Company Overview - Ramsay Health Care Limited is an Australia-based provider of healthcare services. The Company operates approximately 220 hospitals and day surgery facilities across Australia, the United Kingdom, France, Indonesia and Malaysia. The Company's segments include Asia Pacific, the United Kingdom and France. The Company provides a range of healthcare services, such as surgery procedures, psychiatric care and rehabilitation. It has approximately 25,000 beds and more than 50,000 staff across five countries. It has interest in Ramsay Sime Darby Health Care Sdn Bhd (RSDH), a joint venture involved in operating hospitals and day surgery facilities across Malaysia and Indonesia. In the United Kingdom, Ramsay Health Care Health UK also operates a diagnostic imaging service and provides neurological services through its three neuro-rehabilitation facilities. The Company, through Ramsay Generale de Sante, operates a private hospital group in France with around 110 facilities (100 hospitals).

.png)

RHC Dividend Details

Outstanding France business performance: Ramsay Health Care Limited (ASX: RHC) continued to deliver strong financial performance even for the first half of 2016, while its international regions generated even better returns. The group’s French business, Ramsay Générale de Santé, reported an outstanding revenue increase of 57.2% while the EBITDAR rose by 49.6%. The Générale de Santé acquisitions contributed for additional three months earnings. Meanwhile, the group’s UK revenues surged by 2.7% to £203.4 million driven by the NHS admissions growth of 8%. EBIT enhanced by 9.3% to £17.0 million as compared to the prior corresponding period (pcp) as the group’s efforts of improving efficiency paid off in the region. Moreover, the recent tariffs indicate an increase on average of around 1% from April this year after earlier witnessing a negative tariff change in the UK.

As per the core Australian business performance, the region delivered a decent top line increase of 7.4% during the first half while the EBIT improved by 9.4% as compared to the first half of 2015 on the back of strong admissions growth. Management reported that its Australian business performed as per its expectations.

.png)

Strong France business performance (Source: Company Reports)

Solid bottom line growth: Ramsay Health Care was able to achieve a strong bottom line growth with a Core Net Profit after Tax rise of 16.2% to $237.4 million for the first half of 2016, as compared to the same period of last year. Accordingly, the group’s core earnings per share rose by 16.9% to 114.1 cents during the period as compared to 97.6 cents in the same period of last year.

RHC’s net profit after tax post adjusting for non-core items rose by 17.5% to $224.9 million as compared to the pcp. The group declared a fully-franked interim dividend of 47.0 cents, which rose by 16% as compared to the first half of 2015.

.png)

Core NPAT and Core EPS performance (Source: Company Reports)

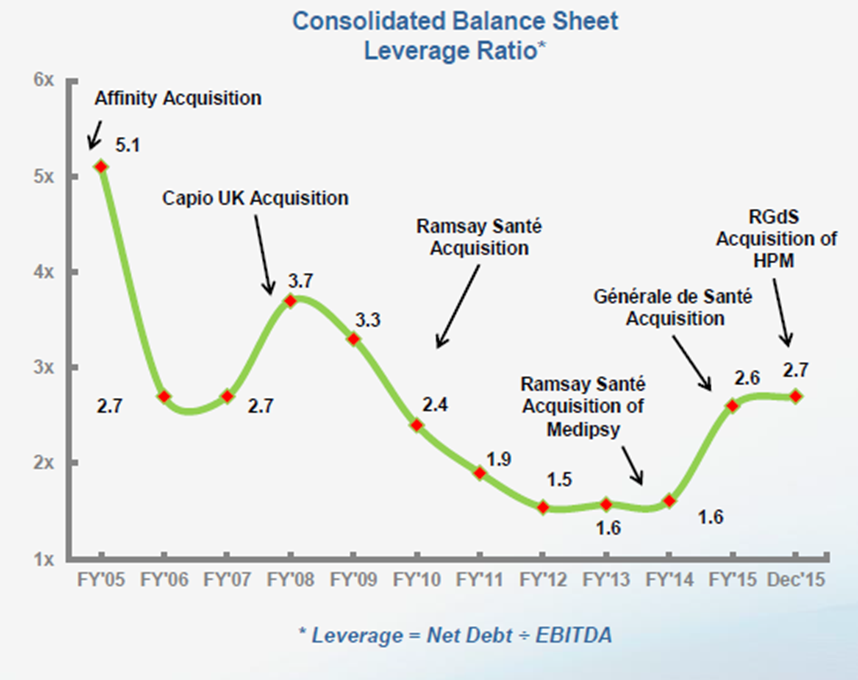

Cautious partnerships or acquisitions: Recently, Ramsay Sime Darby Health Care, which is a partnership between the group and Sime Darby Berhad, reported that they are not advancing the anticipated joint venture at Chengdu in China, as several conditions were not on track as estimated by the firm. This indicates the cautious approach of the group while pursuing partnerships or acquisitions and given the slowdown in China, the group’s joint venture in China might not be able to generate the estimated returns.

