Company Overview - Qantas Airways Limited is an Australia-based company, engaged in providing airline services. The Company operates regional, domestic and international air transportation services. The Company’s business is the transportation of customers using two airline brands-Qantas and Jetstar. The Company operates in two operating segments: Qantas Brands and Jetstar. The Qantas Brand include its Qantas Domestic, which include the Australian domestic passenger flying business of Qantas Brands; Qantas International, which is the International passenger flying business of Qantas Brands; Qantas Loyalty Operates the Qantas customer loyalty program for Qantas Brands, and Qantas Freight, which is the air cargo and express freight business of Qantas Brands. The Jetstar Group are those operations of the Company’s which are dependent on the Jetstar fleet and the Jetstar Brand being the Jetstar passenger flying businesses.

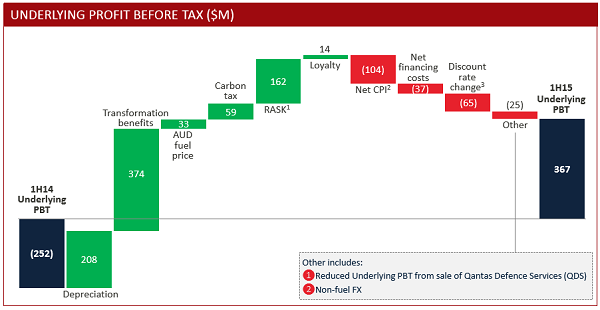

Analysis - Qantas (QAN) is an air transport services company that operates at both international and domestic levels. The Company has been in news recently in view of the release of its half year 2015 financial results that have been quite interesting in view of highlights such as underlying profit before tax of $367 million and statutory profit after tax of $206 million. The improvement in underlying profit before tax seems to be the best first-half performance since 2010. This was backed by the transformation benefits of $374 million and other factors such as reduced depreciation, lower fuel prices and increase revenue per available seat kilometre.

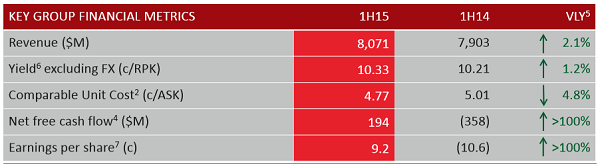

Financial Metrics (Source – Company Reports)

Qantas also highlighted that the comparable unit cost reduction was of the order of 4.8%. $1 billion of cash generation (up 44.8%) was reported from operations. Positive net free cash flow of $194 million with strong liquidity of $3.6 billion including $2.9 billion cash and $720 million in undrawn facilities were other updates. The revenue jumped up by 2.1% to $8.1 billion and the Company believed this to be based on progress with transformation, and recuperating yields and loads in a stabilizing environment. Planned capital expenditure remains at $900 million for FY15 and FY16. The earnings per share were reported to be 9.2 cents. The Company did not pay any interim dividend.

Underlying Profit before Tax (Source – Company Reports)

Various initiatives that have helped QAN in recent past include premium lounges in Los Angeles, launch of A330 product, food and beverage service for economy passengers, automatic SMS check-in for domestic passengers and the long-drawn-out inflight entertainment. Awards and accolades such as Roy Morgan Customer Satisfaction Awards, TripAdvisor Traveller’s Choice Awards, etc. add to the brand’s strength.

Unencumbered Fleet (Source – Company Reports)

QAN International recorded underlying EBIT of $59 million with a turnaround of $321 million on the prior corresponding period. The target of returning to profits is expected to be achieved in FY15. This segment saw a 3.8% reduction in comparable unit costs. Further, there was a 4.8% surge in revenue. Benefits could be leveraged from new airline partnerships and strengthening of existing partnerships in North America, South East Asia and Greater China. The Company reported a slump in competitor capacity growth in the international market from the compound annual growth rate of 7%.

Total Market Domestic Capacity Growth (Source – Company Reports)

The domestic segment’s underlying EBIT of $227 million i.e., an improvement of $170 million compared with the FY14 corresponding period was reported. Transformation benefits of $127 million with a 2.5% improvement in revenue per available seat kilometre was noted. QAN conveyed that 113 account renewals and 42 new accounts with 16 accounts regained from the competition helped in holding an 80% revenue share of accounts in the Australian corporate travel market. Collective underlying EBIT of about $300 million was reported for Qantas and Jetstar in the domestic market.

Jetstar individually reported underlying EBIT of $81 million indicating an improvement of $97 million compared with the same period last year. It reported EBIT of $63 million domestically given better yields and loads. The International arm witnessed $51 million as earnings in view of the network changes and introduction of the Boeing 787 Dreamliner. Other highlights include operation of Dreamliners for Jetstar’s long-haul flights from September 2015; growth in Asia (with flying to 66 destinations across 16 countries in the Asia Pacific region).

