Kalkine has a fully transformed New Avatar.

Company Overview: Pinnacle Investment Management Group Limited, formerly Wilson Group Limited, is a multi-affiliate investment management company. The Company operates through two segments, including Pinnacle and Wilson Group. The Company's Pinnacle segment is engaged in developing and operating funds management business, and providing distribution services, business support and responsible entity services to the Pinnacle Boutiques and external parties. The Wilson Group segment is engaged in specialty funds management through priority funds; selected investments as principal, and servicing structured products for clients. In addition, the Company provides distribution and other support services to its affiliates and a select number of aligned investment managers. It holds equity interests in various specialist investment managers and provides them with a governance framework, working capital, seed funding, and a range of institutional quality, and distribution and other non-investment support services.

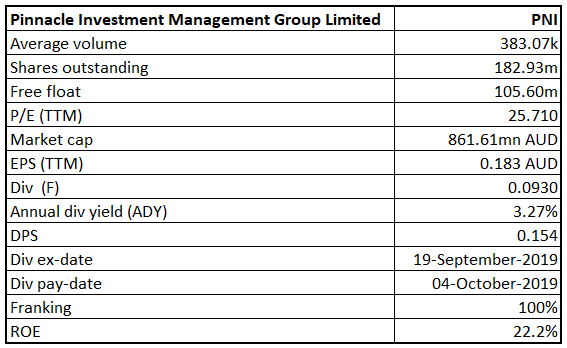

PNI Details

Exceeding Benchmarks Over the Past 5 Years: Pinnacle Investment Management Group Limited (ASX: PNI) is a leading Australia-based multi-affiliate investment management firm, which is engaged in development and operation of investment management businesses and provision of distribution services, business support and responsible entity services to the Pinnacle Affiliates. As on 14 January 2020, the market capitalization of the company stood at ~$861.61 million. The company has built a resilient and a diversified business which is expected to be enhanced by diversity of asset classes, diversity of sources of FUM and percentage of FUM exposed to performance fees. The top management in its recent Annual General Meeting stated that the company witnessed strong growth with an increase in funds under management, earnings and dividends. For the financial year ended 30 June 2019, NPAT (Net Profit After Tax) from continuing operations attributable to shareholders stood at $30.5 million, representing an increase of 32% from $23.1 million in the prior year. This was mainly due to higher starting FUM, continued investment in certain affiliates and low performance fees for FY19. This increase resulted in the earnings per share to increase by 28% to 18.3 cents per share from 14.3 cents in the prior year. The company also reported a strong balance sheet with $51.2 million of ‘liquid’ cash and principal investments. The principal investments of the company were boosted by capital raising and a debt facility of $30 million with the Commonwealth Bank to provide additional ‘dry powder’ or cash reserves.

The company has a track record exceeding 5 years, with its strategies and products exceeded their benchmarks over the past 5 years. This is a classic measure of ‘medium term performance’ consistency and excellence. As on 30 June 2019, total Funds Under Management have grown to $54.3 billion, demonstrating a substantial increase from $19.8 billion in FUM for the 2016 financial year. During FY19, Net Fund Inflows were $6.5 billion. Net Retail FUM Inflows came in at $2.9 billion, as compared to $2.2 million in the prior corresponding year. The improvement in financial performance has enabled the company to declare a fully franked dividend of 9.3 cents per share, bringing the total dividends to 15.4 cents per share.

The company is investing in new affiliates, which will add diversification through global equities, private capital and absolute return from single and multi-asset. With $51.2 million in cash and principal investments at the end of the year, the company is now anticipating opportunities to drive future growth. .png)

FY19 Financial Performance (Source: Company Reports)

Pinnacle Partners with Coolabah Capital: The company has recently announced that it has entered into an agreement to acquire 25% of equity interest in Coolabah Capital Investments Pty Ltd for a consideration of $29.1 million, together with a further of $5 million upon achieving certain milestones over the next 18 months to 4.5 years. The company will share revenues from capital raised with the institutional, retail and offshore distribution channels and will diversify its portfolio of affiliates, particularly in fixed income and alternatives.

Analysis of Historical Performance: The company in its recent presentation has stated that Funds Under Management increased from $19.3 billion as at 30 April 2016 to $56.9 billion as at 30 September 2019. Retail FUM as a percentage of total FUM has witnessed a rise from 8.3% ($0.9 billion) in FY13 to 21.4% ($11.6 billion) in FY19. The company consists of 13 Affiliates, offering a wide range of asset classes. The net profit after tax also increased from $4.7 million in 1H16 to $30.5 million in FY19. In FY19, shareholders received 15.4 cents of fully franked ordinary dividends per share, which compares to 3.3 cents of fully franked ordinary dividends per share in FY16, with a significant compounded growth of 67% p.a. This resulted in EPS to grow from 5.2 cents in FY16 to 18.3 cents in FY19, representing an increase of over 350%. Over a period of 4 years from FY15 to FY19, the company witnessed a CAGR (Compounded Annual Growth Rate) of 29.08% in revenue..png)

Retail FUM evolution (Source: Company Reports)

Growth in Performance Fee FUM: The company witnessed an increase in the proportion of Funds Under Management with the potential to earn performance fees from 16.7% at 30 June 2016 to 30% at 30 June 2019. The company continues to invest in market leading distribution capability and has a marketing team of 37 people across retail, institutional and offshore channels. The company is engaged in enhancing the platform, bringing strength and stability in-house to deliver a substantial range of active investment management services.

