Company Overview: QBE Insurance Group Limited is engaged in underwriting general insurance and reinsurance risks, management of Lloyd's syndicates and investment management. The Company's segments include North American Operations, which writes general insurance and reinsurance business in the United States of America; European Operations, which writes general insurance business, both general insurance and reinsurance business through Lloyd's of London; Australian & New Zealand Operations, which primarily underwrites general insurance risks throughout Australia and New Zealand, providing all lines of insurance for personal and commercial risks; Emerging Markets, which writes general insurance business in North, Central and South America, and provides personal, commercial and specialist general insurance covers throughout the Asia Pacific region; Equator Re, which provides reinsurance protection to related entities, and Corporate & Other.

.png)

QBE Details

Turnaround Performance in 2018: QBE Insurance Group Limited (ASX: QBE) is a large-cap insurance company with the market capitalisation of ~$15.51 billion as of July 22, 2019. The company earlier released its results for FY18 in which it posted cash profit after tax amounting to $715 million, which reflects a significant improvement on cash loss amounting to $262 million witnessed in 2017. The company’s net profit after tax stood at $390 million (which includes a $567 million profit from the continuing operations) as compared to the loss of $1,249 million in the prior year. It stated that the company’s improved financial performance for 2018 reflected significantly improved attritional claims experience throughout all the divisions along with a reduced level of the catastrophe claims. However, this got partly offset by the lower net investment yield, which was adversely impacted by the market volatility in the final quarter. Additionally, the company posted FY18 combined operating ratio of 95.7%, which was in line with the target range of 95.0%-97.0% and a meaningful improvement from 103.9% in 2017. The uplift in the underwriting profitability was supported by improvement in the attritional claims ratio to 50.2% from 53.1% in the prior year, along with the significant reduction in the cost of catastrophe claims after an extreme 2017.

The company’s annual dividend yield of 4.24% is higher than the broader industry average of 3.8%, which might attract the attention of market players moving forward. Moreover, the company has recorded a positive cash RoE of 8.0% in FY18 as compared to negative cash RoE of 1.4% in FY17. Additionally, the company focuses on enhancing data and analytics capabilities and reducing the complexity, which might act as tailwinds for the growth in the long run.

.png)

Results Snapshot (Source: Company Reports)

Top 10 Shareholders: The following table gives a broad overview of the top 10 shareholders of QBE Insurance Group Limited:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Respectable Position In Key Leverage Ratios: QBE is possessing respectable position when it comes to its leverage ratios as is evident from its Debt/Equity ratio of 0.38x in FY 2018, which reflects a fall from the FY17 ratio of 0.41x and, thus, it looks like that the company has been deleveraging its balance sheet. Also, in FY18, the long-term debt as a percentage to total capital stood at 27.5%, which implies a fall of 1.4% on a YoY basis. The reduced exposure to the debt component might help the company in stabilizing its balance sheet moving forward, which could further improve its position to achieve long-term growth prospects.

.png)

Key Metrics (Source: Thomson Reuters)

Recovery of Balance Sheet and Declaration of Dividends: In the market release for FY18 results, QBE stated that the recovery of the balance sheet has been witnessed post the extreme catastrophe experience which was witnessed in 2017. The company stated that its indicative APRA PCA multiple stood at 1.78x at the end of December 31, 2018, which reflects a rise from 1.64x as at December 31, 2017 and it is also towards the upper end of QBE’s 1.6x – 1.8x target PCA range. Additionally, the company’s final dividend for 2018 has been increased to AUD 28¢ps, while in 2017 it was AUD 4¢ps, which reflects confidence in QBE’s balance sheet as well as improved earnings resilience.

As a result of the final dividend, the company’s full year dividend for 2018 stood at AUD 50¢ps in comparison to FY 2017 figure of AUD 26¢ps and, when it gets combined with A$333 million of the shares repurchased via buyback, it brings the total shareholder returns in 2018 to more than A$1 billion.

.png)

Shareholder Returns (Source: Company Reports)

Completion Of Purchase Of QBE’s Travel Insurance Business: nib holdings limited (ASX: NHF) recently made an announcement about the completion of the purchase of QBE’s travel insurance business. It was stated that acquisition includes distribution and claims capability of QBE Travel and the business would be re-branded to nib Travel. The final purchase price happens to be $24.2 million. The top management of nib reflected positive views and stated that the acquisition is consistent with nib’s strategy to grow the travel insurance operations domestically as well as globally. There are expectations that nib Travel’s annual domestic gross written premium would be increased by over 50%. It was also added that the acquisition adds considerable scale to the nib’s existing platform in order to deliver further revenue as well as cost synergies.

