Kalkine has a fully transformed New Avatar.

Company Overview: Primero Group Limited (ASX: PGX) is a multi-disciplinary engineering group mainly involved in providing engineering design and construction services to the minerals, energy and infrastructure sectors. The company’s construction team has several years of experience in all aspects of civil, mechanical and structural construction activities. Primero Group Limited provides its services to a diverse client base which includes mid-sized companies as well as international energy and mining corporations. The company was listed on ASX in 2018 and it intends to grow its existing business and deliver on the record level of contracted work in its current order book..png)

PGX Details

.PNG)

Strong Track Record of Financial Performance: Primero Group Limited (ASX: PGX) is a multi-disciplinary engineering group that provides engineering design and construction services to a diverse client base, ranging from mid-sized companies to international mining and energy houses. As on 5 June 2020, the company had a market capitalisation of ~$43.05 million. The company is focused on growing its existing business and delivering on the record level of contracted work in its current order book.

Over the past few years, the company has witnessed significant improvement in its top line, with revenue rising from $33 million in 2016 to $152 million in 2019. PGX has a three-year compound growth (FY16-19) in underlying EBITDA of +80% pa..png)

Financial Overview (Source: Company Reports)

Amid Covid-19 situation, the company has so far experienced only minor interruptions in its operations and its business growth activities have remained steady with ongoing awards of sustaining capital works, minerals processing feasibility works and Early Contractor Involvement (ECI) engagements. The company’s major project works are currently progressing well, and its business is operating at a run-rate consistent with its FY20 contracted order book guidance. Moving forward, the company expects its contracted order book to grow further, subject to market conditions. The company’s solid cash position and low gearing, places it in a strong position to capitalise on the upcoming future growth opportunities.

FY19 Performance Highlights: For the financial year 2019 or FY19, the company reported revenue from ordinary activities of $151.68 million, up 78% on the previous year. Further, the company reported Statutory net profit after tax of $6.19 million, up 19% on the previous year. The company reported gross operating margin of 13.0%.

The Energy division achieved outstanding growth during the year with revenue of around $76 million, driven strongly by the progressive execution of Primero’s contract with Finnish company Wartsila for the 211MW Barker Inlet Power Station in South Australia, which is being developed for AGL Energy. In FY19, the company successfully completed its IPO and got itself listed on ASX. During the year, the company saw strong execution of several complex and highly technical EPC projects.

The Underlying EBITDA margin of the company stood at 7.7% in FY19, reflecting strong operational contract performance and the company’s ongoing investment in people, systems as well as processes..png)

FY19 Results Snapshot (Source: Company Reports)

H1FY20 Results Highlights: For the first half of FY20 or H1FY20, the company reported total revenue of $112.5 million, up 65% on the previous corresponding period (pcp). The company reported gross operating margin of 7.1% down from 13.8% in H1FY19, impacted by conservative Wartsila contract revenue recognition. The company reported EBITDA of $4.1 million and statutory NPAT of $1.8 million in H1FY20.

The Energy division reported revenue of $71 million in H1FY20, $39 million higher than pcp, driven by the progressive execution of Primero’s contract with Wartsila. During the half-year period, the company announced major contract wins with Rio Tinto Iron Ore and Fortescue Metals Group which strongly validated Primero’s strategy of positioning as a contractor of choice for the Pilbara-based iron ore majors.

At the end of the half-year period, the company’s cash balance stood at $0.2 million with current and non-current debt totaling $6.1 million of which $3.1 million relates to the new accounting lease standard. .png)

H1FY20 Performance Results (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 64.8% of the total shareholding. Henry (Cameron David) and Perennial Value Management Ltd. hold maximum interest in the company at 13.86% and 14.72%, respectively.

.png)

Top 10 Shareholders (Source: Refinitiv, Thomson Reuters)

A Quick Look at Key Ratios: For H1FY20, the company’s asset turnover ratio stood at 1.35x, higher than the industry median of 0.34x. Currently. the company’s ROE is 4.5%, higher than the industry median of 4.1%. The company’s current ratio stands at 1.87x, higher than the industry median of 1.13x, demonstrating that the company is well equipped to pay its short-term obligations. .png)

Key Metrics (Source: Refinitiv, Thomson Reuters)

Substantial New Contract Awards: On 3rd February 2020, the company announced new contract awards totaling approximately $100 million. The company has been awarded the EPC contract for the Christmas Creek Wet High Intensity Magnetic Separation (WHIMS) project by Fortescue Metals Group and it has also secured a significant contract with Rio Tinto Iron Ore (RTIO) for the construction of the Mesa K Non-Process Infrastructure (NPI) facilities. Later, the company was awarded variations extending currently awarded contracts at both Koodaideri and Mesa K for a combined value of approximately $20 million. The award of these contracts has further strengthened the company’s already strong order book and demonstrates the strength of its business model and strategic direction.

Wartsila Contract Update: The company is targeting the commercial close-out of the Barker Inlet Power Station contract with Wartsila Australia as soon as possible and it has escalated the dispute via the South Australian Security of Payment Act (SOPA) provisions, which has resulted in a recent adjudication that awarded Primero the sum of approximately $16.9 million. More applications are currently being finalised by the company to present under SOPA for the larger portion of outstanding monies. PGX has also commenced proceedings in Western Australia’ Supreme Court.

Covid-19 Update: In response to Covid-19, the company has implemented several health and safety measures to protect its people and operations. The company is working closely with its clients in satisfying all testing protocols and it is safely mobilizing large numbers of teams to remote sites within Western Australia. As per the recent update, till now the company has experienced only minor interruptions, which is noteworthy within the general COVID-19 operating environment. The company has commenced the initial return-to-work procedures for its Osborne Park and Bibra Lake offices.

What to expect: The company’s major project works are currently progressing well, and all its business growth activities are also steady with ongoing awards of sustaining capital works, minerals processing feasibility works and Early Contractor Involvement (ECI) engagements. The company continues to target the financing of these substantial contract works through progressive unwinding of its current elevated working capital position and potentially additional debt facilities. Further, it continues to operate at a run-rate that is in line with its FY20 contracted order book guidance of around $195 million. Under the current conditions, the company’s FY21 contracted order book is around $200 million. In addition, the company has further potential to grow FY21 and FY22 contracted orders over the coming months..png)

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

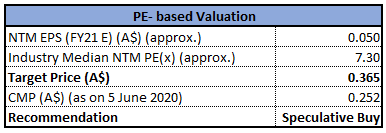

Valuation Methodology: P/E Multiple Based Relative Valuation (Illustrative)

P/E Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months,

Stock Recommendation: The company currently retains strong liquidity and a very low level of gearing, placing it well to capitalise on future growth opportunities. Over the past six months, the stock of PGX has declined by 32.43% on ASX and is trading lower than the average of its 52-week trading range of $0.1 - $0.46, offering investors a decent opportunity for accumulation. We have valued the stock by using a Price-to-Earnings multiple based illustrative relative valuation method and arrived at a target price of double-digit upside (in % terms). For the purpose, we have taken peers like Acrow Formwork and Construction Services Ltd (ASX: ACF), SRG Global Ltd (ASX: SRG) and Austin Engineering Ltd (ASX: ANG). Considering the company’s solid cash position, low gearing, resilient performance amid Covid-19, strong contracted order book, and current trading levels, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.252, up by 0.8% on 5 June 2020.

.png)

PGX Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...