Company Overview: Pushpay Holdings Limited is engaged in the provision of a platform for mobile commerce and electronic payments, and tools for merchants to engage with consumers. The Company focuses on the development and deployment of mobile payment solutions. The Company's solutions include Event Registration, 3D Touch, echurch Apps, Pushpay Fastpay and Virtual Terminal/Envelope Giving. The Company caters to various markets, such as the faith sector, non-profit organization's and enterprises both small medium enterprises and corporate organizations. The Company's subsidiaries include eChurch Inc, eChurch Inc, Pushpay IP Limited, Pushpay Pty Limited, Pushpay Trustees Limited, Pushpay NZ Limited and ZipZap Processing Inc.

.png)

PPH Details

Strong Track Record of Delivering on Guidance: Pushpay Holdings Limited (ASX: PPH) is a provider of a donor management system, including donor tools, finance tools and a custom community app, to non-profit organisations and education providers in Canada, Australia, New Zealand and the US. Looking at the performance over the period FY15 to FY19, the company witnessed a CAGR growth of 170.4% in top-line with FY15 revenue amounting to US$1.84 million and FY19 revenue amounting to US$98.37 million. In addition, the business turned profitable in FY19, amounting to US$18.83 million, against a loss of US$23.27 million in FY18.

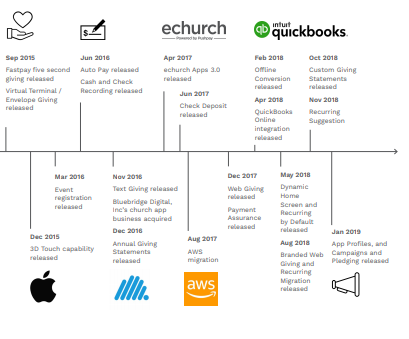

The company has continued to invest in leading solutions, including the release of Campaigns and Pledging functionality in January 2019. In the same month, the company released App Profiles, a foundational capability that enables the company to increase the level of personalisation into its products. In November 2018, the company launched Recurring Suggestion across its customer base, that identifies patterns in regular givers’ behaviour using machine learning. Custom Giving Statements launched in October 2018 enabled customers to create and distribute customer statements at any point during the year. Recurring Migration, Branded Web Giving, Recurring by Default, Dynamic Home Screen and QuickBooks® online were some other solutions launched prior to October 2018.

Going forward, the company expects to deliver continued strong revenue growth by gaining further market share in the medium-term and, in turn, maximising the returns for shareholders. In addition, the company is eyeing potential strategic acquisitions to broaden its growth prospects and add significant value to the current business.

Addition to Pushpay’s Solutions (Source: Company Reports)

Key Highlights of FY19 Results: During the year ended 31 March 2019, the company generated revenue amounting to US$98.4 million, up 40% on prior corresponding period revenue of US$70.2 million. Operating revenue for the period increased to US$95.9 million, up 42% on prior corresponding period revenue of US$67.7 million. The period saw a positive EBITDAF of US$1.6 million, against prior corresponding period loss of US$18.6 million. Net profit after tax during the period, stood at US$18.8 million, increasing 181% on prior corresponding period loss of US$23.3 million. During the year, average revenue per customer was reported at US$1,315 per month, up 33% in comparison to US$989 per month in FY18. The increase in ARPC is attributable to multiple factors, including an increase in subscription fees from new and existing customers, development of product set and incoming of medium & large customers. Staff headcount during the year went up to 389, increasing 11% on prior corresponding period count of 350. Total customers increased by 5%, from 7,276 in FY18 to 7,649 in FY19.

