Company Overview: QBE Insurance Group Limited is engaged in underwriting general insurance and reinsurance risks, management of Lloyd's syndicates and investment management. The Company's segments include North American Operations, which writes general insurance and reinsurance business in the United States of America; European Operations, which writes general insurance business, both general insurance and reinsurance business through Lloyd's of London; Australian & New Zealand Operations, which primarily underwrites general insurance risks throughout Australia and New Zealand, providing all lines of insurance for personal and commercial risks; Emerging Markets, which writes general insurance business in North, Central and South America, and provides personal, commercial and specialist general insurance covers throughout the Asia Pacific region; Equator Re, which provides reinsurance protection to related entities, and Corporate & Other.

.png)

QBE Details

Improved Attritional Claims Aided FY 2018 Results: QBE Insurance Limited (ASX: QBE) had posted strong improvement in its FY 2018 results on YoY basis which is evident as its cash profit after tax amounted to $715 million, and this implies strong improvement as compared to the previous year in which it posted cash loss amounting to $262 million. The company’s net profit after tax stood at $390M (which includes $567 million profit from continuing operations) while there was a loss amounting to $1,249 million in the prior year. The improvement in the attritional claims experience throughout the divisions along with lower level of catastrophe claims have aided QBE’s FY 2018 performance. This improvement got offset by lower net investment yield which got severely impacted because of the market volatility in the final quarter. Also, the company’s balance sheet witnessed a significant improvement after extreme catastrophe experience of 2017. The company’s indicative APRA PCA multiple stood at 1.78x at 31 December 2018 reflecting a rise from 1.64x from the previous year and towards the upper end of the company’s 1.6x – 1.8x target PCA range. The company declared a final dividend of 28 cents per share while in the previous year it declared 4 cps which demonstrates confidence in QBE’s balance sheet and improved earnings resilience.

Moving forward, the company plans to reduce the cost base in the coming years which might attract the market players’ attention. For FY19, QBE’s priorities include the increased focus towards customer outcomes and delivering against the customer commitment program (EQUITY).

.png)

FY 2018 Results Snapshot (Source: Company Reports)

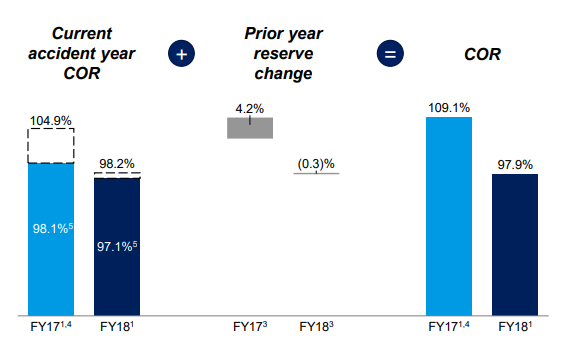

North American Operations’ GWP Rose 3%: QBE’s North American operations posted gross written premium of $4,711 million reflecting a rise of 3% on the back of an average premium rate increase across the portfolio of 4.1% as compared to 0.7% in the prior year. The crop business gross written premium stood at $1,474 million demonstrating a rise of 5% on the back of increased coverage and a modest increase in policy count. However, its net earned premium witnessed a decline of 2% and stood at $828 million highlighting increased cessions with regards to the MPCI scheme. The company’s North American operations’ combined operating ratio (or COR) stood at 97.9% which implies a fall from 109.1% in the prior year. We expect that the company’s North American operations would primarily be helped by the exit which was done from underperforming retail personal lines business (the independent agent and Farmers Union Insurance businesses), by the strengthening of crop business via improved analytics helping better risk selection and management with respect to commodity price volatility and by the strengthening of program partnerships with the deployments which support more data driven approach to pricing.

North America Operations (Source: Company Reports)

Deployments towards pricing, risk selection tools Might Aid European Operations: QBE’s European operations’ posted headline gross written premium of $4,355 million in FY 2018 demonstrating 8% increase as, in 2017, it was $4,049 million. The business’ gross written premium rose 6% on a constant currency basis demonstrating stronger sterling and euro against the US dollar. The business’ net earned premium rose 9% and stood at $3,505 million while in the prior year it was $3,212 million. To tackle the Brexit challenge, the business has fully operational and well-capitalized insurance and reinsurance company which is situated in Belgium. Therefore, the business has been enhanced across Europe, and it has successfully renewed its existing business in continental Europe at 1 January 2019 renewals. We expect that increased footprints might act as a tailwind for European operations. Moreover, the company is optimistic about the deployments towards pricing and risk selection tools.

European Operations (Source: Company Reports)

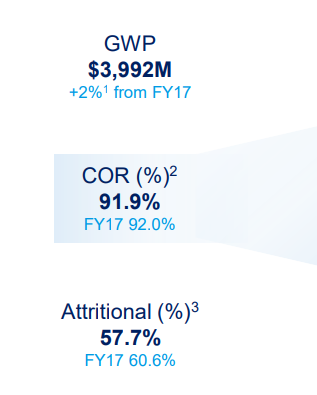

Analysing QBE’s Australian & New Zealand Operations: QBE’s Australian and New Zealand operations have adopted more granular and disciplined approach towards pricing which contributed to the above market rate increases as there was an average premium rate increase of 7.3% in 2018 which implies a rise from 6.1% in the last year and 6.6% in the first half. The company’s Australian & New Zealand Operations posted a combined operating ratio of 91.9% while in the previous year it was 92.0%. The company added that the Australian financial services sector was under significant scrutiny. The company plans to work with industry so that the focus on customer outcomes can be increased. The new strategy of the business would be helping it in becoming simpler, stronger and more customer centred organization which has the ambition to be the number one choice when it comes to commercial lines. This might also help in building strength in personal lines and the business might also be innovative in the small and medium-sized enterprise (SME) space.

