Company Overview: Pushpay Holdings Limited is engaged in the provision of a platform for mobile commerce and electronic payments, and tools for merchants to engage with consumers. The Company focuses on the development and deployment of mobile payment solutions. The Company's solutions include Event Registration, 3D Touch, echurch Apps, Pushpay Fastpay and Virtual Terminal/Envelope Giving. The Company caters to various markets, such as the faith sector, non-profit organization's and enterprises both small medium enterprises and corporate organizations. The Company's subsidiaries include eChurch Inc, eChurch Inc, Pushpay IP Limited, Pushpay Pty Limited, Pushpay Trustees Limited, Pushpay NZ Limited and ZipZap Processing Inc.

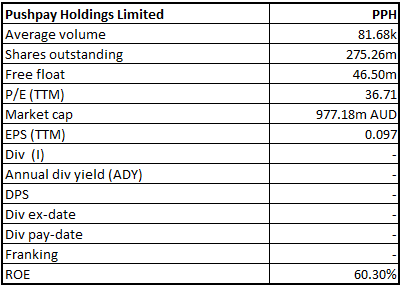

PPH Details

Strong & Sustainable Financial Performance: Pushpay Holdings Limited (ASX: PPH) designs and develops mobile payment application and solutions used by a wide range of customers, including users who donate to charities and non-profit organizations in the US, Canada, Australia and New Zealand. The IT company (with a market capitalization of circa $977.18 million, as at 31 May 2019) operates across the globe to simplify engagement, payments, and administration which helps customers to increase participation and build stronger relationships with their communities. The company is a leading cloud-first solution provider with a global footprint and brand consolidation. The success of the company is underpinned by the growth in two key factors including Average Revenue Per Customer and Annualized Processing Volume. The company has grown substantially since its IPO (i.e., 2014). It exhibited sustainable growth on the back of expanded operating margins, strong revenue growth, and its first positive EBITDAF in FY19. Broadly, the group is subject to various financial risks including liquidity, credit and market risks. However, the company has specific risk management objectives and policies set out to mitigate these risks. The company with its strong and sustainable financial performance along with robust business drivers is on the track to reap the benefits going forward.

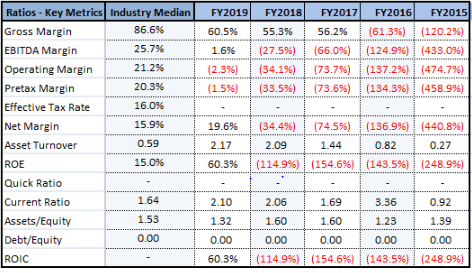

Key Metrics (Source: Thomson Reuters)

Industry Recognition: Several accolades have been achieved by the company, reflecting the quality of its people, product & processes. The success of the company is a testament to the dedication and commitment to excellence of the team. The company has been placed 11th in the Australian Financial Review Most Innovative Companies List and was recognised with three awards in 2018 Best in Biz International Awards, including silver in the Fastest-Growing Company of the Year - Medium and Large category. Moreover, there are several other awards & recognition that the company has achieved till date.

Industry Recognition (Source: Company Reports)

Business Strategy: The customer base of the company increased by 373. The customers over the year to 31 March 2019, moved up from 7,276 to 7,649 with an increase of 5%. The company is well progressing with its strategy of modest growth in the number of new customers and a significant increase in the proportion of new medium and large customers. Over the year to 31 March 2019, Pushpay’s proportion of medium and large customers was increased from 51% to 56%. The company expects customer numbers to steadily grow over the remainder of the financial year to 31 March 2020. The primary focus of the company is on increasing revenue by attracting a larger number of medium and large customers, while expanding Average Revenue Per Customer (ARPC) and increasing retention.

