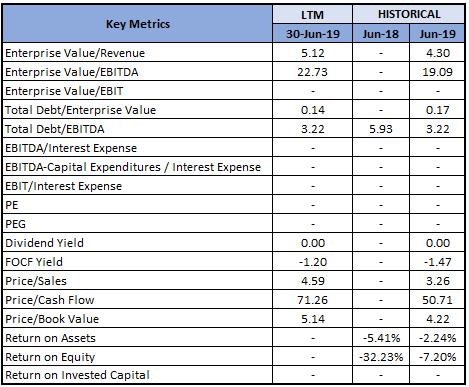

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

Method 1: Enterprise Value to Sales Multiple Approach:

(17).png)

EV/Sales Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

Method 2: Enterprise Value to EBITDA Multiple Approach:

(8).png)

EV/EBITDA Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

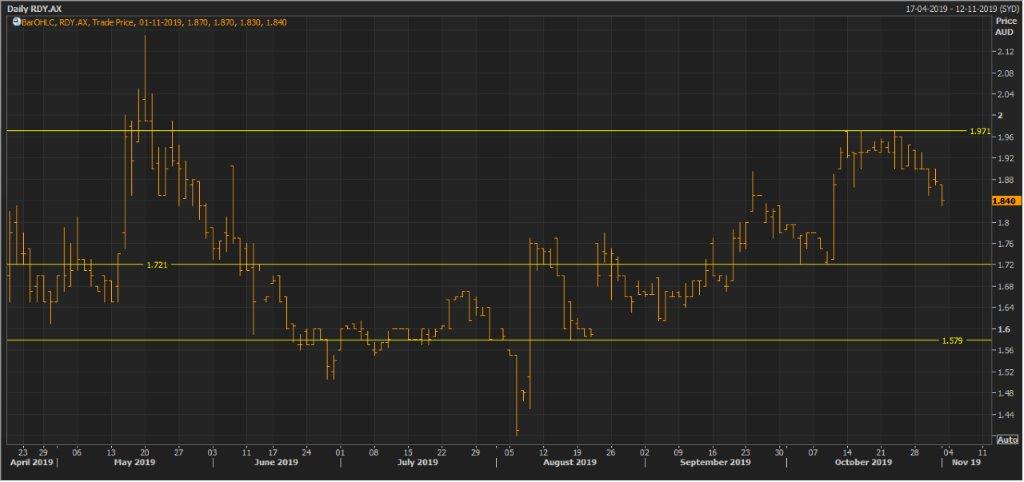

Stock Recommendation: The stock of the company generated returns of 4.46% and 18.67% over a period of 1 month and 3 months, respectively. In FY19, the company reported a decent financial position, with revenue and profits exceeding the prospectus forecasts. On the back of the growing popularity of its product, the company saw substantial client addition during the year. The success of new client wins was evident in the performance of both the Education and Employment segments, depicting an improvement across key financial metrics. The recent acquisitions of Zambion and Wagelink strengthened the company’s position in the employment segments and are well in-line with its strategy to acquire complementary technologies, capabilities and new customer bases, targeting higher value customers. As per the company’s reports, the business has performed to forecast in the first 8 weeks of FY20 and is expected to flourish from a strong pipeline of opportunities in the future. Considering the performance in FY19, outlook for CY19, and future growth prospects across both the business segments, we have valued the stock, using two relative valuation methods, i.e., Enterprise Value to Sales multiple, and Enterprise Value to EBITDA multiple, and arrived at a target price of higher single digit to lower double-digit growth (in % term). Hence, we recommend a “Buy” rating on the stock at the current market price of $1.840, down 1.867% on 01 November 2019.

RDY Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...