Kalkine has a fully transformed New Avatar.

Company Overview: Pro Medicus Limited produces integrated software applications for the healthcare industry. The Company's principal activities are the supply of healthcare imaging products and services to hospitals, diagnostic imaging groups and other health related entities in Australia, North America and Europe. The Company's segments include Australia, Europe and North America. Its products and services include Radiology Information Systems (RIS) and Visage 7.0. RIS offers medical software for practice management (RIS); training, installation and professional services; after sale support and service products; Promedicus.net secure e-mail, and digital radiology integration products. The Company's Visage 7.0 offers medical imaging software; picture archiving and communications system (PACS)/digital imaging software; training, installation and professional services, and service and support products. Its subsidiaries include Promed (USA) Pty Ltd, PME IP Australia Pty Ltd and Visage Imaging Inc.

.png)

PME Details

Major Contracts to Drive Operational Performance: Pro Medicus Limited (ASX: PME) is a leading medical imaging IT provider. The company provides a full range of radiology IT software and services to hospitals, imaging centers and health care groups worldwide. The company has also purchased Visage Imaging, that is a global provider of leading-edge enterprise imaging solutions. The company’s offices are located in Melbourne, Berlin, and San Diego. During the year ended 30 June 2019, the company witnessed an increase of 47.9% in revenue, with performance largely driven by strong growth in transaction revenue from new and existing customers in North America. Moreover, the company continued to expand its footprints in the region via two key contracts with Partners Healthcare and Duke Health. Underlying net profit after tax for the year went up by 83.1%, and NPAT increased by 91.9%. Cash reserves at the end of the period amounted to $32.32 million, representing an increase of 28% on the prior corresponding year. The company had a strong balance sheet position at the end of the period with zero debt. The period was also marked by increased investments in research and development for both the Visage 7 and Visage RIS products, for further development in the business.

Going forward, the company will be focused on developing new products and continued development of its Visage RIS and Visage 7.0 product sets. The above strategy is expected to support the company’s position as a market leader and will enable the group to further leverage its expanded product portfolio and geographical spread.

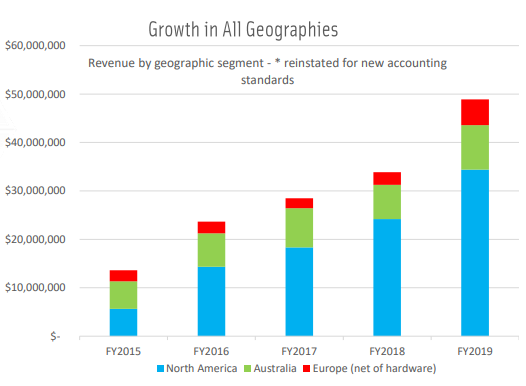

Looking at the performance over a period of 4 years covering FY15 – FY19, the company has reported a remarkable top-line CAGR of 30.1%, with FY15 and FY19 revenue amounting to ~$17.49 million and ~$50.11 million, respectively. Bottom-line CAGR for the above-mentioned period stood at 56.1%, with FY15 and FY19 profit of ~$3.22 million and ~$19.13 million, respectively. Moreover, the company has maintained a continuous upward trend in revenue and profit in all these five years. In terms of geography, the company has seen remarkable uplift in the North American business, which was a key contributor to FY19 results. In addition, the company witnessed solid contribution from other geographies, including Australia and Europe.

