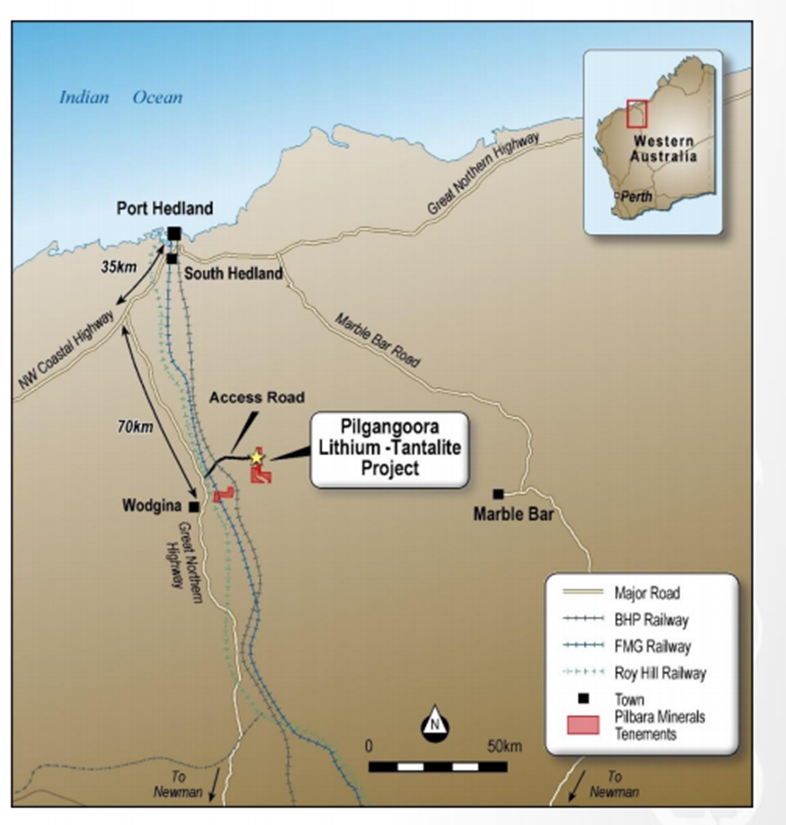

Company Overview - Pilbara Minerals Limited is an Australia-based mining and exploration company. The Company is focused in the Pilbara region of Western Australia. The Company’s Tabba Tabba tantalite project is located 75 kilometers east of Port Hedland and has a production rate of 30,000 pounds of tantalite per annum. The West Pilbara Mineral Tenements is located south of the regional center of Karratha in the West Pilbara region of Western Australia covering approximately 800 square kilometers. The project areas is considered to be prospective for base metals, platinum group elements and gold mineralisation associated with concealed greenstone sequences or layered mafic-ultramafic intrusions. The Company consists of seven granted exploration licenses in West Pilbara Mineral Tenements. The Pilgangoora Project consists of five tenements, including two exploration licenses and three mining leases covering an area of 31 square kilometers, which are prospective for tantalum and lithium mineralisation.

.png)

PLS Details

Wins second largest Spodumene project in the world: Pilbara Minerals Ltd (ASX: PLS) won the Pilgangoora Lithium-Tantalum project. This is the second largest Spodumene project in the world. Mining Plus has completed the mining pre-feasibility study (PFS) and accordingly they confirm technical and financial viability of 2 MTPA Pilgangoora development.

Pilbara Minerals has also signed eight-product off-take MOUs with leading chemical and technical grade customers for 100% forecast production. The company is targeting construction from December 2016 and commissioning from December 2017. Pilbara Minerals is emerging as a low-cost producer of lithium and tantalum at Pilgangoora.Furthermore, the project offers strategic advantages for infrastructure access, mining approvals and lower cost of operations. The project has strong fundamental and very low forecast cash operating costs. It’s a high margin project set to deliver outstanding cash flows and returns. The initial mine life is of 15 years based on current reserve with significant growth potential.

