Kalkine has a fully transformed New Avatar.

Company Overview: Primero Group Limited is an Australia-based multi-disciplinary engineering company. The Company provides a range of engineering services including design, fabrication, procurement, installation, testing and commissioning. Its services also include consultancy, fit for purpose design, construction, operation, maintenance and asset management of project plants. The Company provides its end-to-end engineering services to minerals, energy and infrastructure industries.

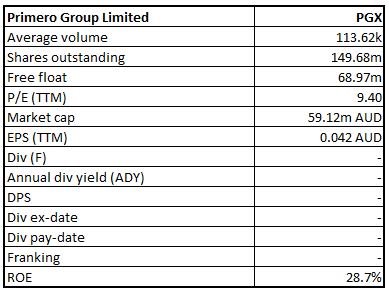

PGX Details

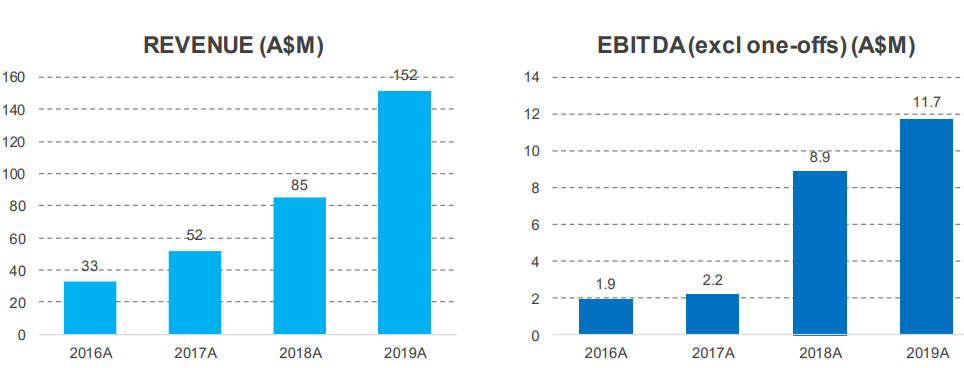

Decent Track Record for Earnings Growth: Primero Group Limited (ASX: PGX) is an engineering contracting company, specialised in providing engineering design and construction services to the minerals, energy and infrastructure sectors. As on 15 November 2019, market capitalisation of the company stood at approximately $59.12 million. The company exhibited a decent track record for earnings growth in the past supported through several projects and growth in revenue over the same period. Looking at the historical performance, top-line CAGR growth over the period of FY16 - FY19 was at ~66.4% with FY16 and FY19 revenue amounting to $32.939 million and $151.7 million, respectively. It reflects that PGX is possessing respectable capabilities to garner revenues. Over the same period, EBITDA (excluding one-off costs) went up from $1.9 million to $11.7 million and witnessed a CAGR of 83.3%. This indicates the efficiency of company and implies that it is capable of managing its costs well. Net profit for FY16 and FY19 was reported at $0.955 million and $6.189 million, representing a 5-year CAGR growth of around 86.4%.

Recently, the company announced that it has been awarded an EPC contract by Kalium Lakes for design, procurement and construction of Beyondie SOP Project gas inlet and delivery stations. The new contract awards, along with existing contract extensions and general client repeat works, have increased PGX’s contracted order book for FY20 to approximately A$120 million.

The company released its results for the year ended 30 June 2019, wherein it experienced remarkable growth with revenue increasing by 78% from $85.2 million in FY18 to $151.7 million in FY19. During the year, EBITDA (excluding one-off costs) of the company was also up by 30% from $9 million in FY18 to $11.7 million in FY19. It removes the impact of issue of limited-recourse employee share loans for listing, initial public offering costs, due diligence costs and bad debts.