On the other side, Ramsay Health Care has been pursuing strategic acquisitions to expand its business base across the globe and by December 2015, Ramsay Générale de Santé finished the acquisition of the HPM Group, which had nine hospitals in Lille, France. As a result, Ramsay Générale de Santé enhanced its greater Lille area penetration at 11 facilities having 2,180 employees, 700 doctors and projects to give their treatment to over 160,000 patients per annum. The group made a strategic alliance with ICHOM (International Consortium for Health Outcomes Measurement) during August 2015 which would position the group on a global level while measuring, reporting and benchmarking patient outcomes.

Consolidated Balance Sheet Leverage Ratio with acquisitions timeline (Source: Company Reports)

Favorable target industry drivers: Ramsay is positioning itself to leverage the favorable industry drivers which includes the rising demand for healthcare on the back of improving ageing population, longer life expectancy, growing chronic disease burden coupled with population increase. Moreover, growing preference for consumers for better treatments and diagnostic methods would also generate demand. In Australia alone the industry fundamentals are very strong wherein the Private health insurance membership represents over 47.2% of the population having hospital treatment insurance (as of Dec 2015 quarter). With the growing demand for healthcare due to rising ageing population, the admissions in the region has been increasing. In fact, the region is expecting to witness further rise in the coming two decades on the back of increase in baby boomers who are shifting to the 70+ age group. Accordingly, the group is involving itself in required government reviews in order to address this booming opportunity as well as attain realistic outcomes to enhance the present health care system. Some of these reviews include Private Health Insurance, Primary Health Care Review, Prostheses Review and Medicare Benefits Schedule (MBS) Review. Even on the global level, greater than 10% of the population is currently above 65 years which is roughly around 580 million.

Moreover, the global population with age above 60 is estimated to increase more than three times by 2050. Then the major cause of mortality in the world is chronic diseases which accounts for 63% of all deaths. Therapeutic innovations would continue to contribute to the healthcare demand while non-demographic factors like new technology and more doctors are also placed among the major drivers of healthcare demand. Given such a tremendous opportunity Ramsay is positioning itself on a global level with presence in UK, Asia and France.

Bed growth estimations in Australia (Source: Company Reports)

Positioning itself to leverage the booming opportunity: The group finished 186 beds and 8 operating theatres with total worth of $126 million, under its brownfield capacity expansion program for the first half of 2016 period. These program initiatives included starting 60 new beds as well as 6 theatres at Hollywood Private Hospital and a 56-bed new accommodation wing at Cairns Private Hospital, during October 2015.

Moreover, the group also started the new Wollongong Private Hospital during January 2016. Ramsay Health Care also enhanced its Figtree Private Hospitals with 151-bed hospital and 10 theatres as compared to the present 101 beds, and intends to convert this into a rehabilitation facility to capture the growing demand for these services at the Illawarra region. The group is planning to open more 400 (310 net) beds as well as 12 theatres in the coming twelve months (as of first half of 2016 reports) which includes major developments at St George Private, Peninsula Private in Melbourne, North Shore Private in Sydney as well as New Farm Clinic in Brisbane.

Stock Performance: The shares of Ramsay have been volatile over the last one year and fell over 8.20% during the period (as of April 01, 2016) given the volatile conditions across the globe. The stock continued its weakness even during this year and declined over 10.6% during this year to date (as of April 01, 2016) as the group was not able to deliver results as per market estimations. RHC’s withdrawal of joint venture in China also hurt its stock price leading to a decline of over 7.8% in the last one month alone (as of April 01, 2016). On the other hand, the long term industry dynamics are very favorable to the group given the growing demand for healthcare on the back of increasing ageing, population, technology changes and the high chronic disease rates. Consequently, the hospital utilization rates would increase as consumers are preferring best treatments on the back of improving penetration of private insurance. Ramsay is targeting this opportunity and accordingly placing itself with its brownfield capacity expansion program. Despite withdrawing the JV opportunity in China, the group is constantly pursuing strategic opportunities in existing as well as new markets.

Accordingly, management improved its fiscal year of 2016 guidance of core NPAT and core EPS increase to 15% to 17% as compared to its earlier estimate of 12% to 14%. We believe that long term investors need to leverage the recent correction and enter the stock. Based on the foregoing, we give a “BUY” on this stock at the current price of $61.16

.PNG)

RHC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...