Australia and New Zealand Operations (Source: Company Reports)

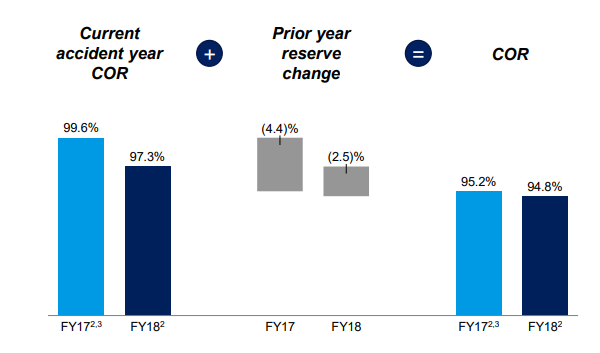

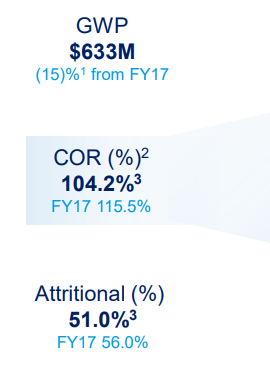

Remediation of Poor Performing Portfolios Might Support Asia Pacific Operations: QBE’s Asia Pacific operations ended FY 2018 on the strong note as the combined operating ratio stood at 104.2% as compared to 115.5% in the previous year and 108.5% in 1H FY 2018. In FY 2018, the company, with respect to the Asia Pacific operations, has remediated poorly performing portfolios, decreased their exposure towards high hazard property business, they also rebalanced the portfolio towards more profitable segments, and they also revised reinsurance protection. We expect that these initiatives would support the QBE’s Asia Pacific operations and might also place the business in a position to cater to long-term growth. The net earned premium of the business declined 18% YoY and stood at $538 million, on a constant currency basis, because of top-line contraction along with higher reinsurance spend.

Asia Pacific Operations (Source: Company Reports)

Equator Re Ended FY 2018 with COR of 91.4%: QBE’s Equator Re business posted underwriting profit amounting to $58 million and its combined operating ratio stood at 91.4% as compared to the underwriting loss amounting to $350 million and a combined operating ratio of 140.9% in the prior year. The changes with regards to divisional reinsurance have contributed to a 6% reduction in Equator Re’s gross written premium in 2018, which declined to $1,486 million from $1,580 million in the previous year. The combined commission and expense ratio witnessed a rise to 13.4% in FY 2018 from 10.6% in the previous year.

Key Features for 2019 Reinsurance Program: QBE Insurance had recently stated that the finalised 2019 reinsurance program happens to be structured to better suit the company’s simplified portfolio and improving underwriting risk profile. The primary features for the program consist significantly reduced catastrophe retention, greatly increased protection against catastrophe severity, protection against the frequency of medium-sized catastrophes and significantly reduced large individual risk claim retention. The other important features include improved protection against the large individual risk claim severity and higher quota share protection to further cut down the claim’s volatility.

As on now, the group focuses on its three?years’ operational efficiency program targeting more than $200 million of gross cost savings by 2021 translating into net savings of $130 million over the same time horizon after underlying inflation and further investment in the Brilliant Basics program, technology and digitisation. Other key features consist of an expense ratio target of around 14% by FY 2021 which implies an improvement of approximately 1.5% and which is inclusive of very modest and selective premium growth and approximately $95 million of the restructuring costs which the company is targeting to incur between FY 2019- FY 2020.

Buy-Back Update: The company has updated the market about the progress on several transactions under its ongoing buy-back event. The company plans to deploy A$306 million in value towards the buy-back program. As of now, the group has bought back a total of 22,04,115 shares via on-market trade for the total consideration of A$2,72,82,602.84.

Future Drivers: QBE Insurance Limited happens to have a clear set of priorities for 2019 which are well-placed that might be building upon the progress which the company made in 2018. The company would be focused on the plan, supported by the rigorous performance management framework that would translate into further improvement in the attritional claims ratio. Also, the company plans to reduce the cost base by $130 million (net) in the span of three years which would help in the reduction of complexity, optimization of end-to-end processes and increasing the automation. Also, in FY 2019, the company plans to be focused on attracting and developing high-quality talent and building it for the future by deploying in and leveraging, data, analytics, and technology. The company would also continue to deploy towards the risk management capabilities which would help in recognizing the obligations to meet the expectations of shareholders, regulators, and communities in which the company operates. In FY 2019, the company has been targeting a combined operating ratio in the range of 94.5%-96.5% and the investment return in the range of 3.0%-3.5%.

.png)

Targets for FY 2019 (Source: Company Reports)

Stock Recommendation: QBE’s stock has been delivering decent returns from the past few months which might attract the attention of the market players at the current juncture. In the span of the previous six months, it posted a return of 13.42% while, in the span of the previous three months, it delivered 21.81% return. On the other hand, the company’s annual dividend yield stood at 4% which is in line with the industry median (Insurance) of 4%. Also, the company is expected to be aided by the deployments which have been targeted to support its future performance. Hence, considering the decent financials in FY18 along with favourable capital structure, turnaround positive cash RoE in FY18, lower than industry expense ratio, and at par dividend yield as compared to industry median, we give a “Buy” recommendation on the stock at the current market price of A$12.540 per share.

.png)

QBE Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...