Company Overview: Premier Investments Limited is an Australia-based company, which operates a range of specialty retail fashion chains within the specialty retail fashion markets in Australia, New Zealand, Singapore, the United Kingdom, as well as Malaysia and Hong Kong. The Company also has investments in listed securities and money market deposits. The Company operates in two business segments: investments and retail. The Company's retail segment includes a range of specialty retail fashion chains. The Company's investments segment represents investments in securities for both long and short-term gains, dividend income and interest. The Company offers brands, including Smiggle, Peter Alexander, Just Jeans, Jay Jays, Portmans, Jacqui E and Dotti. The Company also offers brands, which include Breville, Kambrook and Sage by Heston Blumenthal. The Company's subsidiaries include Kimtara Investments Pty Ltd, Premfin Pty Ltd, Springdeep Investments Pty Ltd and Prempref Pty Ltd.

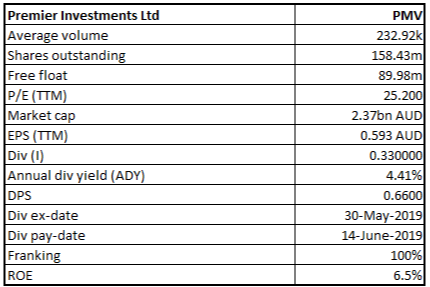

PMV Details

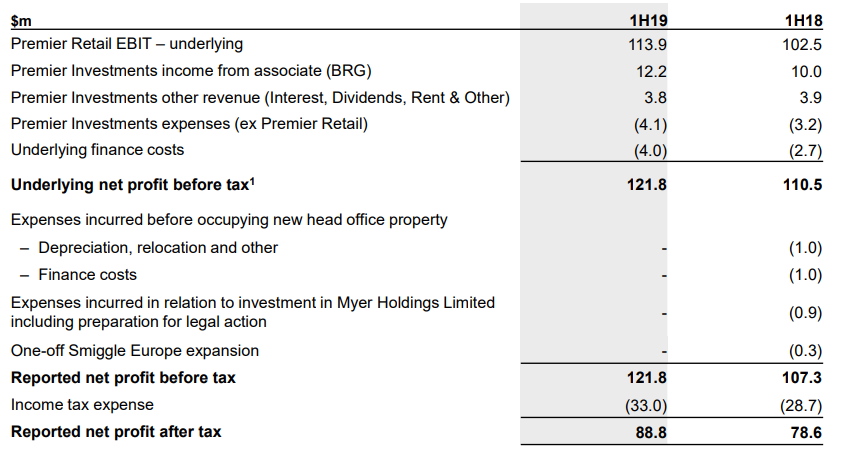

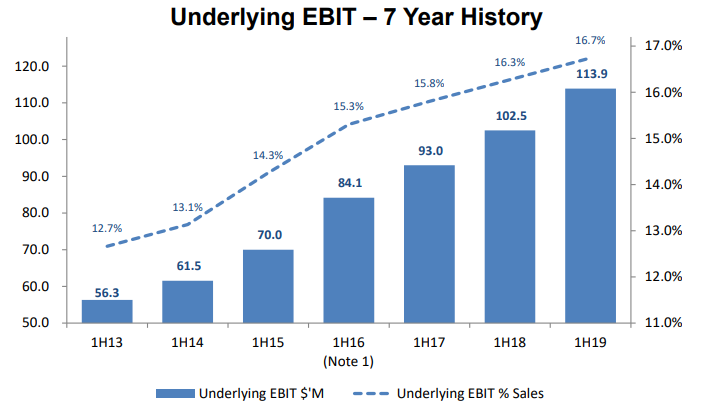

Increase in NPAT and Interim Ordinary Dividend: Premier Investments Limited (ASX: PMV) is engaged in the business of operating numerous specialty retail fashion chains within specialty retail fashion markets in Australia, New Zealand, Asia, and Europe. As on August 26, 2019, the market capitalisation of Premier Investments Limited stood at ~$2.37 billion. PMV declared the results for the six months ended January 26, 2019 in which it delivered net profit after tax (or NPAT) amounting to $88.8 million, which reflects an increase of 13.0%. The company’s Chairman named Mr. Solomon Lew reflected favourable views with respect to the results and stated that the sales witnessed a rise of 8.0% and stood at $680.2 million and its EBIT amounted to $113.9 million (which was up 11.1% as compared to 1H FY18 underlying EBIT). The company’s outstanding performance for the period was driven by solid growth in all the apparel brands, record sales throughout the online divisions, record Smiggle global sales and record Peter Alexander sales. As a result of the strong performance in 1H FY19, the company declared an interim ordinary dividend amounting to 33 cps (fully franked), which reflects an increase of 13.8% or 4 cps as compared to 1H FY18. The company’s balance sheet includes equity accounted value amounting to $238.9 million for the holdings in Breville Group Limited. The market value of investment was $602.6 million, considering the share price of $16.51 as on March 20, 2019. The company stated that the Australian and New Zealand retail environment was competitive during 1H FY19. However, Premier Retail’s Apparel Brands were focused towards key strategies and delivered exceptional results for 1H, and its total Apparel Brand sales rose by 7.5%.

