Kalkine has a fully transformed New Avatar.

Company Overview: Perseus Mining Limited is engaged in mining operations and sale of gold, mineral exploration and gold project evaluation and development in the Republics of Ghana, Cote d'Ivoire and Burkina Faso, in West Africa. The Company's segments include Australia, Ghana and Cote d'Ivoire. The Australia segment is engaged in investing activities and corporate management. The Ghana segment is engaged in mining, mineral exploration, evaluation and development activities. The Cote d'Ivoire segment is engaged in mineral exploration, evaluation and development activities. The Company holds over 90% of Edikan Gold Mine (EGM), approximately 90% of Grumesa Gold Project, over 90% of Yaoure Gold Project and approximately 86% of Sissingue Gold Mine. It has commenced exploration at various near-mine prospects, including Bokitsi, Mampong, Pokukrom and the Agyakusu prospecting license. It has also commenced exploration at other prospects in Cote d'Ivoire, including the Mbengue, Mahale and Napie licenses.

.jpg)

PRU Details

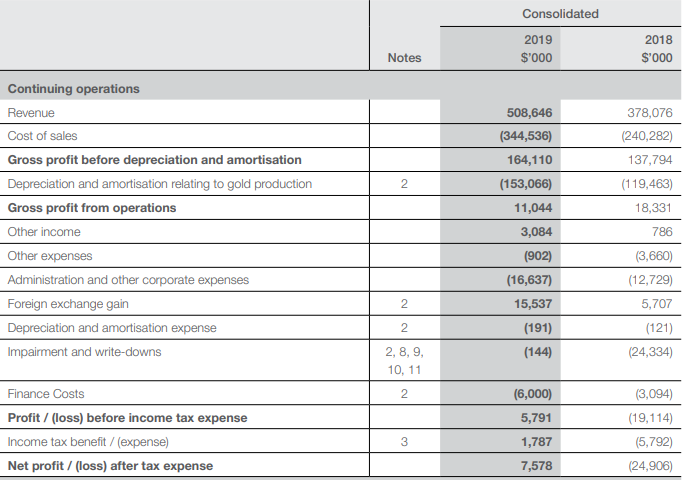

Gold Production Expected to Increase to 500K per annum by FY22: Perseus Mining Limited (ASX: PRU) is involved in the gold exploration, mineral exploration and gold project development in the Republic of Ghana and the Republic of Côte d’Ivoire, both located in West Africa. The group recognizes revenue from gold bullion sales as its obligations are satisfied in accordance with an agreed contract between the group and its customers. Revenue is recognized at a point-in-time when the gold bullion has been credited to the metals account of the customer. Looking at the past performance over FY14 to FY19, total revenue of the company has grown with a compound annual growth rate (CAGR) of 14.13%. In FY19, group’s revenue stood at $511.7 Mn, as compared to $264.2 Mn in FY14. Group posted a net profit after tax of ~$7 Mn in FY19 as compared to a loss of $30.9 Mn in FY14.

Production for FY19 increased by 6% over the previous year, supported by a reduction in average All-In Site cost by 8% over the previous year. Moreover, cash and bullion position at the end of FY19 stood at a remarkable position of $168.3 Mn.

Going forward, the Company is expected to produce 260-300K ounces of gold in FY20, with AISC of US$800-975 per ounce. Two of its important mines, Edikan and Sissingué are expected to deliver decent gold production in the upcoming period. Production at its third gold mine, Yaouré is also expected to deliver decent result in the coming times. Total gold production is expected to increase to 500,000 ounces per annum by FY2022.

.png)

Group’s Mineral Resources Data (Source: Company Reports)

.png)

Group’s Ore Reserves Data (Source: Company Reports)

FY19 Key Highlights for the year ended June 30, 2019: Group’s net profit after tax for the period was reported at $7.6 Mn, as compared to net loss after tax of $24.9 Mn in the previous year. This improvement can be attributed to an increase in revenue, predominantly resulting from higher gold sales, following the commencement of commercial production at Sissingué. The increase in profit was also favored by a reduction in impairment expense to $0.1 Mn (related to Nsuaem prospect in Ghana), as compared to the impairment of asset values and write-offs amounting to $24.3 Mn in the previous year. Additionally, depreciation of AUD versus USD helped to gain $15.5 Mn, an increase of 172% on the previous year.