Senior Management Changes: There was a recent announcement with respect to the changes to the Group Executive Committee. As per the release, Group Chief Operations Officer named David McMillan decided to take up the new opportunity as CEO of UK-based insurer. It was also stated that Group Chief Information Officer named Matt Mansour, who joined QBE in 2018 after working with Barclays, would join the Group Executive Committee.

Margaret Murphy, who happens to be the group Chief Human Resources Officer, would take on the broadened role as Group Executive, People & Change, with the responsibility for People, Culture and Transformation.

Simplification of Segment Reporting: As mentioned in the release, QBE Insurance Group Limited would be simplifying its reporting and it would be disclosing 3 divisional segments rather than 5. The simplification would be resulting in reporting segments like:

(A)Asia and European Operations together would comprise “International”,

(B)Pacific and Australian & New Zealand Operations together would form “Australia Pacific”, and

(C)North America would be continuing as is.

The company would no longer be separately identifying Equator Re as standalone segment.

Announcement Of Ogden Discount Rate Decision: The UK Ministry of Justice made an announcement about the change in the statutory discount rate for use in the determination of lump-sum payments in relation to the UK personal injury claims. QBE has been utilising the discount rate of 0.25% for the purpose of determination of Ogden related lump sum payments. The company has been assessing the impact of the change and stated that the adoption of the revised statutory rate of -0.25% is expected to result in the one-off increase in QBE’s net central estimate of the outstanding claims liabilities of around $60 million. It was also added that the impact would be reported as an adjustment to the company’s 1H FY19 and FY19 statutory results.

What To Expect From QBE Moving Forward: QBE Insurance Group Limited is well-positioned because of improved performance in 2018 along with more simplified structure as well as focus towards achieving the cost reductions throughout the group. There are expectations that in 2019 the company would be continuing to drive further performance improvement, increase usage of the data analytics as well as digital tools when it comes to underwriting, strengthen the earnings quality, target further improvements in the company’s RoE and, would continue to deliver the value for the shareholders.

Priorities for 2019 (Source: Company Reports)

Additionally, the company’s priorities for 2019 revolve around managing the risk, operating sustainably as well as be focused towards the customer. The company is focused towards being more digitally enabled, reduce the complexity and enhance the data and analytics capabilities. However, it is also expected to focus on risk governance.

.png)

Key Valuation Metrics (Source: Company Reports)

Valuation Methodologies:

Method 1: Price to Book Value based Valuation

.png)

Price to Book Value based Valuation (Source: Thomson Reuters), *NTM: Next Twelve Months

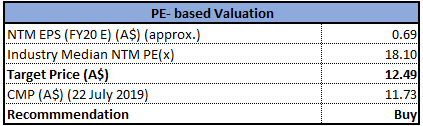

Method 2: PE- Based Valuation

PE- Based Valuation (Source: Thomson Reuters), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock of QBE Insurance Group Limited delivered the return of 6.88% in the span of previous six months, while on the YTD basis, the stock’s return stood at 19.80% which can be considered at respectable levels and might attract the attention of market players. As per ASX, the annual dividend yield of QBE stood at 4.24%, which is higher than the industry median of 3.8%, thus, it can be said that the company has been delivering respectable returns to its shareholders and the dividend-seeking investors might show some interest in the stock moving forward.

The company stated that, throughout 2018, the company witnessed excellent progress in re-underwriting the Asian business, and the company’s Asia Pacific operations returned to an underwriting profit in 2H of the year with the combined operating ratio of 99.5%. As stated in the company’s 2018 annual report, there are expectations that the company would be reducing its cost base by $130 million (net) over the time span of 3 years, reducing the complexity, optimising the end-to-end processes as well as increasing the automation. Also, the company stated that it would remain focused towards attracting and developing high-quality talent as well as building the company for future by investing in, and leveraging, data, analytics, and technology. On the backdrop of above factors, we have valued the stock using Relative valuation method, P/BV and P/E multiple and have arrived at the target price of the stock in the range of $12.49 to $13.32 (high single-digit to low double-digit upside (%)). Hence, in the view of aforesaid facts, we give a “Buy” rating on the stock at the current market price of A$11.730 per share (down 0.593% on 22 July 2019), ahead of its interim result due in August 2019.

.png)

QBE Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...