Kalkine has a fully transformed New Avatar.

Company Overview: Ramsay Health Care Limited is an operator of hospitals. The Company operates approximately 235 hospitals and day surgery facilities across Australia, the United Kingdom, France, Indonesia, Malaysia and Italy. The Company's segments are Asia Pacific, UK and France. The Company's facilities cater for a range of healthcare needs from day surgery procedures to complex surgery, as well as psychiatric care and rehabilitation. In Australia, the Company operates approximately 73 hospitals and day surgery units. In the United Kingdom, the Company provides independent hospital services in England, with a network of over 35 acute hospitals and day procedure centers providing a range of clinical specialties to private and self-insured patients, as well as to patients referred by the National Health Service (NHS). In the United Kingdom, it also operates a diagnostic imaging service and provides neurological services through its over three neuro-rehabilitation facilities.

.png)

RHC Details

RHC Delivered Overall Robust 1H FY 2019 Performance: Ramsay Health Care Limited (ASX: RHC) happens to be a global health care company which is having the reputation for operating high-quality services and delivering excellent patient care. On March 4, 2019, the company had a market capitalization of ~$12.91 billion. Recently, the company had delivered strong results for 1H FY 2019 (six months ended December 2018), and it posted core NPAT of $290.8 million reflecting 1% rise YoY. Excluding Capio, its core NPAT came in at $293.2 million reflecting YoY rise of 1.8%. The company’s core EPS stood at 140.6 cents implying YoY rise of 1.2%, however, excluding Capio, the core EPS was 141.7 cents reflecting a 1.9% rise. Ramsay Health Care has been maintaining its focus towards growth as it added 169 beds through Australian brownfield programme for H1 and it is also expanding and improving the service offering both in and out of the hospital. Additionally, the company has maintained its focus on cost efficiency. Ramsay Health Care also possesses decent position with respect to its key margins as, at the end of December 2018, the net margins stood at 5.3% reflecting a rise of 170 basis points from 2H FY 2018 demonstrating its capability to convert its top line into the bottom line. The company’s EBITDA margin stood at 13.5% in 1H FY 2019 while, in 2H FY 2018, it was 12.4%.

.png)

RHC’s Strategic Position (Source: Company Reports)

In 2018, Ramsay Générale de Santé (or RGdS) had acquired a total of 98.5% of share capital of Capio AB. As a result of Capio acquisition, the company was able to deliver on the strategy of becoming the global health care operator and “provider system of choice” in markets in which it operates. The company now enjoys leading positions in Australia, France and Scandinavia thus enabling it to achieve the improved economies of scale, best practice, cost leadership, speed to market and innovation. The company’s growth, over the long-term, would be supported by its focus towards operational efficiencies, Capio acquisition, robust balance sheet and decent momentum in the dividends from the past few years. Ramsay Australia is in a healthy position to meet the growth in demand and to respond to the market challenges. The focus over operational efficiencies is expected to result in lower costs which would, in turn, support the company’s bottom line moving forward.

Admissions and Focus on Operational Efficiencies Aided RHC’s Australia Division: Ramsay Health Care’s Australian operations posted revenues of $2,603 million in 1H FY 2019 reflecting the YoY rise of 4.8% while these operations posted EBITDA of $484.6 million implying YoY rise of 5.7%. The results for Australian operations got helped by growth in admissions and focus towards the operational efficiencies. The company has been making deployments towards the new and innovative services and we expect that these deployments would continue to support Australian operations and might also bode well for the long-term growth. With regards to Australian operations, the company continues to strengthen its operations and management team in Pharmacy so that the business can accomplish the next phase of growth. Since Ramsay Australia would continue to focus on innovation and cost optimization strategies, we believe that it would continue to support its top line and bottom-line growth in years to come.

.png)

Ramsay Australia Business Division Performance (Source: Company Reports)

Understanding Continental Europe’s Performance in 1H FY 2019: With respect to continental Europe, RGdS had delivered robust operating result in 1H FY19 which is above the expectations. As per the release, the revenues and EBITDAR amounted to €1,340.1 million and €231.3 million in 1H FY 2019 implying the rise of 25.7% and 19.1%, respectively. Further, the large-scale restructuring programme to centralize the non-core hospital functions in France happens to be on track. After the acquisition, Capio had contributed a positive operating result, however, it negatively impacted the net profit, after factoring in the financing costs. Stockholm County Council (or SCC) had extended Capio’s contract to run S:t Görans hospital to 2026 and two acute geriatric services at the hospitals in Stockholm. There has been an announcement for tariff increase for France which happens to be the first positive tariff increase in almost a decade which indicates improvement in sentiments for the sector. With regards to continental Europe, the company has been focusing on achieving the synergies and integrating the Capio business and the divestment of non-strategic assets.