FY19 Income Statement (Source: Company Reports)

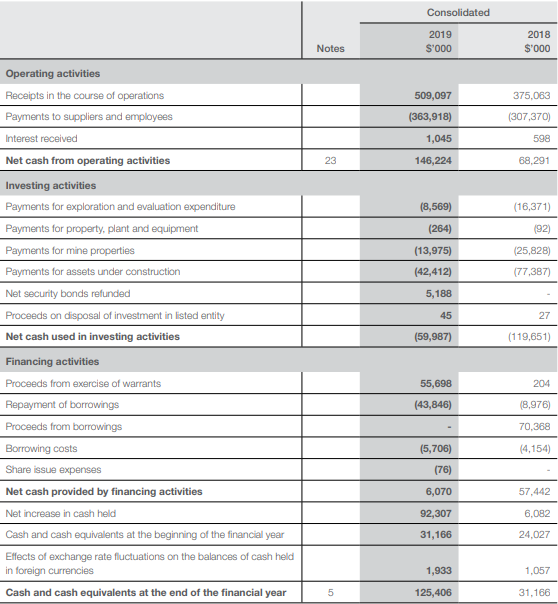

Cash On Hand on June 30, 2019 increased by ~302% on yoy: With gold price of US$1,409/oz and an AUD:USD exchange rate of 0.7029 on June 30, 2019, total cash and bullion balance was reported at $168.3 Mn, as compared to cash and bullion balance of $89.8 Mn in the previous year with gold price of US$1,250/oz and an AUD:USD exchange rate of 0.7411 as on June 30, 2018. Cash on hand was reported at $125.4 Mn, as compared to $31.2 Mn in the prior year, and bullion on hand was reported at 21,388 ounces (worth $42.9 Mn), as compared to 34,763 ounces (worth $58.6 Mn) in the prior year. The group held an additional deposit of $8.6 Mn as on June 30, 2019, as compared to $12.9 Mn in prior year, supporting performance guarantees for environmental rehabilitation of the Edikan Gold Mine (EGM) and Sissingué Gold Mine (SGM). The group held security holdings in Manas Resources Limited of $0.5 Mn and in Amani Gold Limited of $45K.

Under its debt facility, the company paid its loan obligations towards Macquarie for its Sissingué project, reducing outstanding debt from US$38 Mn on June 30, 2018 to US$11 Mn on June 30, 2019. Further, capital debt facility balance for its Edikan project reduced from US$25 Mn on June 30, 2018 to US$20 Mn on June 30, 2019. During the year, the company signed a corporate cash advanced facility of US$150 Mn with a consortium of three international banks.

Group’s net assets as on June 30, 2019 were reported at $783.5 Mn, as compared to $714.3 Mn in the previous year. The result was relatively constant, predominantly due to an increase in cash, offset by a decrease in mine properties.

FY19 Cash Flow Statement (Source: Company Reports)

Key Highlights of September’19 Quarter:

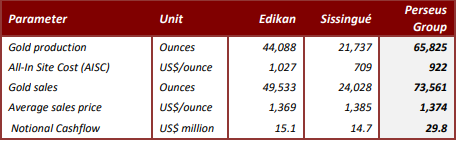

Gold production at Edikan mine and Sissingué mine for the period stood at 44,088 ounces and 21,737 ounces, respectively, taking the total production for September quarter at 65,825 ounces. All-In Sustaining Cost (AISC) for Edikan mine and Sissingué mine for the period stood at US$1,027 per ounce and US$709 per ounce, respectively, with AISC for the group at US$922 per ounce. Gold sales for Edikan mine and Sissingué mine for the period stood at 49,533 ounces and 24,028 ounces, respectively, taking the total gold sales at 73,561 ounces. Average sales price for Edikan mine and Sissingué mine for the period stood at US$1,369 per ounce and US$1,385 per ounce, respectively, averaging to US$1,374 per ounce for the group.