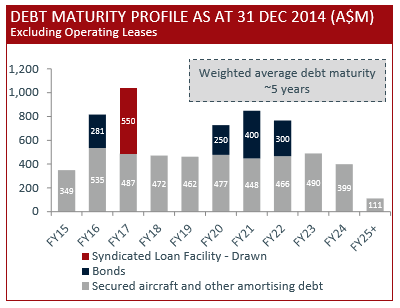

Debt Maturity Profile (Source – Company Reports)

Qantas Loyalty’s half-year underlying EBIT was up 10% to $160 million in comparison to the prior corresponding period. There was 6% increase in billings in view of diversification of customer base and revenue streams through growth ventures. There was a good 27% surge in activations of the Qantas cash travel money and membership card from 2H of FY14. QAN reported that more than 55,000 businesses joined Aquire. There has been a 70% increase in gross profit from ventures including Qantas Cash, Accumulate and Qantas Golf. Qantas Freight reported underlying EBIT of $54 million with an improvement of $43 million. A recovery in international cargo markets was witnessed with $44 million reported as the underlying EBIT. Good performance was noticed from China-US and US-Australia markets. Mixed economic environment led to a challenging domestic market.

QAN intends to have FY15 transformation benefits of $675 million which is a surge from the earlier declared target of $600 million. In fact, the total benefits of at least $875 million by 30 June 2015 are expected coupled with the $204 million FY14 benefits. With more or less a stable demand, moderate international market capacity, and stabilized yield and load factors, QAN’s outlook is noticed to be an improved one. QAN expects the capacity to increase by 1.5 to 2% in 2H of FY15 in comparison to 2H of FY14. All operating segments are expected to be profitable and full-year underlying fuel costs are estimated to be contained within $4 billion at current prices. QAN also believes that the full-year depreciation and amortisation expense will be around $1.1 billion. Nonetheless, QAN did not provide any profit guidance given the volatility and uncertainty associated with economic conditions, changes in government regulations, fuel prices and foreign exchange rates. Few days back, the Company also announced that it has taken a 51% controlling stake in Taylor Fry, a leading Australian and New Zealand analytics and actuarial consulting business. This will enable QAN to grow Qantas Loyalty’s data and analytics capability and further diversify earnings with a complementary adjacent revenue stream.

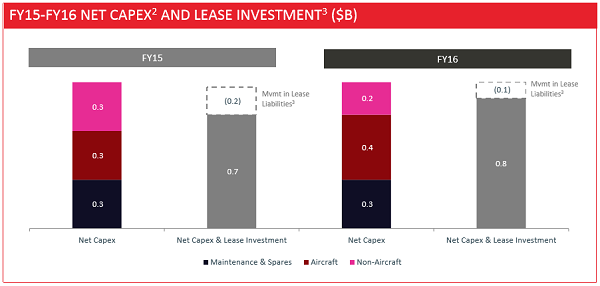

Capex Outlook (Source – Company Reports)

In the present scenario, the oil prices are serving as a catalyst for the Company. It is also noted that QAN is known to use options and swops on jet kerosene, gasoil and crude oil for hedging the exposure to fluctuating prices of aviation fuel. The Company had hedged 85% of fuel requirement in 2H15 as at 28 November 2014. Further softness in fuel price coupled with cost transformation momentum may give a further edge to QAN. It appears that the Company is well-protected in near-term given the fuel cost and currency standing in comparison to its peers. The recently provided outlook is appealing given lower costs and a lucid competitive environment. The ratings agency, Moody’s has also elevated its outlook on the Company from negative to stable in view of the better than expected half-year results. FY16 may serve as a peak profit year in support of the gains that QAN may fetch from transformation efforts and fuel savings. The Company may also post an underlying profit before tax of about $1 billion this year which will be a great step. Possibilities such as a share buyback needs to be closely watched. There is also news that the Company expects to bank a $500 million oil bonus over the remaining FY15 while it draws benefits from the Organisation of the Petroleum Exporting Countries’ war on US onshore oil producers. Of course, certain hiccups such as challenging of QAN’s view on relaxing the rules governing air routes to Australia to encourage more Australians to fly overseas, by the Productivity Commission do not look to weaken the potential.

Qantas Daily Chart (Source - Thomson Reuters)

Based on the foregoing, we put a BUY recommendation for this stock at the current price of $2.89.

.png)

Please wait processing your request...

Please wait processing your request...