During the year, gross operating margin was 13.0% and EBITDA (earnings before interest, taxes, depreciation and amortisation) margin stood at 7.7%, representing a decent operational contract performance along with continued investment in people, systems and processes in order to improve the company’s platform for positive and sustainable growth. Primero Group Limited also witnessed a rise of 19% in statutory net profit after tax from $5.2 million in FY18 to $6.2 million in FY19. The company retained a strong balance sheet with excellent liquidity and significant growth funding flexibility. It was stated that significant milestone payments have been anticipated to be received in the next few months with regards to Wartsila Barker Inlet Power Station contract and the Clough South Flank project work. Annual General Meeting of Primero Group Limited for the year is to be held on 25 November 2019.

Moving forward, low gearing, funding liquidity, along with a robust cash position, are expected to act as tailwinds for long-term growth and might help the company in gaining traction among the market participants.

Financial Performance (Source: Company Reports)

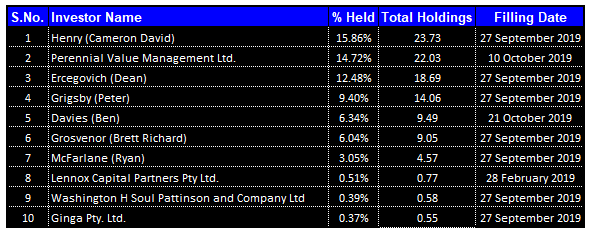

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Primero Group Limited:

Top 10 Shareholders (Source: Thomson Reuters)

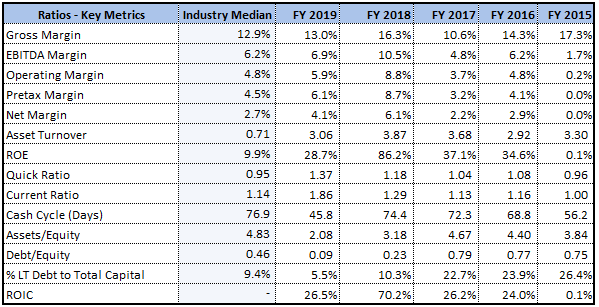

Improvement in Key Margins: EBITDA margin of the company stands at 6.9%, as compared to the industry median of 6.2%. The company’s net margin stood at 4.1% at the end of June 2019, which is higher than the industry median of 2.7% and, therefore, it can be said that PGX has decent capabilities to convert its top-line into the bottom-line. The company’s ROE (Return on Equity) stood at 28.7% at the end of June 2019 as compared to the industry median of 9.9% and, therefore, it can be said that Primero Group Limited has managed to deliver decent returns to its shareholders, which might attract the attention of market participants.

During the year, current ratio stood at 1.86x in comparison to the industry median of 1.14x, implying that the company is in a better position to address its short-term obligations when compared to the broader industry. The company’s Debt/Equity ratio stood at 0.09x at the end of June 2019, which is lower than the industry median of 0.46x and, thus, it looks like the company’s balance sheet is less leveraged as compared to the broader industry.

Key Metrics (Source: Thomson Reuters)

Update on Barker Inlet Power Station Progress: AGL Energy’s Barker Inlet Power Station (or BIPS), situated in Adelaide, South Australia happens to be Primero’s current flagship energy project as the sub-contractor to EPC Contractor Wärtsilä which has just completed 1,000,000 manhours on site. This has been done without Lost Time Injury (or LTI). It was further added that there has also been just one (1) Medically Treated Injury (or MTI) throughout the entire period. The project is nearing completion with successful milestones reached for start-up of 9 of the 12 x 18MW engines that will fire the 211MW peaking load power station.

Appointment of Administrators to Alita: Primero Group Limited announced the appointment of administrators to Alita Resources Limited and noted that it had unpaid accrued work-in-progress and receivables of approximately $325,000 specific to Alita contract at June 30, 2019.

The company also noted that its maximum potential exposure in FY20 with respect to the Alita contract is estimated to be less than $500,000 and thus, plans to work constructively with the administrators of Alita towards a targeted restructure of Alita business. The company was also awarded with the major contract for pre-assembly of BHP’s south flank balance machines for Thyssen Krupp Industrial. Thyssen Krupp was awarded supply and installation of Balance Machines by BHP in the month of November 2018.

