Company Overview: Primero Group Limited (ASX: PGX) provides engineering design, construction and operational services to the minerals, energy and infrastructure sectors. The company has expertise in project implementation and provides services to a diverse set of clients, ranging from mid-sized companies to international mining and energy houses. Primero Group contracts range from straight design, straight construction and design and construction in all three sectors.

.png)

PGX Details

Several Contract Wins and Strong Growth in Revenue: Primero Group Limited (ASX: PGX) is an engineering contracting company, which provides engineering design and construction services to the minerals, energy and infrastructure sectors. As on 6 March 2020, the market capitalisation of the company stood at ~$40.47 million. During FY19, the company delivered healthy and sustainable growth and reported a record of delivery and excellence. The company reported outstanding financial delivery with an increase of 78% in revenue to $152 million, up from $85 million in FY18. The composition of FY19 service revenue by key business segments was approximately 50% from Energy, 27% from Non-Process Infrastructure (NPI) and 23% from Minerals. In the same time span, EBITDA of $11.7 million was in line with the guidance and represented an increase of 30% on FY18. This brings EBITDA margin to 7.7% and reflects strong operational contract performance coupled with continued investment in people, systems and processes. Over the span of three years, the company witnessed a compound growth of over 80% p.a. in underlying EBITDA. During FY19, the company broadened its client base and increased its number of clients to 53 from 39 in FY18. The company also retained an extremely strong balance sheet with significant growth funding flexibility and cash position of $21.9 million and a low gearing with net debt of $3 million. In the same time span, the company won several significant contract awards across various sectors and remains active and competitive for upcoming new contract opportunities over the coming months. Over the span of 4 years from FY15 to FY19, the company witnessed a CAGR of 43.6% in revenue and a CAGR of 34.06% in gross profit.

PGX has also released its interim results for the period ended 31 December 2019 which represented another definite period of revenue growth and contract delivery from PGX businesses. The unwavering focus of the company on risk-weighted returns and strong execution of several complex and highly technical EPC projects will enhance the company’s potential and capacity to deliver more substantial and higher margin projects. Primero Group Limited is targeting to finance the considerable contract works via progressive unwinding of its current elevated working capital position and via additional debt facilities.

The company remains well placed to capitalise on the strong pipeline of available growth opportunities. The recent contract wins of Rio Tinto Iron Ore and Fortescue Metals Group, have strongly validated the company’s strategy of positioning as a contractor of choice for the Pilbara-based iron ore majors. The company’s focus on technical excellence and being a partner of choice remains the core of PGX business model. The market remains active and competitive, and hence the company expects large volumes of contract opportunities in the coming months. The tendering activities in the iron ore market in Western Australia is likely to generate considerable Non-Process Infrastructure (NPI) opportunities..png)

Growth in Revenue and EBITDA (Source: Company Reports)

Details of Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of Primero Group Limited. Henry (Cameron David) Ltd is the largest shareholder in the company, with a percentage holding of 13.79%. .png)

Top 10 Shareholders (Source: Thomson Reuters)

Sufficient Liquidity Levels and Stable Balance Sheet: During 1H20, gross margin of the company stood at 7.1%, and EBITDA margin of the company was 3%. In the same time span, net margin of the company was 1.6% as compared to the industry median of 3.1%. Return on Equity of the company was in line with the industry median and stood at 4.5%. During 1H20, current ratio of the company stood at 1.87x, higher than the industry median of 1.12x. This indicates that the company is liquid enough to pay off its current liabilities using its current assets. In the same time span, Assets/Equity ratio of the company was 2.14x, lower than the industry median of 4.90x and Debt/Equity ratio stood at 0.13x as compared to the industry median of 0.59x. This indicates that the business is financed with a significant proportion of investor funding and a small amount of debt, resulting in a financially stable balance sheet. .png)

Key Margins (Source: Thomson Reuters)

Update on Wartsila Contract: The company has announced that it has completed the contracted workstreams with Wartsila Australia on AGL Energy’s major Barker Inlet Power Station, marking a considerable achievement for the company. PGX has delivered over 1.3 million manhours of work on a Lost Time Injury (LTI) free basis and is continuing to target the conclusion of the process as soon as possible in order to bring the assessment to a conclusion. The company has recognised all residual revenue and costs associated with the project in 1H FY20.