.png)

Continental Europe Business Performance (Source: Company Reports)

Recovery to NHS Volume Aided UK’s Operations: The company’s United Kingdom operations encountered a challenging Q1, and it weighed over the overall earnings for 1H FY 2019. The UK operations garnered revenues of £209.6 million reflecting a 1.6% YoY rise and EBITDAR of £44.8 million implying 9.2% fall YoY. However, the company’s UK operations witnessed a good recovery in NHS volume growth in Q2. There have been positive signs in the UK which are emerging in terms of both price and volume growth, and the UK government has renewed the commitment to patient choice and the use of independent providers to cut waiting times. However, this business unit might face short-term challenges due to Brexit.

.png)

United Kingdom Business Performance (Source: Company Reports)

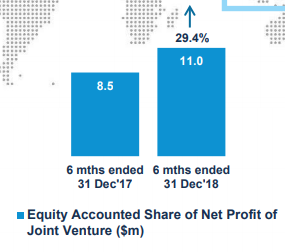

Analysing Performance of Asian Operations: With respect to Asia, the company stated that there has been a robust operating performance in Malaysia and its key focus area is the cost controls. These operations posted equity accounted share of net profit of the joint venture of $11 million in 1H FY 2019. The new developments which target the universal healthcare patients have been opened throughout the Indonesian facilities. The company would continue to analyse the growth opportunities in the market.

Asia Business Performance (Source: Company Reports)

How Capio Acquisition Could be A Long-Term Growth Driver: It can be said that Capio acquisition would drive the growth over the long term. The company’s management is also very optimistic about the acquisition, and they reiterated its strategic fit with RGdS and its underlying growth fundamentals. The company had spent required time to gain a better understanding of the business and the company views that there are numerous synergies and opportunities.

Within two to three years, the management expects that Capio would be core EPS accretive. However, considering the timing of acquisition and delays to processes with regards to completion, there are expectations that it would be slightly EPS dilutive to Ramsay Group in FY 2019. The company stated that the integration plan is underway as they are setting up a new executive governance structure, harmonizing the operations in France and enhancing clusters and divesting the non-strategic assets. Also, they are securing the synergies, and they conducted the debt refinancing.

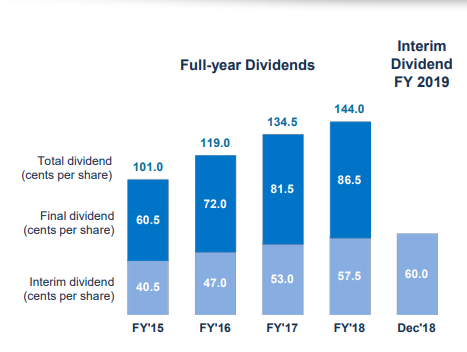

Decent Growth in Interim Dividend: Ramsay Health Care has delivered a decent growth in declaring the interim dividend as, in 1H FY 2019, they declared 60.0 cents per share. The record date happens to be March 7, 2019 and the payment date is March 29, 2019. The company’s dividend has been witnessing an uptrend over the past few years which is reflective of its robust business fundamentals and, we expect, that it might attract market players’ attention. The interim dividend of 1H FY 2019 is fully franked and is up 4.3% on the previous corresponding period’s interim dividend.

Dividend Growth (Source: Company Reports)

Drivers for Future: Over the long-term, there are expectations that demand of the hospital market would be driving growth in the sector globally. With respect to Australia, the company has been maintaining a market leadership position with regards to the strength and diversity of the portfolio and delivering high-quality services. Even though the private healthcare sector is exposed to short term challenges, the outlook for long-term for the sector is positive. The company has maintained its focused towards achieving the synergies which are related to Capio transaction, divestment of non-strategic assets and integrating the business with RGdS. Barring the unforeseen circumstances, the company has reaffirmed its core EPS growth of up to 2% for FY 2019 (including Capio).

With regards to Australia, for FY 2019, brownfield programme is on track to deliver $242 million in the completed projects.

Stock Recommendation: In the last three months, the stock has risen 16.64% and is trading at PE multiple of 32.16x. From the technical perspective, Moving Average Convergence Divergence or MACD has been applied on the daily chart of RHC, and default values were used for the purposes. After careful observation, it was noted that MACD line has crossed the signal line and had trended in the upward direction after crossover which reflects that the company’s stock price might witness a rise moving forward.

Fundamentally, we are optimistic on the company at the back of healthy balance sheet, securing a strategic partnership with Capio, strong pipeline of brownfield opportunities, and the ability to assess growth opportunity in the Asia Pacific market. The company’s ROE stands at 11.2% in 1HFY19 which is decent enough considering the concerned industry median of 8.5%. Given the backdrop of aforesaid facts and decent outlook in the long run, we give a “Buy” recommendation on the stock at the current market price of A$63.030 per share (down 1.315% on 4 March 2019).

.png)

RHC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...