Kalkine has a fully transformed New Avatar.

Company Overview: Pinnacle Investment Management Group Limited, formerly Wilson Group Limited, is a multi-affiliate investment management company. The Company operates through two segments, including Pinnacle and Wilson Group. The Company's Pinnacle segment is engaged in developing and operating funds management business, and providing distribution services, business support and responsible entity services to the Pinnacle Boutiques and external parties. The Wilson Group segment is engaged in specialty funds management through priority funds; selected investments as principal, and servicing structured products for clients. In addition, the Company provides distribution and other support services to its affiliates and a select number of aligned investment managers. It holds equity interests in various specialist investment managers and provides them with a governance framework, working capital, seed funding, and a range of institutional quality, and distribution and other non-investment support services.

.png)

PNI Details

Significant Increase in FUM Witnessed in FY19: Pinnacle Investment Management Group Limited (ASX: PNI) is a small-cap multi-affiliate investment management firm with the market capitalisation of circa $841.19 Mn as of 17 September 2019. It provides investment management services through its affiliated boutiques to a portfolio of investment managers across a range of complementary investment styles. Recently, the company posted a decent set of numbers for FY19 wherein profitability continued with robust net margin. The company reported revenue from continuing operations of $21.1 million in FY19, exhibiting a growth of 27.7% on Y-o-Y basis. Profit after tax from continuing operations stood at $30.5 million as compared to the prior year figure of $23.1 million. Resultantly, basic earnings per share came in at 18.3 cents in FY19, showing a decent rise of 28.0% from 14.3 cents in FY18. Currently, Pinnacle has 13 investment Affiliates, namely Antipodes, Firetrail, Hyperion, Longwave, Metrics, Omega, Palisade, Plato, Resolution Capital, Riparian, Solaris, Spheria and Two Trees. As at June 30, 2019, Pinnacle Affiliates collectively managed approximately $54.3 billion in assets across a diverse range of the asset classes which reflects a significant increase of 42.9% on funds under management (FUM) as at June 30, 2018. During the span of 6-month period from December 31, 2018 to June 30, 2019, FUM of PNI’s 13 Affiliates grew by $7.6 billion or 16.3%, which comprises of net fund inflows amounting to $1.5 billion and market movements/investment performance of $6.1 billion. As per the company’s Chair named Alan Watson, the company has been delivering on the medium-term mission, which was described to the shareholders when it became pure-play funds management group back in 2016. It was also mentioned that PNI has continued robust growth, with FUM, earnings and dividends all witnessing substantial growth. Also, the existing affiliates have grown the Funds Under Management, additional affiliates, as well as investment strategies, have been added, while the resourcing levels have been prudently expanded in order to cater for the current and future growth, including in the new markets.

The company continues to diversify its business with the new, high-quality affiliates. It was added that recently established affiliates, like Spheria and Firetrail, have grown rapidly since inception. Additionally, the company is expected to be supported by the decent liquidity levels and by capabilities to garner revenues. Needless to say, a robust and flexible balance sheet can act as a primary tailwind for long-term growth.

.png)

Five-Year Financial Highlights (Source: Company Reports), *Non-statutory measure

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Pinnacle Investment Management Group Limited:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Key Margins Higher Than Industry Median: The key margins of Pinnacle Investment Management Group Limited of FY19 are higher than the industry median, which reflects that the company has better fundamental base. This decent base might help it in gaining traction among the market players moving forward. The company’s RoE (or Return on Equity) stood at 22.2% in FY19, which is comfortably higher than the industry median of 6.2% and, thus, it can be said that PNI has been delivering better returns to its shareholders as compared to the broader industry. The company’s current ratio stood at 7.23x in FY19 as compared to the industry median figure of 1.46x and, therefore, looks like that PNI has a decent liquidity footing which could help it in meeting short-term obligations. PNI could also make deployments towards key strategic activities which could support the long-term growth.

.png)

Key Metrics (Source: Thomson Reuters)

Update on Retail FUM: Retail FUM stood at $11.6 billion as at June 30, 2019 (which includes $0.7 billion ‘acquired’ in the month of July 2018), as compared to $9.4 billion as at December 31, 2018, and $7.9 billion as at June 30, 2018. The growth of $3.7 billion for the financial year was because of $2.9 billion net inflows (out of which $1.0 billion was in the LICs/LITs), $0.7 billion acquired and the remainder was because of market movements/investment performance. The following picture provides a broad overview of retail FUM evolution:

.png)

Retail FUM evolution (Source: Company Reports)

Pinnacle has deployed significantly towards the retail distribution and has generated the substantial retail FUM in the span of last five years.

