Company Overview - Platinum Investment Management Limited is a holding company. The Company is a fund manager, which specializes in investing in international equities. The Company trades as Platinum Asset Management. The Company’s product range consists of global, regional and sector products for investment, as well as a global listed investment company. The Company Platinum also manages various institutional mandates that invest primarily in global equities. The Company’s fund includes PlatinumTrust Funds, MLC Platinum Global Fund, Platinum Capital Limited and Optima Funds. PlatinumTrust Funds are unit trusts and primarily comprise investments in global, regional or sector, equities. MLC Platinum Global Fund is a unit trust that primarily invests in global equities. Platinum Capital Limited is a primarily comprises investments in global equities. Optima Funds primarily comprise investments in either global or Japanese/Korean equities for the respective Funds.

Analysis - Our focus for today’s report is Platinum Investment Management Limited (PTM), the funds management company, which illustrated a strong balance sheet and few liabilities in FY2014.

PTM’s sales during the year ended June of 2014 were A$319.80 million, an increase of 37.8% as opposed to 2013, wherein the sales were A$232.15 million. Most of the revenue is derived from Australia wherein the sales were A$277.01 million in 2014 (i.e., ~86.6% of total sales). Sales in North America increased by 210.7% to A$42.79 million. For the 52 weeks ending 3 Oct 2014, the stock was up 7.4% to A$5.95. PTM has a market capitalization of about A$3.45 billion.

PTM’s earnings before interest, taxes, depreciation and amortization (EBITDA) were A$261.72 million, or 81.8% of sales. PTM reported a net profit after tax of $189.9 million, which is 47.1% up from $129.1 million of 2013. On 23

rd September 2014, the Company paid fully-franked dividend of 20 cents per share as opposed to the fully-franked dividend of 14 cents per share on 17 March 2014. The total dividend for the year is 34 cents per share, which is up from what it paid last year.

The Company’s Funds under Management (FUM) has been the most important factor for its profit. FUM is impacted by individual funds and investment mandates. PTM reports that FUM increased to $22.3 billion in FY2014 from $16.8 billion in FY2013. There was an increase in performance fees earned to $27.4 million from $5.0 million of the previous year.

Expenses are generally resulting from costs associated with FUM growth, incentive payments, and staff costs. However, costs as a proportion of revenue have declined from 21.1% for FY2013 to 18.4% for FY2014. We note that the Company is offering a long-term incentive profit-share plan to its senior employees in place of the share grants / options. This adds to the cost heavily, Margins still look attractive nevertheless.

Net Operating Profit (Source – Company Reports)

Net Operating Profit (Source – Company Reports)

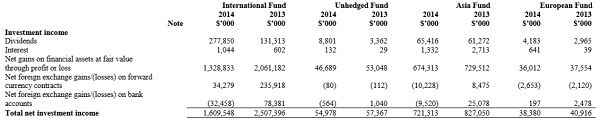

PTM also declared that investment returns steered the FUM increase. Capital flows were up by $0.2 billion and distributions net of reinvestments were a negative of $0.5 billion.

Investment Income (Source – Company Reports)

Investment Income (Source – Company Reports)

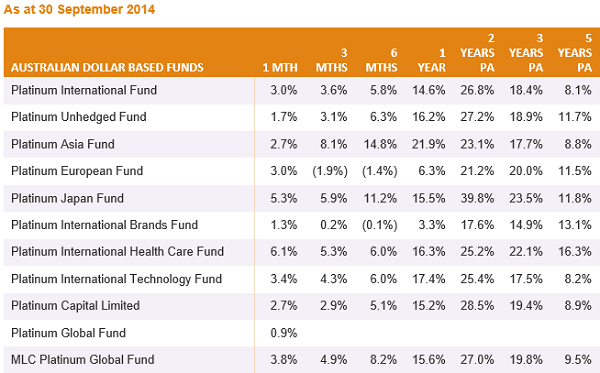

PTM’s star product – Platinum International Fund, which is known to deliver high-end performance usually, has appreciated 13.01% per annum. The Asia Fund delivered a strong performance while outpacing its benchmark. The Company has also made some changes to its regular investment plan to a minimum initial investment of $10,000 with a minimum $200 per month or quarter contribution in order to lure more investors.

