Company Overview– QBE Insurance is an international property and casualty insurance company based in Australia, but it only writes about 24% of its annual gross earned premiums in its home country. Other regions include a large presence in North America (42% of premiums), Europe (26%) and Latin America and Asia Pacific (4% each). QBE offers a number of personal, commercial and specialty lines including property (33%), auto insurance (14%), agriculture (13%), public/product liability (12%), workers compensation (7%), marine (7%) and financial & credit (5%).

Analysis- Our investment thesis is for a recovery in earnings underpinned by improving insurance margins and productivity, rising insurance premiums, strong cash flow, and lower gearing. A spate of costly natural disasters in 2011 and 2012, combined with lower investment returns and acquisition indigestion, pushed down insurance margins from globally competitive levels in the high teens to decade lows of about 7% to 8%. The latest earnings downgrade in December 2013 was very disappointing and sets the recovery back about 12 months. Competitive advantages are derived from underwriting discipline and cost advantages. Longer term we expect stronger economic conditions in the U.S and higher northern hemisphere interest rates to boost returns.

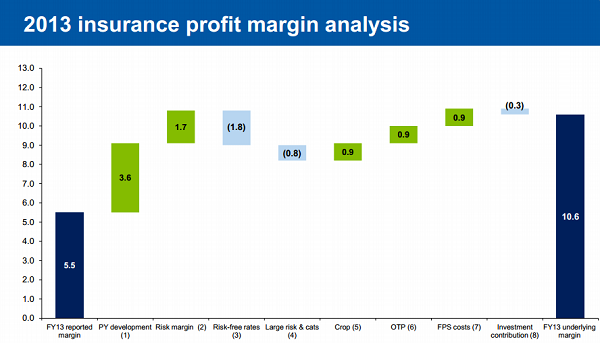

Insurance profit margin analysis (Source - Company Reports)

Insurance profit margin analysis (Source - Company Reports)

The cost reduction program is guided to reduce operating expenses by USD 250 million per year by 2015, but we believe this is a conservative estimate and the productivity improvement outcome will likely be materially better, delivering a sustainable base for higher medium to long term earnings growth. The 2013 financial year was a transition year with no major acquisitions likely and a painful USD 930 million in write downs. Despite the industry weakness, QBE insurance has successfully applied its large scale and risk management standards to produce a sustained period of underwriting profitability. We believe the positive dynamics dominate the financial results. Aggressive acquisition via expansion has more than doubled gross written premium during the past 10 years, generating returns strong enough to justify a long term competitive advantage. Strong competitive advantages, a lower cost base, normalization of investment returns are expected to see returns on capital above the cost of capital in the longer term. The focus on disciplined risk management and the strength of the business model is evident in the ongoing insurance underwriting profit - a characteristic most in the global industry have not achieved.

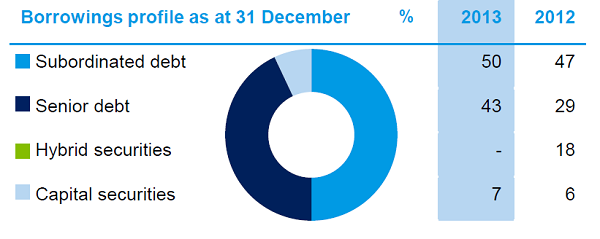

QBE Borrowings Profile (Source - Company Reports)

QBE Borrowings Profile (Source - Company Reports)

Unlike previous years we believe North America’s main specialty businesses, Crop and FPS are unlikely to be a material source of top line volatility in FY14. Of more concern is the likelihood that Gross Written Premiums (GWP) for the US$900m middle market business contracts as QBE seeks to remediate or sell it in the twilight of the recent hardening cycle. Encouragingly planting is progressing normally unlike last year’s very slow start. As at 20 May, 73% of corn acreage had been planted across a sample of 18 states that were responsible for 91% of total plantings in 2013. This compares to 65% in 2013 and a 5 year average of 76%. Although QBE is already factoring in low single digit rate increases and a 2% reduction in GWP for North America, we have taken a more conservative view given the top line track record in North America and potential disruption from the strategic review of the middle market business.

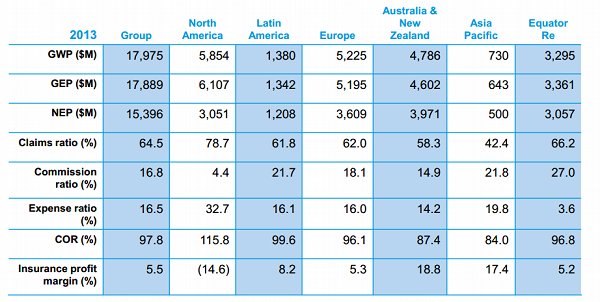

Divisional Performance (Source - Company Reports)

Divisional Performance (Source - Company Reports)

In Europe we understand that recent divestments have been broadly in step with expectations factored into guidance. QBE anticipated minimal rate increases in guidance for Europe but we believe that pricing over 2014 could become tougher than envisaged at the Feb result. Divestments appear to be proceeding in line with intentions at time of result. Europe’s flagged £300m reduction in premium for FY14 related almost entirely to the exit of a range of portfolios and businesses, a number of which have appeared in various insurance journals or have been reported by acquirers in recent months. In order of significance these include: (1) Inwards Reinsurance – We understand QBE planned to withdraw £120m of capacity due to expected soft reinsurance markets. (2) Aviation – Renewal rights to £60m of top end aviation businesses were recently sold to Brit. This business incurred losses in four of the past five years. (3) Central and Eastern Europe businesses – Sub scale businesses responsible for £20-30m of GWP. (4) Global Bloodstocks – Most likely a renewal rights sale. (5) Italian Medical Malpractice – Largely shut down already. 1Q Lloyd’s results highlights a tougher environment. Europe has been in a soft pricing cycle for some time, but through 2012/13 most Lloyd’s insurers managed to flat or modestly higher rates on renewal. Interim Management statements illustrated this was no longer the case in 1Q14.

Daily Chart QBE (Source - Thomson Reuters)

Daily Chart QBE (Source - Thomson Reuters)

With regards to Australia & New Zealand, Reflecting the global backdrop pricing conditions are only becoming more challenging. In QBE’s favor it has two businesses – Lenders’ Mortgage Insurance (LMI) and NSW CTP – that are largely immune to this and should deliver the majority of ANZ’s growth if current run rates can be maintained. QBE grew its NSW CTP book by 38% over 2013, increasing market share from 16% to 20%. Similar rates of growth are unlikely in FY14, however with pricing still the most competitive in the market further growth appears reasonably certain. The balance of QBE’s ANZ business is largely exposed to long tail commercial classes, where conditions remain relatively soft, or property classes where rate increase have now pulled back materially. There could be some downside risk in these areas, however on balance we believe that relatively modest expectations for inflation matching premium rate increases can be achieved.

We expect the external factors that caused so much damage in 2011, 2012 and 2013 will reverse in 2014 at the same time new management is reducing costs and gaining traction in the operational turnaround. Core competitive strength is sourced from superior insurance underwriting skills delivering underwriting profits in the long term despite increasingly expensive natural disasters. The robust global business model is leveraged to a stronger U.S economy, a recovery in the U.S dollar and long term U.S, European and U.K interest rates. We put a BUY on the stock at the current price of $11.12.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...