Company Overview: Pinnacle Investment Management Group Limited, formerly Wilson Group Limited, is a multi-affiliate investment management company. The Company operates through two segments, including Pinnacle and Wilson Group. The Company's Pinnacle segment is engaged in developing and operating funds management business, and providing distribution services, business support and responsible entity services to the Pinnacle Boutiques and external parties. The Wilson Group segment is engaged in specialty funds management through priority funds; selected investments as principal, and servicing structured products for clients. In addition, the Company provides distribution and other support services to its affiliates and a select number of aligned investment managers. It holds equity interests in various specialist investment managers and provides them with a governance framework, working capital, seed funding, and a range of institutional quality, and distribution and other non-investment support services.

.jpg)

PNI Details

Resilient and Diversified Business Model: Pinnacle Investment Management Group Limited (ASX: PNI) is a leading Australia-based multi-affiliate investment management firm. The market capitalisation of the company stood at ~A$841.49 million as on 26 November 2019. The company currently consists of 13 investment affiliates, with approximately $54.3 billion in assets across a diverse range of asset classes at 30 June 2019. The business continues to mature and prosper in all market conditions, however, not being immune to challenging conditions, it will increase its resilience, thus, allowing shareholders to benefit across the whole cycle. The company believes that resilience is enhanced when it (1) increases the diversity of asset classes under management, (2) increases the diversity of sources of FUM through industry leading distribution performance, and (3) retain a healthy percentage of funds under management exposed to performance fees.

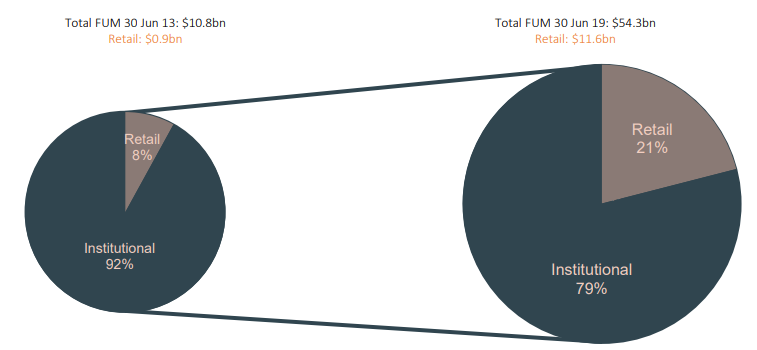

During FY19, the company encountered robust growth, as favourable movements were witnessed in its funds under management (or FUM), earnings and dividends. Existing affiliates grew their FUM and there have been addition of affiliates and investment strategies. Resourcing levels have been prudently expanded to cater for current and future growth, including in new markets. Notably, Retail FUM as a percentage of total FUM has increased from 8.3% at 30 June 2013 to 21.4% at 30 June 2019. The company continues to invest significantly in market-leading distribution capability. It now has a distribution and marketing team totalling 37 people, working across retail, institutional and offshore channels.

Looking at the past performance over FY16 to FY19, net profit after tax from continuing operations attributable to shareholders of the company have grown with a CAGR (compounded annual growth rate) of 73.9%. Group’s diluted EPS improved from 5.2 cents in FY16 to 17.1 cents in FY19, and dividend per share improved from 3.30 cents per share in FY16 to 15.40 cents per share in FY19. Moreover, it retained a decent and flexible balance sheet, and, thus it can be said that PNI's flexible balance sheet position might help it in making deployments towards strategic growth objectives, which might help in overall growth of the company.

Moving forward, there are expectations that sound liquidity levels, decent operational capabilities and RoE better than the broader industry median might help the overall company to gain traction among the market participants.

Growth in Retail FUM (Source: Company Reports)

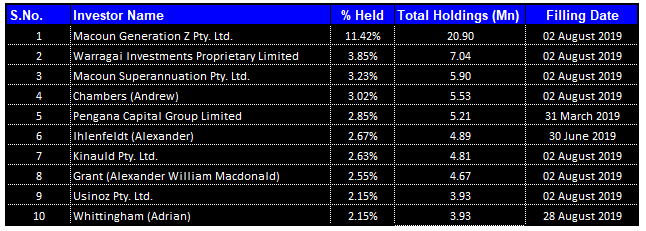

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Pinnacle Investment Management Group Limited:

Top 10 Shareholders (Source: Thomson Reuters)