In our view, the company has a potential to grow further at the back of (1) decent cash position, (2) improving RoE over the last few years, (3) strong business strategy to focus on growth and cost optimization, and (4) holds rich customer base. There are expectations that decent capabilities to generate cash and revenues, favourable fundamentals, and respectable liquidity levels might act as tailwinds moving forward.

Summarised Consolidated Income Statement (Source: Company Reports)

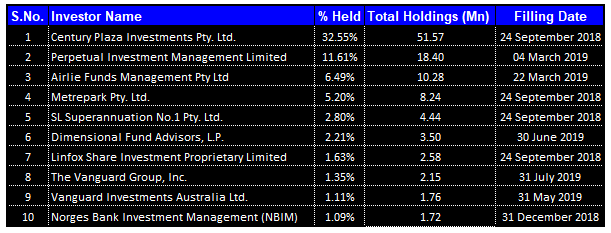

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Premier Investments Limited:

Top 10 Shareholders (Source: Thomson Reuters)

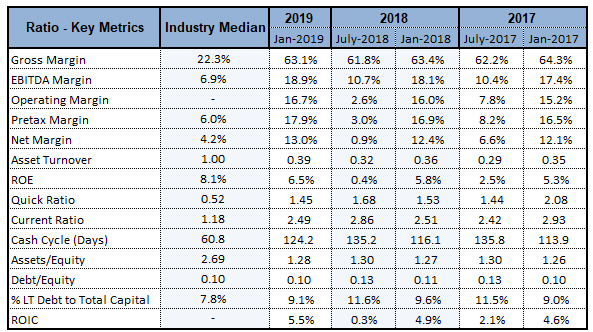

Key Margins Higher Than Industry Median: The key margins of Premier Investments Limited are higher than the industry median as its net margin stood at 13% in 1H FY19 as compared to the industry median of 4.2% and, thus, it looks like that the company has improved its capabilities to convert its top-line into the bottom-line. Also, the company’s EBITDA margin stood at 18.9%, which is comfortably higher than the industry median figure of 6.9%.

Key Ratios (Source: Thomson Reuters)

The company’s current ratio stood at 2.49x while the industry median is 1.18x and, therefore, it can be said that PMV is well-placed to meet the short-term obligations as compared to the broader industry. Also, it looks like that the decent liquidity levels place the company well to make deployments towards the strategic growth prospects. It can be said that the decent liquidity levels along with net margin position, might help PMV to post decent growth momentum moving forward. PMV’s Debt/Equity ratio stood at 0.10x which reflects a fall of 6.3% on a YoY basis and, therefore, it can be said that the company has been focusing towards deleveraging its balance sheet. Generally, a deleveraged balance sheet reflects stability and helps the company in meeting long-term growth objectives.

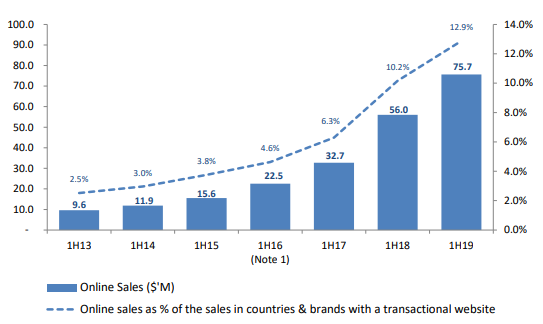

A Quick Overview of PMV’s Growth Initiatives: In the release, it was stated that Premier Retail grew online sales for 1H FY19 by 35.2% and stood at $75.7 million. The online business contributed 12.9% of the sales in countries and brands with a transactional website as compared to 10.2% in 1H FY18. Premier Retail would be launching New Zealand transactional websites for Just Jeans, Smiggle, Portmans and Jacqui E in 2H FY19. These will be in addition to already offered and rapidly growing New Zealand Peter Alexander and Dotti transactional websites.

Premier Retail 1H FY19 EBIT (Source: Company Reports)

With respect to Smiggle, it was added that brand witnessed record global sales for 1H FY19 which amounted to $178.8 million, which include stand out performance from Asian market which encountered sales growth of 34.8% on 1H FY18. In the month of September 2018, Smiggle made an announcement about the plan to accelerate the global growth from 4 major pathways, which were: (1) Global wholesale arrangements in the markets where Smiggle has significant opportunity, but it elects not to or would unlikely operate the company-owned standalone stores, (2) Online growth, both proprietary and third party, (3) Concession partnerships with iconic global retailers, and (4) New store growth via continued rollout of the standalone stores where economics and shareholder returns are attractive.