Performance by Revenue (Source: Company Reports)

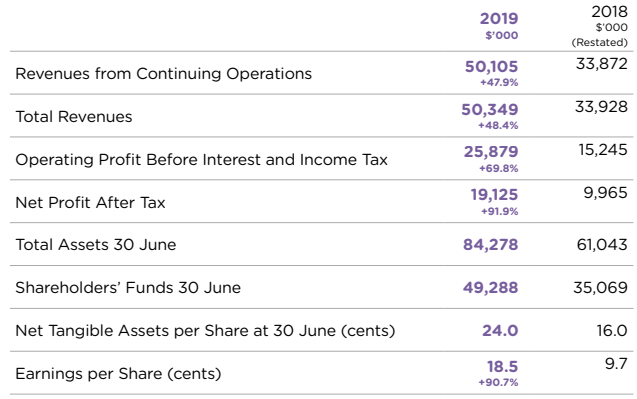

FY19 Financial Highlights: During the year ended 30 June 2019, the company reported revenue amounting to $50.11 million, representing an increase of 47.9% on prior corresponding period. Net profit after tax came in at $19.13 million, up 91.9% on the previous year. Reported net profit after tax witnessed a reduction on account of a change in accounting standards regarding revenue recognition. The change in accounting standards also resulted in revenue of $22.91 million being deferred to future periods. Underlying profit after tax was reported at $22.74 million, representing an increase of 83.1% on the previous year. At the end of the period, the company had cash reserves amounting to $32.32 million, representing an increase of 28.0% on the previous year. Dividends also went up drastically to 10.5 cents per share, representing an uplift of 75.0% on prior corresponding period.

FY19 Results (Source: Company Reports)

Performance by Geography

(a) Australia: The company’s operations in the region comprise of research and development of the Visage RIS and e-health products. Alongside, the company is also engaged in sales and services support functions of both Visage RIS and Visage 7 products. Revenue from the region went up by 30.2% in comparison to the previous year, driven by the progressive implementation of Visage RIS fulfilling the 5-year contracts with Healius and I-MED Network Radiology. Performance was also driven by new contracts secured in the region. The company’s e-health offering in Australia also experienced modest growth throughout the year.

(b) North America: The period was characterised by signing of multiple key contracts by the company. In July 2018, the company inked a 7-year transaction-based deal with Carle Foundation, worth $5 million. Another significant contract was signed in November 2018, comprising a 7-year deal with Partners Healthcare for $27 million. Partners Healthcare is one of the largest health providers in North America. Under the contract, the company’s Visage 7 technology will be implemented at two flagship hospital systems, including MGH and BWH. In February 2019, the company renewed its contract with the Veteran Affairs (VA) Midwest Health Care Network (VISN 23), for another 5 years. Another major contract was signed in April 2019, with Duke Health, the largest health systems in North Carolina. The contract covers a period of 7 years, with a consideration of $14 million. As per the service terms, PME’s Visage 7 technology will be implemented across the radiology departments at Duke Health. The technology will also be integrated into Duke’s electronic health record (EHR). During the year ended 30 June 2019, North America became the largest contributor to overall performance, with revenue rising at a rate of 42.2% in comparison to the previous year. Revenue growth was driven by an increase in transaction volumes for existing clients that provided a boost to transaction-based revenue.

(c) Europe: Revenue from the European operations witnessed an increase of 102.3% in comparison to the previous year. In December 2018, the company announced the extension of its contract with a large German Government Hospital network.

Going forward, the company will continue to invest in R&D for its flagship Visage 7 suite of products, including the Visage 7 Viewer and Visage 7 Open Archive, which will continue to differentiate its offerings. Moreover, the next financial year will bring in more opportunities due to improved prospects in North America and the continued commercialisation and roll out of Visage RIS, the company’s new technology RIS platform.

Recent Updates:

Presentation at RSNA Conference: The company recently updated that Visage Imaging Inc., its wholly owned subsidiary in the U.S, showcased the Visage AI Accelerator solution and the new Visage developed breast density classification algorithm at the Radiological Society of North America (RSNA) conference. Visage AI Accelerator represents a new semantic annotation functionality to optimise curation and building of new AI models. The initiative will support the company’s objective of fast track the adoption of AI by its customers.

Contract with The Ohio State University: In another recent update, the company notified that it has signed a 5-year contract with The Ohio State University Wexler Medical Center. As a part of the contract, Visage 7 will be implemented across all radiology departments at the center. The center employs around 30k staff and 1.7k physicians. Implementation of Visage 7 is expected to begin in Q2FY20, with completion expected in mid-2020.

