Company Overview: Praemium Limited is a provider of investment platforms, investment management, portfolio administration, client relationship management (CRM) solutions and financial planning tools to the wealth management industry with offices in Australia, the United Kingdom, Jersey, Armenia and Hong Kong. The Company's segments are Australia, the United Kingdom and Asia. Its investment platform is based on Separately Managed Accounts (SMA) technology. An SMA allows wealth managers to implement investment strategy changes across a number of client accounts and is available in both retail super (SuperSMA) and non-super. It provides Smart Investment Management (Smart), which is an in-house investment management solution. Its WealthCraft gives financial professionals the tools and services to develop and expand their wealth management business. Its V-Wrap system provides reporting solutions across a range of reports and for any date or range of dates.

.png)

PPS Details

Strong Inflows, Improving Equity Markets Supported PPS’s Platform AUM: Praemium Limited (ASX: PPS) is a small-cap fintech services provider with the market capitilsation of circa $184.4 Mn as of 7 May 2019. Recently, the company released its Q3FY19 results wherein it witnessed combined quarterly gross platform inflows of $744 million while the company’s UK/International gross platform inflows stood at $234 million (or £127 million). The platform FUA (Funds Under Administration) witnessed a rise of 13% over the quarter and stood at $8.9 billion because of the robust inflows and improvement in the equity markets. The company witnessed a CAGR growth of 23.68% in its top-line in the span of five years (FY 2014-FY 2018). The company possesses strong revenue-generating capabilities which is evident from the growth rates which has been witnessing over the past few years. Recently, the company announced it has lost its contract with ANZ Private, worth $4 million or 8% of total group revenue for the calendar year 2018. However, it is disappointing that a valued client chose to go in the different direction, while the numerous major new agreements which have been executed might be having a positive and material impact. Besides this, the company’s management stated that the financial advisers have expanded investment universe of 1,300 domestic and international model portfolios and single investment assets which allows them to broaden their usage of the platform. This new capability significantly increases the addressable reach in the Australian Platform market. Moreover, the quality of new Adviser Portal along with the Investor Portal has witnessed favourable responses from the existing and prospective clients. The company expects that it will continue to attract considerable new business on the back of its broadened offering, which in turn will add to the positive business momentum.

.png)

Platform Gross Inflows and FUA (Source: Company Reports)

Top 10 Shareholders: Following table gives the broader picture of top 10 shareholders of Praemium Limited:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Release of Integrated Managed Accounts Platform: The fully integrated managed account platform provides advisers and wealth managers with the ability to construct the full breadth of managed accounts solutions for their clients through seamless digital platform experience. The upgrade and enhanced feature set address the needs of the platform market. The primary components of upgrade consisted a fully integrated managed accounts digital experience for the advisers and their clients which includes Separately Managed Accounts (or SMA) as well as Individually Managed Accounts (or IMA) under custody, non-custodial Virtual Managed Accounts to underpin MDAs, IDPS and similar structures, and Unified Managed Accounts which enable the consolidated view of custody and non-custody investment assets. During the quarter, the group witnessed a highly positive response with respect to the global rebrand and marketing campaign for Praemium’s Integrated Managed Accounts platform. Moreover, major expansion of the available platform custodial assets with addition of ASX 300 & MSCI 200 equities along with the broad range of managed funds, hybrid, XTBs as well as local and international ETFs and the launch of intuitive Adviser Portal and dashboard with individual adviser customisation were also some of the key developments during the quarter.

Decent Standing of Margins, Significant Improvement in CFO: Praemium Limited’s key margins’ position has witnessed an improvement in FY 2018 on the YoY basis which reflects an improvement in its financials. Its net margin in FY 2018 stood at 3.4% which implies a YoY rise of 1.4% reflecting the company’s improved capability to convert its top line into bottom line. However, in 1H FY 2019, its net margin was 2.9%. During the same period, its EBITDA margin was 13.7% which is higher than the industry median of 13.3%.

.png)

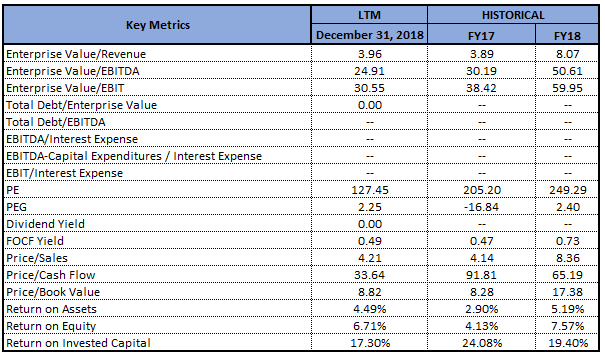

Key Metrics (Source: Thomson Reuters)

In the span of previous five years, the company’s cash from operating activities (CFO) have demonstrated a significant improvement which is evident from its CAGR growth of 104.39% (FY 2014-FY 2018) which was primarily due to strong growth momentum witnessed in its cash receipts. The company’s current ratio stood at 1.69x which is marginally higher than the industry median of 1.66x reflecting the company’s better footing to address its short-term obligations.