September’19 Quarter Operational Metrics (Source: Company Reports)

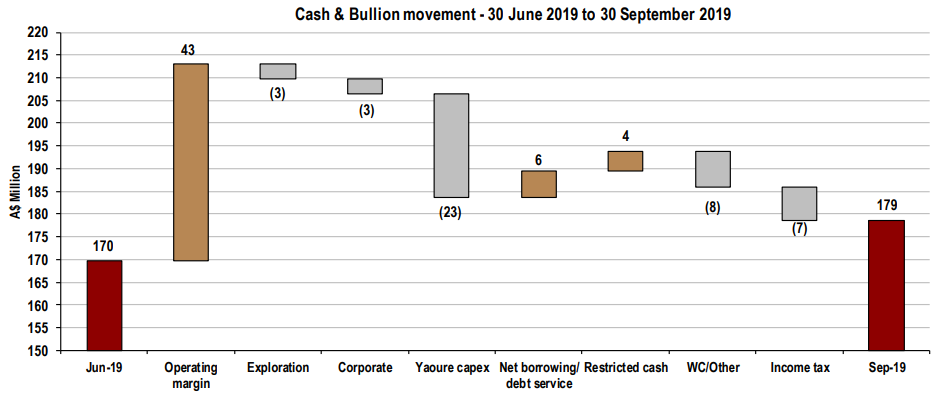

Cash & Bullion Balance for Sep’19 Qtr Increased By 5% than June’19 Qtr: As per the company’s balance sheet, notional cashflow by operations was reported at US$29.8 Mn. Around US$40 Mn of debt funding were drawn under the recently established US$150 Mn corporate debt facility, to repay pre-existing project loans. Total cash and bullion as on September 30, 2019 was reported at US$120.6 Mn, with a gold price of US$1,485 per ounce and AUD:USD exchange rate of 0.6754. Cash on hand was reported at US$ 98.5 Mn, and bullion on hand was reported at 14,843 ounces (worth US$22 Mn). The cash and bullion balance increased by ~5%, mainly due to a material decrease in AUD:USD exchange rate during the quarter. Net cash and bullion after drawn debt of US$40 Mn were reported at US$80.6 Mn.

Quarterly Cash and Bullion Movements (Source: Company Reports)

Gold Hedging:

During the quarter, the spot deferred sales held for the debt facility were rolled out over the three-year period ending in 2022. Gold forward sales contracts at the end of the quarter were reported at 232,668 ounces of gold at a weighted average sales price of US$1,307 per ounce, designated for delivery over the period up to June 30, 2022. The company also held 34,931 ounces of gold at an average sales price of US$1,456 per ounce for spot deferred sales contracts. With this, the company’s total hedged position at the end of September quarter was reported at 267,599 ounces at a weighted average sales price of US$1,327 per ounce.

Recent Updates:

On October 21, 2019, the company informed the market about the appointment of Mr David Ransom to the role of non-executive director. On November 29, 2019, the company’s shareholders will be asked to elect Mr Ransom as a director. His appointment would take the number of directors in the board to six, five of whom would be independent, non-executive directors. He has directly managed exploration programs in many companies in Australia and Canada, and also served as an independent consultant in the global mining industry for many years.

On the same date, PRU announced the decision of a founding Director, Mr Colin Carson, to retire as an Executive Director of the company at Annual General Meeting to be held on November 29, 2019.

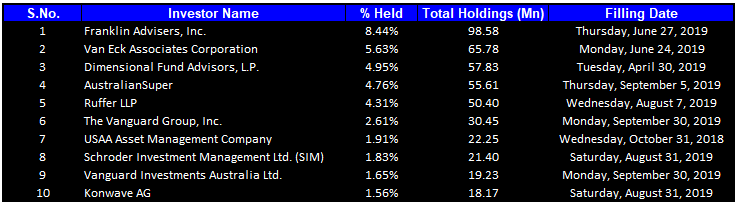

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 37.65% of the total shareholding. Franklin Advisers, Inc. and Van Eck Associates Corporation hold maximum interests in the company at 8.44% and 5.63%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

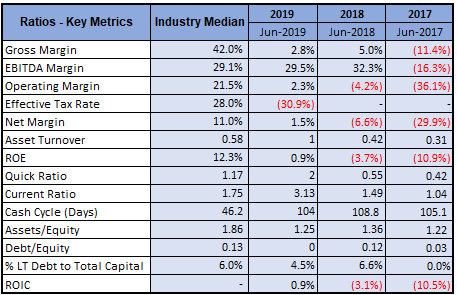

A Quick Look at Key Metrics: Its EBITDA margin for FY19 stood at 29.5%, better than the industry median of 29.1%. Its net margin improved from -6.6% in FY18 to 1.5% in FY19. Its current ratio for FY19 stood at 3.13x, better than the industry median of 1.75x, which implies that the company is in a better position to address its short-term obligations. Its long-term debt to total capital for FY19 stood at 4.5%, lower than the industry median of 6.0%.