Diversified Client Base with Strong Net Fund Inflows: The company has a diversified client base with 78 institutional separate account clients and 95 institutional separate accounts across its affiliates. Despite the lower institutional basis point fees trend, the company witnessed growth in its aggregate fees with growing FUM. Also, large superannuation funds are willing to pay substantial fees for investment strategies and managers that produce attractive investment performance. The company expects to achieve robust net fund inflows in both the retail and the institutional markets in Australia, along with further developing its early distribution efforts in offshore markets to expand institutional sales.

Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of Pinnacle Investment Management Group Limited. Macoun Generation Z Pty. Ltd is the largest shareholder with a percentage holding of 11.42%..png)

Top 10 Shareholders (Source: Thomson Reuters)

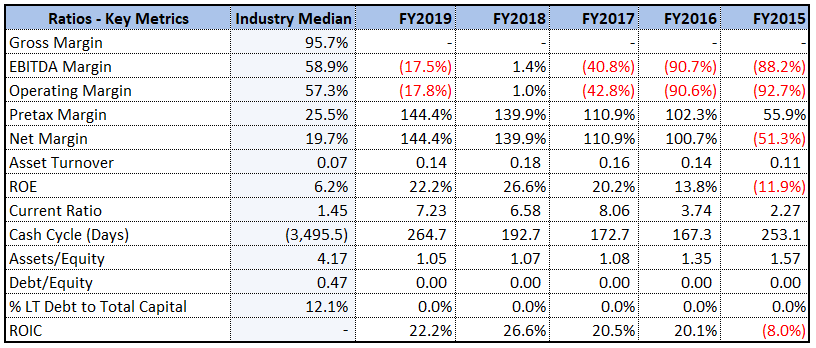

Increasing Returns to Shareholders: Over a period of 4 years from FY15-FY19, EBITDA margin witnessed a significant improvement, indicating increased profitability and focus on volume growth to increase the bottom line. During FY19, net margin of the company stood at 144.4%, higher than the industry median of 19.7%. This indicates that the company has better capabilities to convert its top-line into the bottom-line as compared to peers. In the same time span, Return on Equity stood at 22.2% as compared to the industry median of 6.2%. This indicates that the company is well deploying the capital of its shareholders and is capable to generate profits internally. During the year, current ratio of the company stood at 7.23x, higher than the industry median of 1.45x. This indicates that the company is liquid enough to pay off its current liabilities using its current assets. The company also reported a strong financial position with Debt/Equity ratio of ‘Zero’, lower than the industry median of 0.47x.

Key Metrics (Source: Thomson Reuters)

What to Expect from PNI: The company continues to seek world class investment teams in new asset classes. The new asset classes are expected to induce diversification across the company’s platform. This will help the company to build stability and meet the evolving needs of its clients. PNI is also ready for future growth and opportunities and has built a stronger balance sheet which will help it to cope up with challenging conditions. The company will further invest to enhance the distribution capability in the newer markets, namely direct to retail and international. The company will continue to explore opportunities across existing profitable investment management firms which can drive business growth and may be synergistic with its existing businesses and ambitions..png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: Price/Book Value Multiple Approach .png)

Price/Book Value Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of PNI gave a return of 1.95% in the past 6 months and a return of 6.80% in the last 3 months. The stock is slightly inclined towards its 52-weeks’ low level of $3.800, offering a decent opportunity for accumulation. To reiterate, the business reported a substantial increase in funds under management, earnings, and dividends. In order to push to growth trend into FY20, the company has added additional affiliates and investment strategies on the platform. Considering the returns, trading levels, decent financial performance, improving margins and higher return to the shareholders, we have valued the stock using a relative valuation method i.e. Price/Book Value multiple, and have arrived at a target price with upside lower double-digit (in % term). For the said purposes, we have considered Magellan Financial Group Ltd (ASX: MFG), Navigator Global Investments Ltd (ASX: NGI), and Pendal Group Ltd (ASX: PDL) as peers. Hence, we recommend a “Buy” rating on the stock at the current market price of $4.70, down by 0.212% on January 14, 2020.

PNI Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...