Contract Extension with Shaw and Partners: Praemium had made an announcement that it had signed the major contract extension with Shaw and Partners in order to provide an integrated suite of portfolio administration and investment platform services. Shaw and Partners had also rolled out ‘Shaw Managed Accounts’ solution in the year 2016, using Praemium’s Managed Accounts platform. PPS had stated that Shaw and Partners extended its existing VMA contract for the span of 5 years with an option to further extend for 5 years. Additionally, the relationship of PPS has been expanded and include portfolio administration for more than 2,500 client portfolios, which Shaw and Partners administered and reconciled internally. The expanded agreement has an incremental contract value of around $1 million per annum.

Expansion Of Relationship With Morgan Stanley Wealth Management Australia: Praemium had made an announcement of a major expansion in the relationship with Morgan Stanley Wealth Management Australia. Currently, PPS gives non-custodial reporting for 2,500 investor portfolios with the domestic assets, via VMA reporting solution. Moving forward, a further 2,500 portfolios with international assets will be added to its VMA. Under the expanded agreement, Praemium would be providing portfolio administration and taxation reporting for the portfolios having international investments. Praemium expects that these portfolios have an incremental contract value amounting to around $1 million p.a.

Understanding Praemium’s 1H FY 2019 Results: Praemium posted underlying EBITDA amounting to $5.1 million in 1H FY 2019 which implies a rise of 19% rise on 1H FY 2018. The platform FUA witnessed a rise of 14% and stood at $8.4 billion. The company witnessed a rise of 30% in the clients globally in 2018 calendar year. In 1H FY 2019, Australian business witnessed a positive momentum and its revenue rose by 13% on 1H FY 2018. With respect to Australian business, there were robust inflows to Managed Accounts investment platform which led to a 28% rise in SMA revenue and the portfolio services revenue witnessed the rise of 2% because of growth of institutional clients on Praemium’s VMA.

.png)

Key Metrics for 1H FY 2019 (Source: Company Reports)

The company’s international’s EBITDA loss witnessed the fall of 4% and stood at $1.0 million which comprises UK’s EBITDA loss amounting to $0.6 million and Asia’s EBITDA loss amounting to $0.4 million. The UK business got impacted by the strong declines witnessed in the global equity markets as well as outflows in Smartfund Protected range of managed funds. However, Asia’s EBITDA loss witnessed the fall of 31% and stood at $0.4 million and its revenue rose by 116% as compared to the prior reporting period. This was because of a rise in WealthCraft CRM as well as planning software licences in 2018 which rose 43% internationally from 503 to 718.

What To Expect From PPS Moving Forward: Referring to Hayne Royal Commission report, the management of Praemium had stated that advisers would need to work harder in order to garner revenue because of the higher compliance requirements. Therefore, it would be critical that they use technology in order to find efficiencies elsewhere. The company stated that the UK market had witnessed a steady increase in the usage of professionally-run model portfolios, and PPS has been witnessing an increase in interest in the Managed Accounts platform in the UK as well as in the international markets. Complimented with the expanded capability related to sales and marketing, the company is focussed towards ramping up its growth.

At the end of 1H FY 2019, the company had a robust balance sheet with the net assets amounting to $20.9 million and $11.3 million in cash. The company stated that there are strong cash reserves in order to support investments towards earnings enhancing initiatives which include organic and strategic opportunities and to manage any future foreign currency impacts of the overseas operations.

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

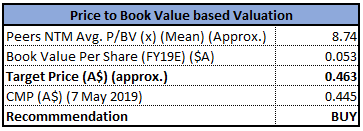

Method 1- Price to Book Value Multiple Approach (NTM):

P/BV Based Valuation (Source: Thomson Reuters)

Method 2- EV/Sales Multiple Approach (NTM):

.png)

EV/Sales Multiple Approach (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: In the last three months, the stock has been down by around 36.36% and is trading close to its low levels, proffering a decent opportunity for accumulation as the business has favourable prospects at the back of decent balance sheet position, prudent investment towards technology, and other positive business developments incurred during the third quarter of 2019. Fundamentally, the company’s RoE (or return on equity) stood at 3.1% which is higher than the industry median of 1.6% reflecting that the company has been delivering better returns to its shareholders. We expect that its stable balance sheet position and increasing RoE might help to gain traction moving forward. On the other hand, PPS had been informed by key Australian institutional client of an investment platform that it has selected an alternative supplier. Given the backdrop of decent fundamentals and long-term growth potential in the business, we have valued the stock using two Relative valuation methods, P/BV, and EV/Sales multiple and arrived at a single digit upside growth (%) in the next 12 -24 months. Based on the foregoing and current trading level, we give a “Speculative Buy” recommendation on the stock at the current price of A$0.445 per share (down 2.198% on 7 May 2019).

PPS Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...