Position of Cash Flows: During the year ended 30 June 2019, the working capital build in the business, which is directly attributable to the large year-on-year increase in service revenue, resulted net operating cash flow to fall from $4.7 million in FY18 to $3.1 million in FY19. The purchase of two cranes for the construction of the Barker Inlet Power Station resulted net investing cash outflow to go up to $1.8 million in FY19 from $1.4 million in FY18. The company also received gross new equity funds of $20 million through Primero’s IPO and ASX listing, resulting in net financing cashflow of $20.1 million, up from the cash outflow which amounted to $2.6 million in FY18.

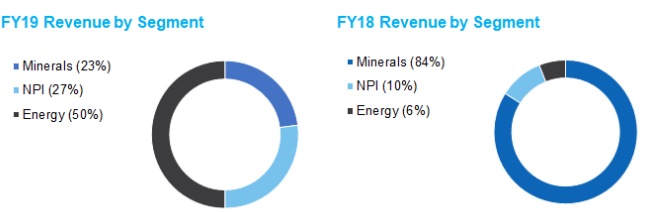

Composition of Revenue: The composition of FY19 service revenue by key business segment was circa (1) 50% Energy, (2) 27% Non-Process Infrastructure (or NPI), and (3) 23% Minerals. The Energy division reported an outstanding growth during the year, with revenue of approximately $76 million, mainly driven by the progressive execution of the company’s contract with Wartsila for the 211MW Barker Inlet Power Station in South Australia. The execution of major design and construct work on a number of projects for Pilbara-based iron ore majors helped the revenue from the NPI business which amounted to approximately to $41 million for FY19.During the year, revenue from the Minerals division, which was earned across a wide range of major mining projects, geographies, commodities and underlying workstreams in FY19, totalled approximately to $34 million.

Composition of Revenue (Source: Company Reports)

What to Expect: Primero Group Limited remains optimistic about the outlook for FY20 based on existing business conditions and tendering opportunities across its three key divisions. The company anticipates a significant volume of new contract opportunities over coming months as market remains active and competitive. The company expects that current contracted revenue for FY20 to be approximately $90 million, similar to the levels of FY19. It was added that increased proportion of total FY20 revenue has been anticipated to be comprised from Minerals division, that typically yields higher margins to those from NPI as well as Energy businesses.

The company also continues to grow the Early Contractor Involvement (or ECI) model and broaden the potential access to the multi-year O&M and BOO project opportunities. The company’s decent cash position, low gearing and funding liquidity place the company in an excellent position to capitalise on the available future growth opportunities. The company also continues to deploy towards the capacity to deliver larger, and targeted higher margin projects.

Given the magnitude of capital programs undertaken by the Pilbara majors, tendering activity in the iron ore market of Western Australia is generating considerable NPI opportunities. This is combined with strong activity in the Minerals and Energy sectors. The recent monthly revenues of $17 million demonstrate a capacity to deliver. Primero Group Limited is also building committed work for FY21.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: Price to Earnings based Valuation

.png)

Price to Earnings based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM: Next Twelve Months

Stock Recommendation: As per the ASX, the stock of the company gave a return of 5.33% in the past 6 months and 1.28% in last one month. Currently, the stock is trading below the average of its 52-week trading range of $0.345 - $0.480, proffering a decent opportunity for accumulation. The cash position of the group remains robust and stands at $21.9 million with a low gearing of $3 million debt. Considering the growing battery mineral sector, strong project pipeline with recent contract wins, geographic expansion, soaring revenue growth, high RoE and decent outlook, we have valued the stock using a relative valuation method, i.e., P/E multiple and arrived at a target price of double-digit growth (in percentage term). Hence, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.395 on 15 November 2019.

PGX Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...