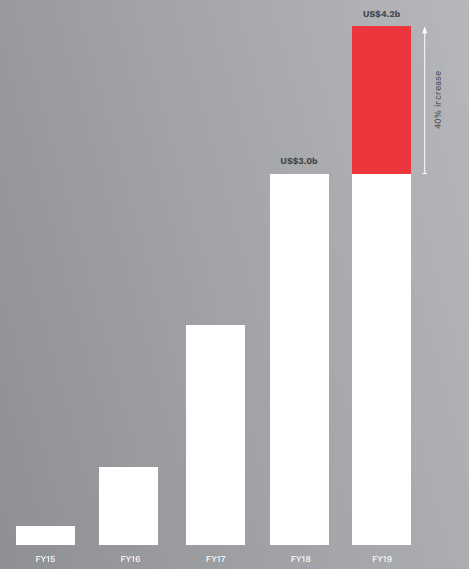

Annualised Processing Volume (APV): During the year, the annualised processing volume went up by 40% to US$4.2 billion from US$3.0 billion in prior corresponding period. Over the period starting FY15 to FY19, the company witnessed a continuous increase in the annualised processing volume. Going forward, the company expects the growth in APV to be continued on the back of larger proportion of new medium and large customers, increased adoption of digital giving in the US faith sector, increased giving to religion in the US and further development of its product set.

Growth in Annualised Processing Volume (Source: Company Reports)

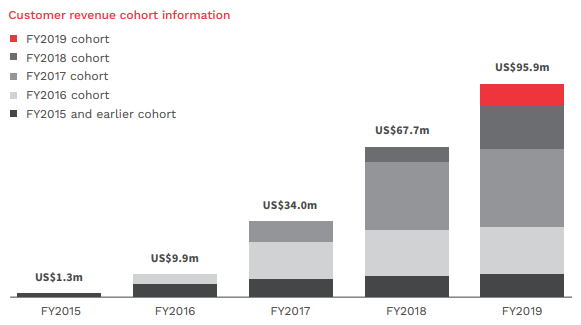

Customer Revenue Cohort: Over the period, the company has strengthened its business model on the back of consistent revenue from Customer cohorts, joining the company’s platform at different times in history. Total customer cohort revenue in FY19 was reported at US$95.9 million, up from US$67.7 million in FY18.

Revenue from Customer Cohorts (Source: Company Reports)

Improved Operating Leverage: As the operating revenue increased by 42% with operating expenses remaining stable, the percentage of operating expenses in comparison to operating revenue improved by 28 percentage points in FY19 to 65% in comparison with operating leverage ratio of 93% in FY18. Furthermore, the company expects further improvement in operating leverage as operating revenue continues to increase and growth in total operating expenses remains low.

FY19 Guidance Delivered: In FY19, the company delivered on its total revenue guidance with an increase of 40% over prior corresponding period. Growth during the period, was backed by investment into product design and development, implementation of business strategy and growing team capabilities. In the coming years, the company expects to see consistent revenue growth on the back of increased efficiencies and further market share in the US faith sector. During the year, the company delivered on its gross margin guidance. For the year ended 31 March 2019, the gross margin increased to 60% from 55% in prior corresponding period. EBITDAF guidance of FY19 was also met with a growth of 108% over the prior year.

Recent Updates:

(a) Change in Director’s Interest: The company recently updated that Christopher Peter Huljich, one of the directors, transferred 2,150,000 ordinary shares to Link Market Services Limited on account of off-market transfer of shares for benefit of various parties to pursue philanthropic interests. On account of the same underlying purpose, another director of the company, Peter Karl Christopher Huljich also disposed the same number of shares to Link Market Services Limited.

(b) Appointment & Resignation of Director: Recently, the company appointed Justine Smyth as a new Director on its Board, effective from 26 August 2019. In addition, he is also serving as the Chairman of the Audit and Risk Management Committee and a member of the Nominations and Remuneration Committee. Total remuneration package for the new director was reported at US$95,000. Alongside the new appointment, Daniel Steinman resigned from the Board of Directors.

(c) Update on Bookbuild: In the month of July 2019, the company announced a fully underwritten bookbuild to facilitate a partial sell down of ordinary shares held by Chris Heaslip. Chris Heaslip resigned from the position of CEO in May 2019. The bookbuild closed successfully, comprising sale of 12.24 million shares at the clearing price of NZ$3.70 per share. Total value of the bookbuild stood at NZ$45.3 million. The company attracted 13 institutional investors across Hong Kong, the US, Australia and New Zealand for subscribing to the bookbuild, with strong participation from retail investors.

(d) Appointment of CEO: The company appointed Bruce Gordon as the new CEO and Executive Director on the Board upon Chris Heaslip, vacating the position on 31 May 2019.

