Kalkine has a fully transformed New Avatar.

Company Overview: PWR Holdings Limited (ASX: PWH) is engaged in the design, prototyping, production, testing, validation and sales of advanced cooling products and solutions to the motorsports, automotive original equipment manufacturing, automotive aftermarket, and emerging technologies sectors for domestic and international markets. The group has two operating segments, namely- PWR Performance Products which includes its Australian and European operations, and C&R, which comprises its USA operations.

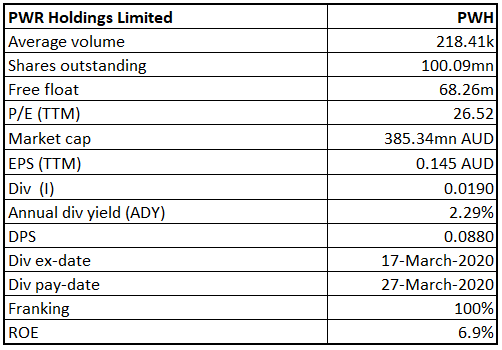

PWH Details

.png)

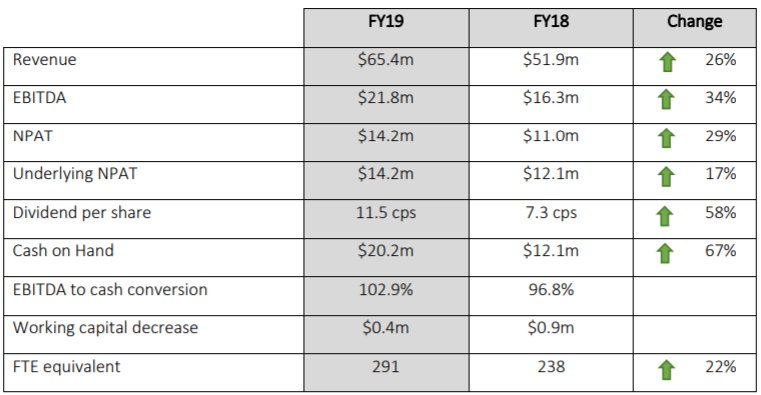

Decent Growth in Revenue and Healthy Balance Sheet: PWR Holdings Limited (ASX: PWH) is engaged in the design, prototyping, production, testing, validation and sales of advanced cooling products and solutions to the motorsports, automotive original equipment manufacturing, automotive aftermarket, and emerging technologies sectors for domestic and international markets. As on 19 May 2020, the market capitalization of the company stood at ~$385.34 million. During FY19, the group achieved overall revenue growth of 26.1% as compared to the prior corresponding period, which stood at $65.41 million. This was primarily driven out of Europe, where sales increased by 40%. Sales in the Australian and American markets were stationary, although activity at both these manufacturing operations increased significantly to support the increased sales in Europe. In the same time span, the company reported higher EBITDA with an increase of 23.6% to $21.76 million. This was mainly due to growth in overall revenue at consistent margins, a steady increase in production and overhead costs with an increase in sales volume and a lower rate of increase in administration and overhead costs than sales. The company also reported a growth of 29% in NPAT to $14.2 million. Over the span of 4 years from FY15 to FY19, the company witnessed a CAGR of 19.08% in revenue and a CAGR of 19.61% in gross profit. This reflects a robust operating model of the company which supports customer and technology enhancements. During the year, PWH reported a healthy and robust balance sheet with a net positive cash position. The decent financial and operational performance enabled the Board to increase its total dividend per share by over 57% from FY2018 and paid 11.5 cents per share as compared to 7.3 cents per share in FY18.

The company has also released its interim results for the period ended 31 December 2019, wherein it saw a significant portion of growth from its diversification strategy, emerging technologies, and OEM customers. PWH has a continued focus on working capital utilization and is well advanced in technology for potential future growth opportunities.

The company is focused on its strategy of managing growth which has its own set of challenges and demands. It is aiming to build capability, systems, and processes to support profitable growth, and is focused on diversifying its revenue base through new products and industries.