Pilgangoora Lithium-Tantalite is a robust, long-life project in a Tier-1 mining jurisdiction (Source: Company Reports)

Solid prospects for PFS: The group finished the JORC Inferred /Indicated and reported an 80Mt Resource while the project has 2 MTPA mining and on-site processing. Moreover, the group forecasts further resource prospects but for now, they are forecasting to have annual production of over 330 KTPA of 6% Spodumene concentrates (48 ktpa of lithium carbonate equivalent) and 274,000 lbs pa of tantalite. Additionally, it has maiden ore reserves of 29.5 Mt @131%Li

2O and 134 ppm Ta

2O

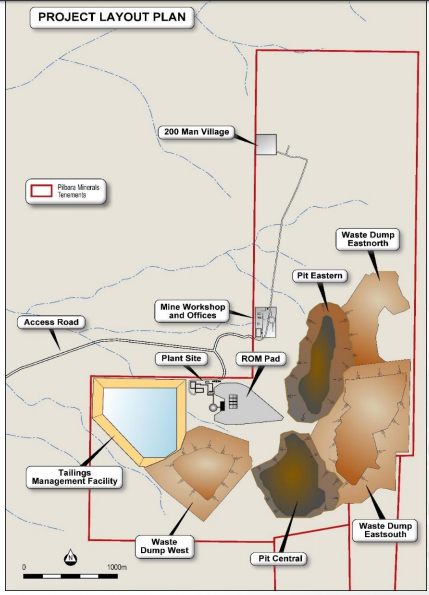

5. The group expects to have EBITDA over first 5 years of operations of around $120 million per annum. The project capital is estimated at $184 million. Meanwhile, the average Spodumene price is US$456/t FOB while current Spodumene price is US$600/t at margin of 60%. The likely reserve of Spodumene is 29.5 MT with average 2 MTPA for 15 years. DFS is targeting mining inventory of 53.9 MT, which could increase mine life to circa 30 years suggesting potential expansion of 3 MTPA. The stage 3 process is underway wherein the group is preparing a detailed Design and Project Planning, and targeting more than 25 years of mine life. Under the stage 3 process, the group is also preparing thePlant process and design optimization and developing a product specification and bulk samples for customers.

The group is also preparing the Tailings design, OPEX, CAPEX and even updating their financial models. The stage 4 of Pilgangoora DFS is project delivery and the group expects to deliver this by December 2016.

Technically and financially robust long-life project (Source: Company Reports)

Boosting capital position via SPP:Pilbara Minerals reported that they would raise over $100 million through a share placement and share purchase plan at $0.38 each. The steep discount to market price is offered for issue. Pilbara’s existing cash reserves of $12 million and the issue would boost the company’s cash to over $106 million after capital raising costs. The new funds would enable Pilbara to rapidly advance its Pilgangoora Lithium-Tantalum Project in Western Australia into production, and take advantage of strong market conditions and rapidly increasing demand for lithium. On the other side, the total capex funding requirement for this projects is $184 million plus working capital. Recently, the group announced that they closed their Share Purchase Plan on 18 May 2016 and shares were heavily oversubscribed, leading to a total of over $50.68 million.

The maximum value of the shares via the SPP offer price is limited to $15 million. Applicants having less than 5,000 shares as of May 20 would not be allotted securities under this offer.

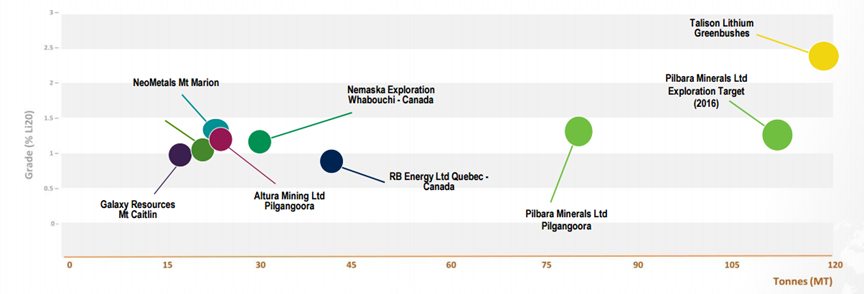

Peer Comparison – Resource Tonnage and Grade (Source: Company Reports)