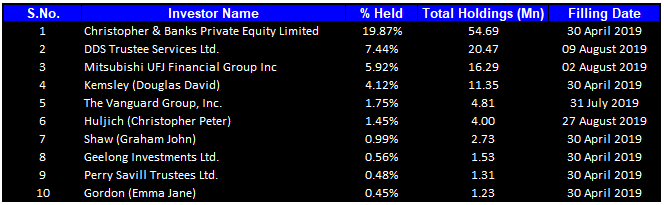

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 43.02% of the total shareholding. Christopher & Banks Private Equity Limited holds the maximum interest in the company at 54.69%, followed by DDS Trustee Services Ltd., holding 20.47% of the shares.

Top Ten Shareholders (Source: Thomson Reuters)

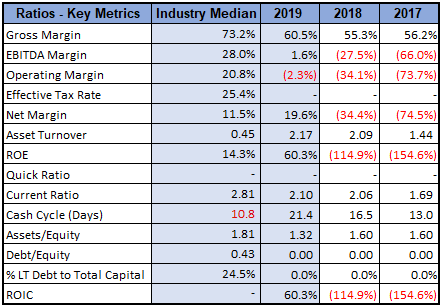

Key Metrics: In FY19, the company had a net margin of 19.6%, which was higher than the industry median of 11.5%. Current ratio for the year was reported at 2.10x as compared to FY18 ratio of 2.06x and FY17 ratio of 2.06x, reflecting a continuous improvement in the company’s ability to meet its short-term obligations. Gross margin in FY19 also improved in comparison to prior corresponding period.

Key Metrics (Source: Thomson Reuters)

What to Expect: In FY20, the company expects operating revenue to be in the range of US$122.5 million – US$125.5 million. Gross margin for the period is expected to exceed 63%. FY20 EBITDAF is expected to be in the range of US$17.5 million and US$19.5 million. Total processing volume is anticipated to be between US$4.6 billion and US$4.8 billion. Looking at the company’s strong track record of delivering on its guidance, revenue in the future is expected to witness continued growth through continuous execution of business strategy and increased market share. Furthermore, the company is targeting over 50% of the medium and large church segments, that represents a potential of over US$1 billion in annual revenue. Pushpay expects to maintain a continued balance in the expanding operating margin with opportunities to boost revenue. Overall, the company is aiming to maintain high efficiency in its operations through maintenance of cost throughout the business.

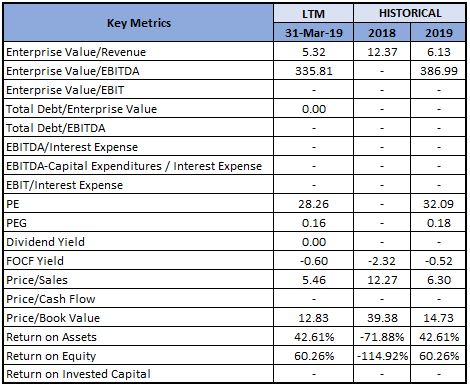

Key Valuation Metrics (Source: Thomson Reuters)

Stock Recommendation: The stock of the company generated negative returns of 10.73% and 22.04% over a period of 1 month and 3 months, respectively. Since its listing in August 2014, the company holds a strong track record of delivering on guidance, with performance either in-line or above the guidance provided. In FY19, the company delivered decent growth across all key metrics achieved through targeted implementation of its strategy and enhanced product design & development through responsible investment. Subscription revenue for the year stood at US$26.66 million, increasing 35% on prior corresponding year. Processing revenue witnessed an uplift of 44% in comparison to pcp at US$69.25 million. The company is primarily focused on medium and large customer segments that contribute higher ARPC and, thus, revenue. The percentage of medium and large church customer in comparison to total customers in FY19, increased to 55.7% from 51.5% in FY18. Gross margin during FY19 also improved, with further growth expected from the margin improvement program over the coming year. Going forward, the company is expecting a further boost in operating revenue with growth in the range of 27.74% and 30.87%. FY20 is further expected to report an improvement in gross margin and a significant increase in EBITDAF. Moreover, the company also expects to achieve significant operating leverage with further growth in revenue through strong financial discipline. Considering the aforesaid factors, we recommend a “Buy” rating on the stock at the current market price of $2.830 as on 30 August 2019.

PPH Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...