FY19 Financial Highlights (Source: Company Reports)

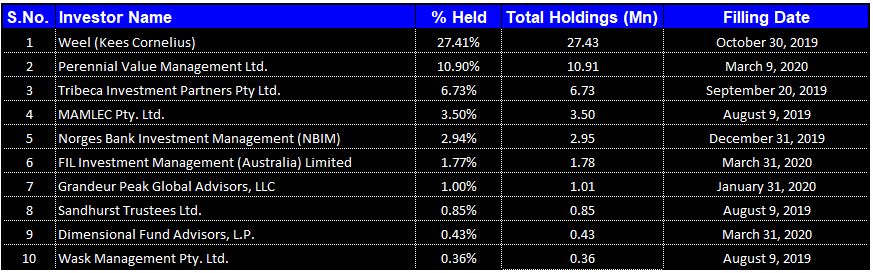

Details of Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of PWR Holdings Limited. Weel (Kees Cornelius) is the largest shareholder in the company, with a percentage holding of 27.41%.

Top 10 Shareholders (Source: Refinitiv, Thomson Reuters)

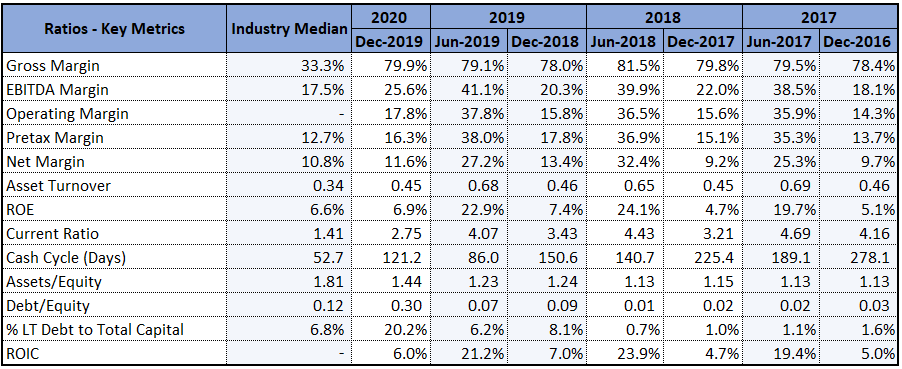

Increased Profitability and Financially Stable Balance Sheet: During 1H20, gross margin of the company stood at 79.9%, higher than the industry median of 33.3%. In the same time span, net margin of the company was 11.6% as compared to the industry median of 10.8%. The higher gross and net margin indicate that the company is managing its costs well and is capable of converting its revenue into profits. During the half year, EBITDA margin of the company stood at 25.6%, higher than the industry median of 17.5%, reflecting increased profitability. In the same time span, Return on Equity of the company was slightly higher than the industry median and stood at 6.9%. This indicates that PWH is well managing the capital of its shareholders and is capable of generating profits internally. During 1H20, current ratio of the company was 2.75x, higher than the industry median of 1.41x. This indicates that the company is liquid enough to pay off its current liabilities using its existing assets. In the same time span, Assets/Equity ratio of the company was 1.44x, and Debt/Equity ratio stood at 0.30x, as compared to the industry median of 1.81x and 0.12x, respectively. This indicates that the business is financed with a significant proportion of investor funding and a small amount of debt, resulting in a financially stable balance sheet.

Key Margins (Source: Refinitiv, Thomson Reuters)