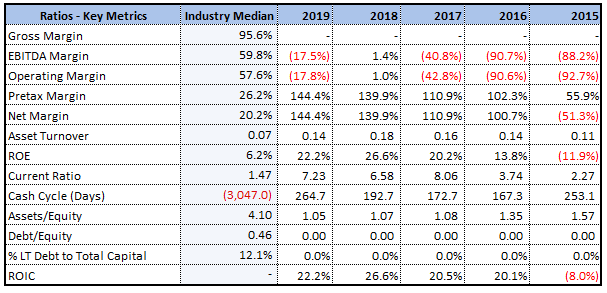

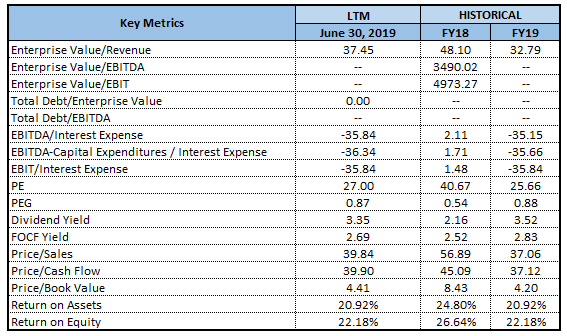

Key Ratios Better Than Industry Peers: Its RoE stood at 22.2% in FY19, which is above the industry median of 6.2%, which means that the company has provided good returns to its shareholders. The company’s current ratio is exceedingly well as compared to its peers. Current ratio stood at 7.23x in FY19, which is above the industry median of 1.47x, that makes it a better company to meet its short-term obligations. The company has also improved its net margins from 139.9% in FY18 to 144.4% in FY19, which shows the company has improved its ability to convert its top-line to the bottom-line.

Key Metrics (Source: Thomson Reuters)

Five New Affiliates Added: The company has a deliberate strategy to diversify into new asset classes with substantial growth potential. The company’s five new affiliates, i.e., Metrics Credit Partners, Omega Global Investors, Firetrail Investments, Longwave Capital Partners and Riparian Capital Partners are proof of this approach. In July 2018, the company purchased 35% interest in Metrics Credit Partners, a leading Australian non-bank corporate lender and alternative asset manager specialised in fixed income, private credit, equity and capital markets. Also, in July 2018, it acquired a 40% interest in Omega Global Investors, which offers smart beta, factor investing and client solutions (including ESG) capabilities.

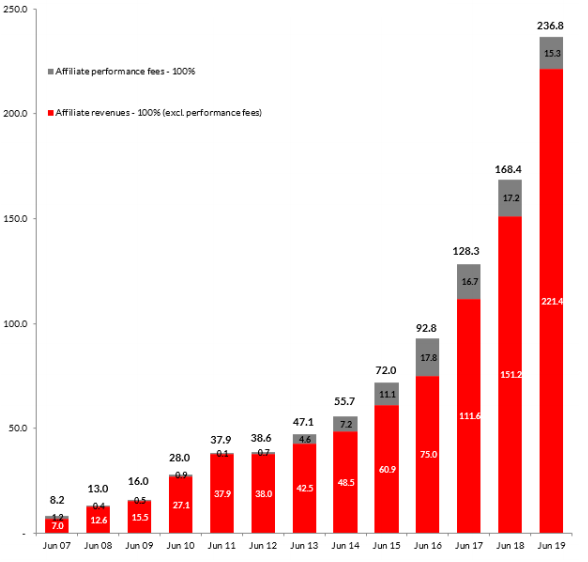

The aggregate funds under management of affiliates have grown to $56.9 billion by 30 September 2019. This was an increase of $18.9 billion, or 49.7% (including $6.8 billion ‘acquired’ in July 2018) on the FUM 15 months earlier, at the beginning of the 2019 financial year. The company’s net fund inflow was $6.5 billion during the 2019 financial year, out of which $2.9 billion was retail.

FY19 Financial Highlights: The company reported NPAT from continuing operations, attributable to shareholders of $30.5 million, up 32% from $23.1 million in the prior year. EPS (Earnings Per Share) stood at 18.3 cents, up 28% from 14.3 cents in the prior year. In FY19, shareholders have benefitted from 15.4 cents of fully franked ordinary dividends per share, which registers a compound growth rate of 67% per annum over the period when compared to 3.3 cents of fully franked ordinary dividends per share in FY16. The Board of thecompany has maintained the policy of paying out in excess of 80% of EPS each year as it has ample franking credits available.