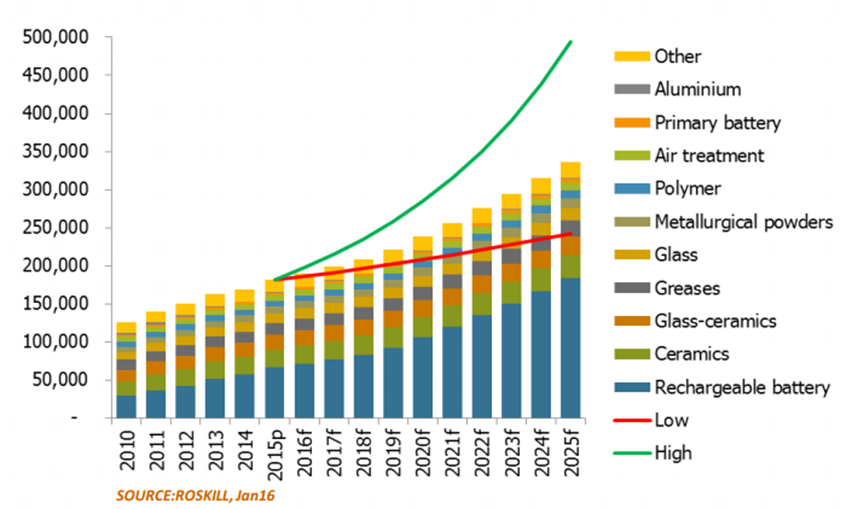

Strong demand for lithium ion battery: Lithium-ion batteries have been in demand from quite a while now and delivered a 20% annual growth from 2000. The Electric Vehicles and E-Bikes presently have over 3% of global lithium market while this growth has been ramping up from 2015. Conventional applications account over 70% of the global market whileGlass & ceramics use technical grade concentrate. Meanwhile, the demand from the automobile sector is a major growth driver and rising demand from vehicles will keep the run rate going at rapid space. Pilgangoora spodumene concentrates have met the metallurgical specifications of the entire range of lithium products and around 100% of projected lithium oxide production are subject to MOUs with major off-take partners located at China, Japan, Americas and Europe. These partners expressed their solid substantial expansion plans in order to leverage the projected demand for EV’s. As per the Motor Vehicle Lithium Demand, the Tesla Series 3 is expected to launch by 2017 for a retail price of US$36,000 while the Chinese car manufacturers are forecasting a sub $20K EV’s by 2017. Mercedes Benz is set to launch 12 new models of EV’s by 2017 while BMW i3 Series is forecast to release by 2017 to give direct competition to Tesla Series 3.

Audi and Volkswagen are also entering the EV market in 2017 -2018 while 30 Million E Bikes are expected to be produced annually in China, progressively converting to Li ion batteries. Moreover, China, Japan and Korean Government also have favorable policies to support EV’s with large rebates, zero sales tax and free licensing. But, Lead -acid batteries are currently subject to export tax out of China. Even Toyota would stop using lead acid batteries from 2017 and intends to entirely adopt Li ion batteries in all models. With regards to Japanese and Korean car plans, the makers are forecasting to announce a major adoption of EV’s by 2020. Accordingly, the chemical lithium products expansion is growing rapidly restrained by lack of mine supply.

World forecast demand for Lithium by first use (Source: Company Reports)

Stock Performance:The shares of PLS have been delivering an outstanding performance during this year to date and delivered over 116.67% (as of May 31, 2016) during the period driven by the high prospects Pilgangoora Lithium-Tantalum project. Meanwhile, Pilbara is undertaking diamond drilling to extract samples for network as well as bulk samples for marketing. These samples would be important in converting MoUs to binding agreements, and we believe that the group would be successful in building pipeline. Considering the strong market condition, high lithium prices and rapidly rising demand for lithium, the company is set to achieve strong revenues and profit growth post production from this project. However, investors need to track the growth in lithium prices as well as the production/ extraction costs involved in the project. But, we remain bullish on the stock despite this rally and we believe that the stock has the capability of rallying further in the coming months. The stock has been consolidating in the last four weeks and rose 2.36% (as of May 31, 2016) in the last five days, while we believe investors could enter the stock to leverage the further growth potential in the stock.

The upcoming launches from motor vehicles industry would continue to contribute to the stock performance in the coming months. Based on the foregoing, we give a “Buy” recommendation on the stock at the current market price of $0.66

.PNG)

PLS Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...