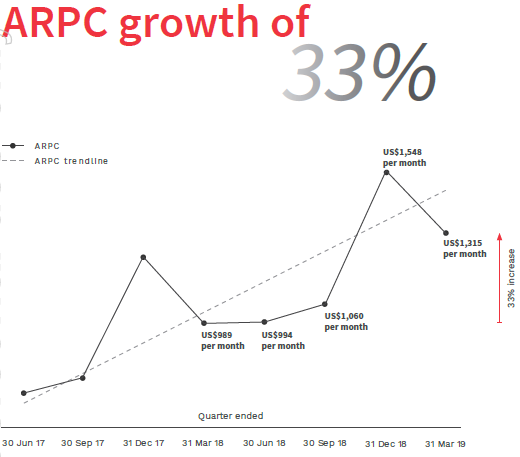

The Average Revenue Per Customer (ARPC) increased by US$326 per month over the year to 31 March 2019. The 33% increase from US$989 per month to US$1,315 per month was driven by several factors like increased subscription fees from new and existing customers, and a larger proportion of medium & large new customers.

ARPC Growth (Source: Company Reports)

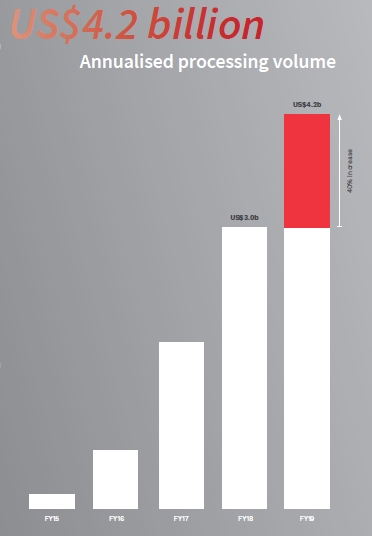

The annualized processing volume increased by 40.0% Y-o-Y to US$4.2 billion in FY19 as compared to $3.0 billion in FY18. The company process ~18.9 million transactions with an average transaction value of US$192 million over the year.

Annualized Processing Volume (Source: Company Reports)

The continued growth in Annualised Processing Volume is expected on the back of a larger proportion of new medium & large customers and further development of the product set which will result in higher adoption & usage.

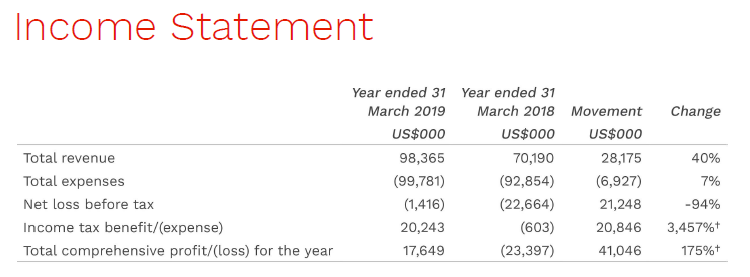

Key Financials: The company maintained its strong track record of delivering on guidance since its listing in 2014. The total revenue of the company increased by US$28.2 million from US$70.2 million to US$98.4 million in FY19, an increase of ~40% driven by the targeted implementation of the strategy, growing team capabilities & expertise, and responsible investment into product design & development. The annual revenue retention rate remained substantially stable over the year to 31st March 2019.

Income Statement 1HFY19 (Source: Company Reports)

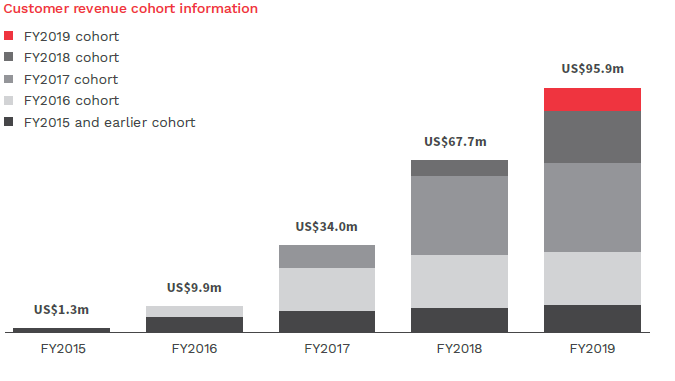

The strength of the business is in the generation of consistent revenue from each cohort. The increase in revenue from remaining customers growing within a cohort offset the decline in revenue from customers who are leaving the platform as exhibited in the below chart.