Aggregate Affiliate Revenues ($ million) (Source: Company Reports)

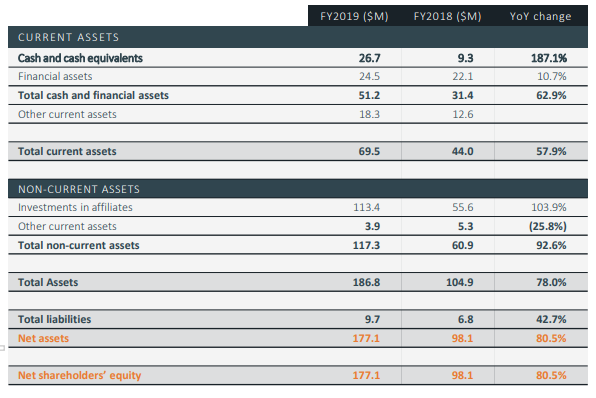

Strong and Flexible Balance Sheet: As at 30 June 2019, the company had $51.2 million of ‘liquid’ cash and principal investments, of which $23.2 million was invested with the company’s affiliates. The company’s cash and principal investments position was boosted by its capital raising in July 2018 and it has recently entered into a $30m debt facility with the Commonwealth Bank to provide additional ‘dry powder’.

FUM Figure as at October 31, 2019: The company’s FUM closed at $54.3 billion as at 30 June 2019, which increased to $57.3 billion as at 31st October 2019). Over the last ten years, the FUM has grown at a CAGR of 34.6% per annum and 31% by excluding $6.8 billion ‘acquired’ in July 2018. The increase in FUM of $16.3 billion in the year to 30 June 2019 mainly happened because of $6.8 billion which was acquired, net inflows of $6.5 billion, and market movements/ investment performance of $3.0 billion. Out of $6.5 billion net inflows to 30 June 2019, $2.9 billion was retail.

Balance Sheet (Source: Company Reports)

Performance Over the Years: In the last five years (FY15 to FY19), the company has registered a CAGR growth of 29.08% in top-line, thus, it can be said that the company has decent capabilities to garner revenues. The company has also improved its cash flow from operating activities. In FY15, the company generated negative cash flow of $3.61 million, but by the end of FY19 it generated cash flow from operating activities of $21.09 million and, therefore, it can be said that PNI’s operational capabilities have improved.

Ready to Grab New Opportunities: The company has built and will maintain a robust balance sheet which will allow it to consider opportunities that would be expected to present themselves in challenging conditions. The company’s key personnel have stated that they have been building Pinnacle by taking measured approach towards growth. They are also focusing towards supporting growth of the current affiliates with the increased investment towards the distribution channels as well as infrastructure. The company would continue to invest in new Affiliates where management teams possess a strong track record along with growth potential.

The company has capital available to seed new affiliates, facilitate Affiliate equity recycling, and respond to any very high quality ‘Horizon 3’ opportunities that may arise. For that, it has recently entered into a $30 Mn borrowing facility with the CBA, to be used as additional ‘dry powder’ in the event that attractive ‘Horizon 3’ opportunities were to arise; and in the meantime, these funds will be deployed as investments in appropriate liquid funds of affiliates, including for the seeding of new funds.

Key Valuation Metrics (Source: Thomson Reuters)

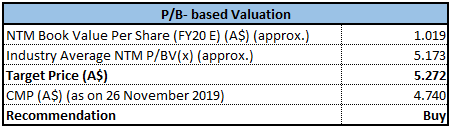

Valuation Methodology: P/BV based approach

P/BV based approach (Source: Thomson Reuters), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters

Stock Recommendation: The stock of PNI has delivered a return of 1.32% in the span of previous three months, while on YTD basis, the stock has witnessed a rise of 8.24%. The cash and cash equivalents rose $17.4 million and the figure stood at $26.7 million at year-end as compared to $9.3 million at the end of previous year. Additionally, cash inflows from operating activities amounted to $20.9 million, that included dividends received from Affiliates amounting to $27.0 million, as compared to $17.7 million in the previous year. In FY19, a fully franked final dividend amounting to 7.0 cents per share was paid on October 5, 2018 and an interim dividend (fully franked), which amounted to 6.1 cents per share was paid on March 22, 2019. Based on the foregoing, we have valued the stock by using a relative valuation method, i.e., P/BV multiple, and arrived at a target price of lower double-digit growth (in % term). Hence, we give a “Buy” recommendation on the stock at the current market price of A$4.740 per share (up 3.043% on 26 November 2019).

.png)

PNI Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

AU

AU

Please wait processing your request...

Please wait processing your request...