Low Gearing and Significant Increase in Revenue: The company has recently released its results for the half year ended 31 December 2019, wherein it reported an increase of 65% in revenue to $112.5 million. Approximately $70 million of this revenue was attributable to the Wartsila contract. In the same time span, gross operating margin of the company stood at 7.1%, which was significantly impacted by the conservative approach adopted with respect to Wartsila contract revenue recognition during the period. The company also reported a very low gearing with current and non-current debt totaling to $6.1 million. In the same time span, EBITDA of the company stood at $3.6 million and statutory NPAT came in at $1.8 million. The company remains focused on growing its existing business and on delivering a record level of contracted works in its current order book.

Performance of Business Segments: The company derives its revenue from Energy, Non-Process Infrastructure and Minerals sectors. During 1H20, the energy segment contributed approximately 63% in revenue, followed by Non-Process Infrastructure (NPI) revenue of 19% and 18% from Minerals. PGX’s energy division has a successful track record of servicing its clients which operate onshore and offshore gas facilities. The energy division achieved revenue of approximately $71 million in 1H20, up from $32 million in 1H19. This was driven by progressive execution of the company’s contract with Wartsila. In the same time span, revenue from NPI totalled to approximately $21 million, driven predominately by the execution of significant design and construction work on several projects for Pilbara-based iron ore majors. The mineral division of the company offers services from the early stage geochemical assessment of orebodies through to the expansion or optimisation of established operations. During 1H20, the company generated revenues of approximately $20 million from the minerals segment..png)

Revenue by Segment (Source: Company Reports)

Future Expectations and Growth Opportunities: Based on current business conditions and opportunities across the three key divisions of the company, PGX remains positive about the outlook for the coming years. The company expects an increased proportion of revenue from the minerals division and yield higher margins relative to NPI and Energy businesses. The stable cash position of the company along with low gearing and funding liquidity places PGX in a good position to capitalise on future opportunities.

The recent significant wins of the company - Rio Tinto Iron Ore and Fortescue Metals Group have strongly validated the company’s strategy as a contractor of choice for the Pilbara-based iron ore majors. The contracted orders for FY20 stand approximately $120 million, and the current record book of the company is at record levels. PGX continues to target the financing of these contracts via progressive unwinding of working capital position and additional debt facilities. The company expects 2H20 contracted orders to grow and deliver an underlying EBITDA margin of approximately 6-8%. PGX will continue to expand its Early Contractor Involvement (ECI) model and will broaden its potential to access potential project opportunities..png)

Key Valuation Metrics (Source: Thomson Reuters)

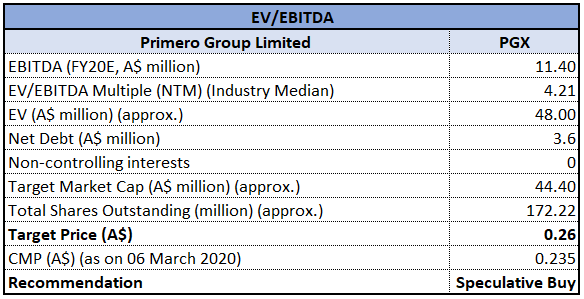

Valuation Methodology: EV/EBITDA Multiple Approach

EV/EBITDA Multiple Based Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of PGX is trading close to its 52-weeks’ low level of $0.215, proffering a decent opportunity for accumulation. The company is pursuing further panel positions for major sustaining capital group work and strengthening itself to capture major sector spends within Australia. PGX is enhancing the commodity suite for full life-cycle project services delivery and is expanding the global project footprint in key areas of specialisation. The company has a sustained culture of safety and excellence and has diversified across key sectors, with further expansion in existing and new geographies. Considering the trading levels, lower Assets/Equity ratio, decent financial performance, and significant growth opportunities, we have valued the stock using EV/EBITDA based relative valuation approach and have arrived at a target price offering an upside of higher single-digit (in percentage terms). Hence, we recommend a “Speculative Buy” rating on the stock at a current market price of $0.235 on 6 March 2020.

PGX Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...