Revenue Cohort Information (Source: Company Reports)

The Earnings before Interest, Tax, Depreciation, Amortisation and Foreign Currency (gains)/losses (EBITDAF) for the company increased by US$20.2 million in FY19. The company exhibited108.0% increase from a loss of US$18.6 million to a gain of US$1.56 million. However, theNPAT grew by US$42.1 million over the year ended 31 March 2019, from a net loss of US$23.3 million to a net profit of US$18.8 million, an increase of ~181%, primarily on the back of recognized deferred tax asset of US$20.9 million.

Gross margin of the company improved from 55% to 60% in FY19. The company undertook a diligent approach to optimize gross margin which has driven satisfying results. The company expects to continue to benefit from the margin improvement program over the coming year.

The operating revenue of the company increased by 42.0% in FY19, however, the total operating expenses remained stable. The total operating expenses improved by 28 percentage points, as a percentage of the operating revenue. The company is expecting significant operating leverage to accumulate as it continues to increase the operating revenue and the rate of growth in total operating expenses at the lower levels. The months to recover CAC (Customer Acquisition Cost) was less than 18 months for the company and remained stable over the year to 31st March 2019.

Early in the development phase, the company adopted best in class software tools and scalable processes. The strong financial discipline along with the initial investments, will enable the company to achieve significant operating leverage with the growth in revenues.

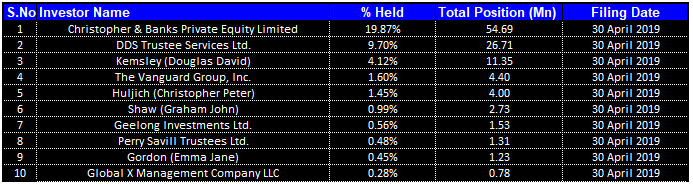

Top 10 Shareholders: Top ten shareholders of the company form around 39.51% of the total shareholding as highlighted in the below table. Christopher & Banks Private Equity Limited holds the maximum interest in the company with a stake of 19.87% followed by DDS Trustee Services Ltd and Kemsley (Douglas David) with a stake of 9.70% and 4.12%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

Key Risks: The group is subject to several financial risks including liquidity risk, credit risk, and market risk, however, it does not trade financial instruments, including derivative financial instruments, for speculative purposes. The group manages its capital to ensure that entities in the group will be able to continue as a going concern while maximising the return to the shareholders using optimal debt and equity. The company faces interest rate risk arising out of its cash & cash equivalents balance. These are placed on deposit at variable rates which exposes the company to cash flow interest rate risk.

Guidance & Outlook: The total processing volume for FY20 has been guided in the range of US$4.6 billion and US$4.8 billion. The company expects strong revenue growth to continue driven by the execution of the strategy to increase further market share in the medium-term. Going forward, the company will continue its balanced approach in expanding the operating margin along with the opportunities to increase revenue growth. The focus of the company will be on ensuring high efficiency while maintaining the cost discipline across the business. It will continue to evaluate potential strategic acquisitions to expand the current business and add significant value to it.

As per the company guidance for the year ending 31 March 2020, the operating revenue is expected to be in the range of US$122.5 million and US$125.5 million. The company expects a gross margin of above 63%, EBITDAF of between US$17.5 million and US$19.5 million and a total processing volume of between US$4.6 billion and US$4.8 billion for FY20.

Stock Recommendation: The operating cash flow of the company remained negative over the years, although the improvement was seen on a consistent basis. The initial investments for business operations are one of the primary reasons of experiencing consistent negative cash flows. However, it exhibited improving financial performance along with strong business drivers. With consistent and sustainable performance in the past few years, decent guidance, resilient growth outlook, etc., Pushpay is well placed to attain higher growth in the future. Hence, considering the above key factors, we recommend a “Buy” rating on the stock at the current market price of $3.530 per share (down 0.563% on 31 May 2019), and expect single-digit growth in the next 12-24 months.

.png)

PPH Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...