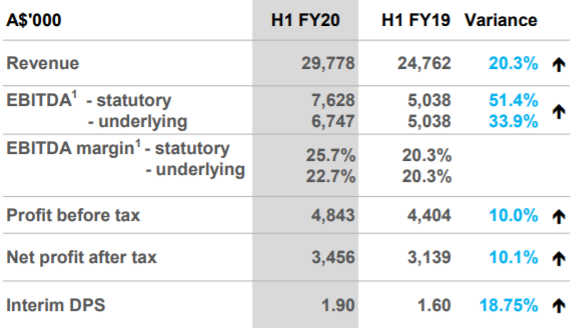

Decent Increase in Revenue and EBITDA: During 1H20, the company reported an increase of 20.3% in revenue to $29.8 million. This was mainly due to growth across all primary categories, with 82% of revenue growth from emerging technologies and OEM categories. In the same time span, statutory EBITDA of the company went up by 51% to $7.6 million, and EBITDA margin witnessed an increase of 12% to 22.7%. This was mainly because of higher volumes, efficiencies of scale and exchange rate movements. The increased revenue and higher EBITDA and EBITDA margin resulted in a rise of 10% in NPAT to $3.5 million. The decent financial and operational highlights enabled the Board to declare a fully franked interim dividend of 1.90 cents per share, reflecting an increase of 19% on the pcp. During the half-year, the company reported higher working capital which resulted in an increase of 24% in operating cash flow to $4.6 million. In the same time span, the company reported a stable balance sheet with a cash balance of $7.9 million and long-term debt of £2 million. The company also reported $12 million of unutilized finance facilities.

During 1H20, the company reported an improved performance in both of its segments with an increase in segment revenue to ~$22.9 million in PWR Performance Products and $8.3 million in C&R, up from $20.37 million and $6.45 million, respectively. The decent increase in revenue resulted in higher operating EBITDA in both segments.

1H20 Financial Performance (Source: Company Reports)

Future Expectations and Growth Opportunities: The company has expanded its capital expenditure program for FY20 and FY21 for projected growth and productivity benefits. It has ramped up its OEM programs which will impact its category composition. The company has hedged its US operations through C&R, and the portion of debt from C&R to PWR has been converted to equity, reflecting financial stability. The company is closely monitoring developments in Brexit. The group will continue to pursue its strategy of increasing profitability and market share within existing markets and will take up opportunities in emerging markets in the coming financial years.

Like all businesses, this is an uncertain time for PWR Holdings. However, the company is maintaining a strong balance sheet and a solid working capital position to proactively mitigate the impact of the coronavirus on its business and customers. PWH remains committed to its planned investment in CAPEX to support its growth in new market sectors such as emerging technology, aerospace, and defence. The company expects to complete 36 races as The National Association for Stock Car Auto Racing (NASCAR) has resumed operations from 17 May 2020.

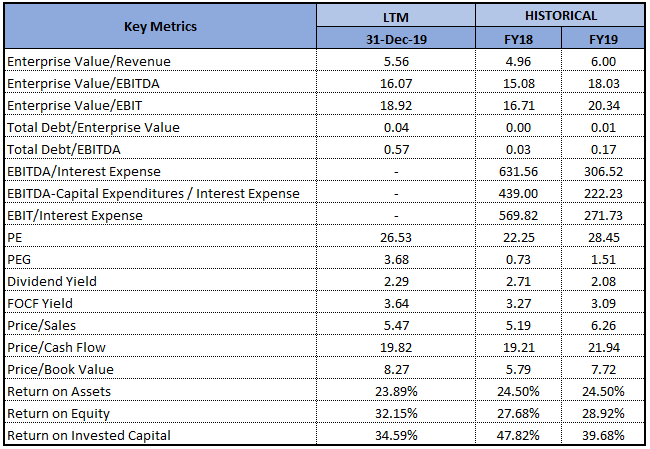

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

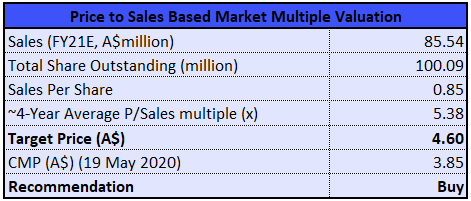

Valuation Methodology: Price to Sales Based Market Multiple Valuation Approach (Illustrative)

Price to Sales Based Market Multiple Valuation Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of PWH gave a return of 15.62% in the past one month and is trading slightly above the average of its 52-weeks’ band of $2.5 - $5.160. The diversified cost base and resilient business model place the company in a strong position to capitalize on emerging market opportunities. Despite the outbreak of COVID-19, the company is well-capitalized with a financially stable balance sheet and sufficient liquidity. Considering the decent returns in the past one month, resilient financial position, improvement in fundamentals, and positive long-term outlook, we have valued the stock using price to sales based market multiple valuation approach, and have arrived at a target price of low double-digit growth (in percentage terms). Hence, we recommend a ‘Buy’ rating on the stock at the current market price of $3.850 on 19 May 2020.

PWH Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...