Buy-back and Cancellation of Shares: Pinnacle Investment Management Group has recently advised that, in accordance with the Pinnacle Omnibus Incentive Plan, it is undertaking the employee share scheme buy-back of 150,000 ordinary shares. Asper the release dated September 6, 2019, the shares are held by the former employee(s) who are no longer entitled to shares in accordance with the terms of the plan. It was added that the buy-back, as well as subsequent cancellation of shares, would be implemented on September 18, 2019.

Significant Increase in Cash and Cash Equivalents: The company’s revenue from continuing operations witnessed a rise of $4.6 million and stood at $21.1 million, from $16.5 million generated in the prior period. The 2019 financial year witnessed a robust performance in Pinnacle’s affiliated investment managers, as there were record FUM, FUM inflows and affiliate revenues achieved. Pinnacle’s share of net profit post tax from the equity interests in affiliates stood at $33.1 million, which reflects a rise of 32.9% as compared to the previous year. The revenues and costs within Pinnacle grew significantly as the business has been strengthening ahead of further growth and diversification. The company’s cash and cash equivalents witnessed a rise of $17.4 million and stood at $26.7 million at the year-end as compared to $9.3 million in the prior year. The cash inflows from operating activities amounted to $20.9 million, that included the dividends received from the affiliates, which were $27 million, as compared to $17.7 million in the previous year. The company wrapped up a successful capital raising event in the month of July 2018, which resulted in raising a net $67.5 million. It was added that $48 million was deployed towards Metrics and Omega transactions, and further $6.9 million was deployed towards other affiliates in accordance with the Pinnacle’s commitments under the various shareholders’ agreements.

.png)

Financial Metrics (Source: Company Reports)

Dividend Declaration: The Board of Directors declared a fully franked final dividend of 9.3 cents per share to the shareholders recorded on register on September 21, 2019, and it will be payable on October 4, 2019. As a result, the total dividend for FY19 amounted to 15.4 cents per share. The company is also possessing a robust and flexible balance sheet which could help it in witnessing long-term growth.

What to Expect from PNI Moving Forward: The company has been focusing on managing a business in order to maximize the profits and company value over the medium term. As per the presentation, there have been efforts to build Pinnacle with the help of a measured approach to growth. PNI would continue to evolve in response to as well as in anticipation of the market developments, and it has a very diversified base of clients (i.e., 78 institutional separate account clients, 95 institutional separate accounts throughout its affiliates). It was also mentioned that the retail FUM has been growing, in absolute terms and as the proportion of total FUM.

The company will continue to deploy towards the activities which it believes to bring substantial benefits over the medium term, while recognising the such kind of investment which may constrain the profits to some degree in short-term. Additionally, the company will remain vigilant to the potential opportunities which may arise, including potentially because of the changes in funds management industries, domestically and internationally. It was stated that the company’s results, as well as outlook, are influenced by the equity market conditions and, to a lesser extent, by the broader economic trends and also by investor sentiment.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

Method 1: PE- Based Valuation

.png)

PE- Based Valuation (Source: Thomson Reuters), *NTM: Next Twelve Months

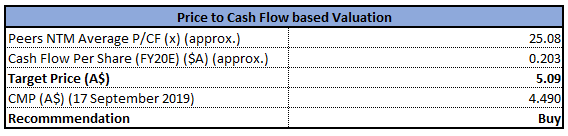

Method 2: - Price to Cash Flow based Valuation

Price to Cash Flow based Valuation (Source: Thomson Reuters), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters.

Stock Recommendation: The stock of PNI has witnessed a fall of 11.37% in the span of previous three months while, in the time frame of past six months, it has fallen 21.77%. Currently, the company’s stock is trading towards its 52-week lower levels of $3.80, proffering a decent opportunity for accumulation. The company’s focus remained towards supporting each of the affiliates and help them to grow their business and profitability, as well as expanding the distribution and infrastructure capabilities in order to support future growth. The company’s total revenues have witnessed a CAGR growth of 29.08% between the time span of FY15- FY19 and, thus, it can be said that the company is possessing decent capabilities to garner revenues. These capabilities might help it in achieving respectable growth moving forward, which could attract the attention of market players. Based on the foregoing, using two relative valuation methods, i.e., Price to Earnings multiple and Price to Cash flow multiple and arrived at the target price of the stock in the range of $5.09 to $5.38 (lower double-digit upside (in %). Hence, we recommend a “Buy” rating on the stock at the current market price of A$4.490 per share (down 2.391% on 17 September 2019).

PNI Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...