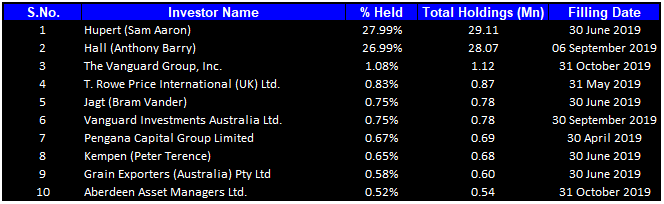

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 60.81% of the total shareholding. Hupert (Sam Aaron) held the maximum number of shares with a percentage holding of 27.99%, followed by Hall (Anthony Barry) with a holding of 26.99%.

Top Ten Shareholders (Source: Thomson Reuters)

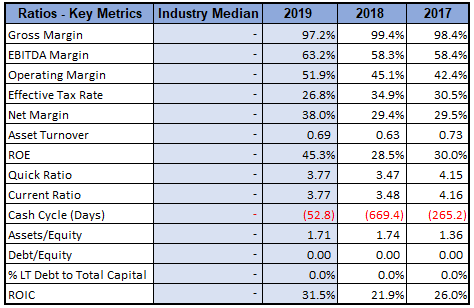

Key Metrics: EBITDA margin for the year ended 30 June 2019 stood at 63.2%, which is higher than the EBITDA margin of 58.3% in the prior corresponding year. Net margin for the year stood at 38.0%, better than prior corresponding year’s net margin of 29.4%. Current ratio for the period stood at 3.77x, up from FY18 current ratio of 3.48x, demonstrating improved short-term financial liquidity. Moreover, the company reported another debt free year, representing the financial stability of the business.

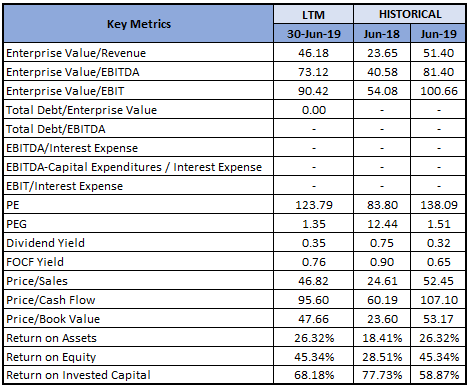

Key Metrics (Source: Thomson Reuters)

Outlook: Year 2020 is expected to be a period of increased revenues from previously won transaction- based contracts which are scheduled to come on stream in the next financial year. The company is focusing on expanding its Visage 7.0 product to address key market segments such as large Health Systems and Hospitals. Moreover, the company will also see additional revenue coming in from Visage RIS, the new technology RIS platform. Overall, FY20 will demonstrate further improvement in operational results, which may see an impact from certain non-controllable market factors.

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: Price to Earnings Multiple Approach(27).png)

PE Based Valuation (Source: Thomson Reuters)

Stock Recommendation: The stock of the company generated negative returns of 31.76% over a period of 3 months. Currently, the stock is trading below the average of its 52 weeks’ trading range of $9.824 - $38.390. FY19 proved to be another year of record performance, with a healthy increase across all key metrics. The company continued to be cash flow positive with retained cash earnings increasing by 28%, after payment of dividends, that increased by 75%. FY20 is expected to be another strong year, with the majority of growth occurring in the second half. Considering the financial performance in FY19, anticipated benefits from major contracts signed during the period, continued investment for product development and portfolio expansion, and expected contribution from the North American region, we confide in the company’s ability to deliver sufficient returns to shareholders. Therefore, we have valued the stock using the price-to-earnings multiple relative valuation method and arrived at a target price denoting high single-digit upside in percentage terms. Hence, we give a “Buy” recommendation on the stock at the current market price of $21.830, down 3.705% on 11 December 2019.

PME Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...