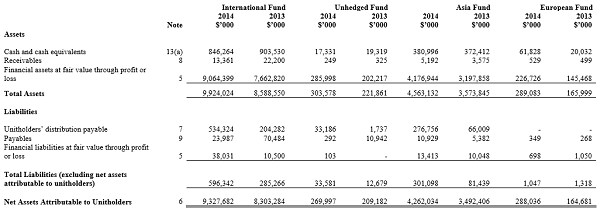

Assets and Liabilities (Source – Company Reports)

Assets and Liabilities (Source – Company Reports)

PTM reported a jolt in its attempt to launch the UCITS (Undertaking for Collective Investment in Transferable Securities) product on account of an unknowable tax legislation, which is currently under review by the government. In other words, the expected launch of the UCITS-based funds has been help-up due to tax complications. The Company, however, expects to achieve better opportunities with the launch of the mFund Settlement Service (mFund) on the Australian Securities Exchange. PTM plans to come-up with the product offering, the Platinum Global Fund, to counterpoise the funds rejection for eligibility for the first round of listings. mFund would be targeting a specific set of customers and will help the Company augment the brand image.

Fund Performance (Source – Company Reports)

Fund Performance (Source – Company Reports)

The Company also believes that mandated superannuation contributions will steer the high-margin retail funds under management. As per the Company’s outlook, PTM is contented with the progress on its capabilities and greater commitment to develop relationships with investors.

The positive sentiments with regards to the wealth management sector adds strength to PTM’s capabilities. Lower AUD would also be fuelling to PTM’s success by virtue of its FUM strong point and robust net-flows. Average net-flows of ~$40m a week were reported towards the end of FY 2014 and as a kick-start for FY2015, indicating a far better position for the Company. The net inflows compensated for the relatively weak performance.

PTM may also benefit from the enhanced apportionment to international equities. Further, the Company expects that reforms in countries like India and Indonesia may help get an exposure to an improving environment.

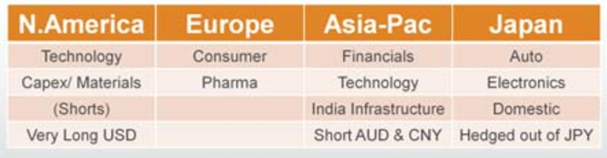

Key Sectors Exposures and FX Positions by Geography (Source – Company Reports)

Key Sectors Exposures and FX Positions by Geography (Source – Company Reports)

Over September 2014, the Company reported that Chinese equity markets were the star performer adding 14% in AUD. PTM is able to figure out quality businesses to invest on striking valuations. Investment via HK appears to be an important move for foreign investors who eye China as an interesting play. The Company sees an opportunity of deploying funds in India and China, with India having a focus on infrastructure, banks, property, construction and ports. In addition to India and China, Korean corporate rejuvenation also fascinates PTM. More or less, Company’s Platinum Asia Fund has been reported to focus on the following investment themes – Ecommerce, data and mobility; financial sector; and emerging market consumer, apart from above country-specific interests.

The Company confirmed that average FUM, investment performance and capital flows will drive its future growth. Specifically, the capital flows will be on an advantage based on new institutional mandates, tendency of Australian investors to have a diversified portfolio and the growth of self-managed superannuation funds.

Platinum’s Approach (Source – Company Reports)

Platinum’s Approach (Source – Company Reports)

However, the factors creating turbulence may include risks associated with performance of the Company with respect to its product and service offerings. We also see that the earnings are emanating from some specific funds, showcasing PTM’s reliability on few key investment personnel and the performance of its main funds. An underperformance by these funds or exit of any such key personnel can materially impact the present sweetened scenario.

PTM Daily Chart (Source - Thomson Reuters)

Given the current ambiance, the business momentum has bettered in view of Company’s efforts in re-establishing the portfolio performance and concentrating on distribution. As mentioned earlier, PTM has a healthy track record in international equities which enables it to charge investors a premium management fee. All-in-all, this brand in the Australian wealth universe appears to be benefitted by the international exposure and retail investor demand. Further, the high dividend payout ratio will be the bait for good growth and income returns from investment standpoint. Its operating margins, strong cash flows and long-short investment strategies add springiness to its footprint.

Accordingly, we put a

BUY recommendation for this stock at the current price of $5.77.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...