Decrease in CODB in 1H FY19: The company stated that its Cost of Doing Business (or CODB) witnessed a fall of 68 basis points as a percentage of sales and stood at 46.3%. The company continued to control the costs even though there was structural inflationary pressure. It was also added that deployment would continue towards growth initiatives which include Online, Smiggle International and Peter Alexander. Over the past twelve months, Premier Retail closed 16 stores, which take total closed over the past 6 years to 101 stores, and this happens to be a part of an ongoing program to close the unprofitable stores.

Decent Growth Witnessed in Top-Line: From the analysis standpoint, the company looks decent as its top-line has witnessed a CAGR growth of 7.06% between the time frame of FY14- FY18 and, thus, it can be said that PMV is possessing decent capabilities to generate revenues. Coming to the balance sheet, it can be said that the company’s cash and short-term investments are standing at decent levels. At end of 1H FY19, the company’s balance sheet consisted free cash on hand of $183.2 million, its investment in Myer Holdings Limited which was valued at $34.9 million (and its market value was $50.4 million based on the share price of $0.57 as on March 20, 2019) plus its equity accounted investment in Breville at $238.9 million (which was having a market value of $602.6 million based on the share price of $16.51 on March 20, 2019).

The company’s cash receipts have witnessed a CAGR growth of 7.24% in the time frame FY14- FY18 which can be considered a respectable level and, thus, it looks like that PMV is possessing capabilities to generate cash which could help it over the long-term. There are expectations that its capabilities to generate revenues and cash might help in achieving overall growth.

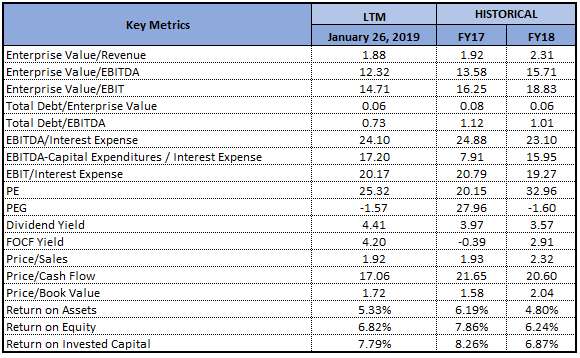

Key Valuation Metrics (Source: Thomson Reuters)

What to Expect from PMV moving Forward: Premier Retail has been deploying towards new stores, upgrades and refurbishments in order to deliver the sustainable sales growth. It was also added that, in 1H FY19, 89% of the capital investment in Australia and New Zealand stores financed through the landlord contributions. The following picture provides a broader overview of online sales growth:

Online Sales Growth (Source: Company Reports)

The company stated that online channel has been delivering significantly higher EBIT margin as compared to the group average and all the global sites have been delivering robust growth with all the brands outperforming the market. The Board of Premier Investments Limited would continue to review the capital management, which could help in delivering decent returns to the shareholders and can help the company in gaining traction among the market players. Additionally, the Apparel Brands’ LFL (or like for like) performance happens to be stronger than total sales result as Premier Retail have and would continue to close the unprofitable stores because of the unrealistic landlord rents.

Valuation Methodology: EV/EBITDA Multiple Approach (NTM)

EV/EBITDA Multiple Approach (NTM) (Source: Company Reports), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The company’s stock has fallen 8% in the span of the previous one month while, in the time frame of the previous three months, it has fallen 12.93%. Currently, the stock is trading towards the 52-week lower levels of $13.61 with PE multiple of 25.20x, proffering a decent opportunity for accumulation. Premier Retail’s Dotti and Smiggle stores on Chapel Street would close down in calendar 2019. Additionally, Just Jeans earlier made an announcement about the closure of flagship store in Rundle Mall (South Australia) in the 2H FY19, which reflects willingness of Premier Retail to walk away from the stores which are having unrealistic rents that deliver the unprofitable sales.

There are expectations that the company’s capabilities to generate revenues and cash might support the overall growth of PMV moving forward. It was added that Peter Alexander’s strategic 2020 Growth Plan, which focuses on delivering in excess of $250 million in annual sales by FY 2020 happens to be well ahead of the plan. The brand opened 26 new stores over the past 18 months and is well ahead of the planned 40 new store openings between the time frame of FY18 and FY20. Additionally, Peter Alexander confirmed 4 new stores to open in the 2H FY19. Based on the foregoing, we have valued the stock using a relative valuation method, EV/EBITDA multiple and have arrived at the target price about low double-digit growth (in percentage term). Hence, considering the above-stated facts and current trading levels, we give a “Buy” recommendation on the stock at the current market price of A$14.800 per share.

PMV Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...