Key Metrics (Source: Thomson Reuters)

Key Risks: The company is susceptible to a variety of financial risks such as market risk, interest rate risk, credit risk, liquidity risk, and equity price risk.

What to expect: The company has forecasted a decent, grade-driven performance in terms of both production and AISCs in the second half of FY20 relative to the first half of FY20. Gold production for the first half of FY20 has been estimated in the range of 120-140k ounces and for the second half of FY20, production is anticipated to be in the range of 140-160k ounces, taking the full year guidance to 260-300k ounces. All-In Sustaining Cost (AISC) for the first half period has been estimated at US$850-1,000 per ounce and for second half, AISC has been estimated at US$750-950 per ounce.

Yaouré Gold Mine development:

Development work at Yaouré Gold Mine is progressing well, in-line with the schedule and within the budget. By the end of September’19 quarter, out of the total capital budget of US$265 Mn, US$135 Mn has been committed, and US$61 Mn was expensed. Despite the increased seasonal rainfall, site earthworks at the proposed plant site and tailings storage facility remained unaffected and advanced as scheduled. Mine development also remained on schedule to achieve the stretch target of pouring first gold pour in December 2020.

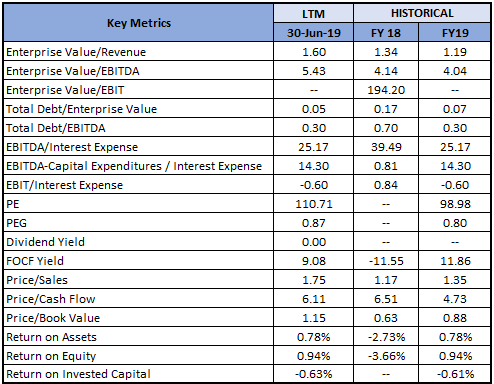

Key Valuation Metrics (Source: Thomson Reuters)

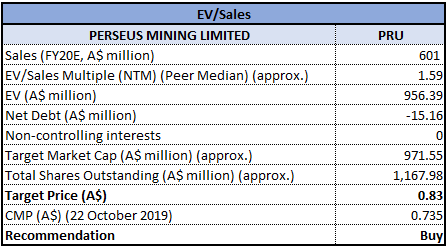

Valuation Methodology 1: EV/Sales Multiple Approach:

EV/Sales Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

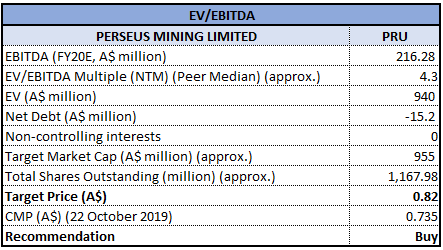

Valuation Methodology 2: EV/EBITDA Multiple Approach:

EV/EBITDA Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock price rose by 73.86% in the past six months, and in the span of one year, it has delivered a decent return of 98.70%. The group delivered a decent top-line and bottom-line performance in FY19, and the performance is expected to be continued given a positive production guidance for FY20. With Yaouré (third gold mine) coming on stream, company’s production level is expected to increase to 500,000 ounces of gold per year, which means that PRU will be in a position to continue to generate a material amount of free cash flow and significant profits. At the current market price of $0.735, the stock is available at a price to earnings multiple of 115.910x. Looking at the business prospects over the long-term, we have valued the stock using two relative valuation methods, i.e., Enterprise Value to Sales and Enterprise Value to EBITDA multiples, and arrived at a target price of low double-digit growth (in % term). Hence, we give a “Buy” recommendation on the stock at the current market price of A$0.735 per share, down 3.922% on October 22, 2019.

PRU Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...