Company Overview - Perseus Mining Ltd. (Perseus) is an Australia-based gold explorer, developer and producer. The Company focuses on under-explored gold belts in West Africa. Perseus produces approximately 200,000 ounces per annum from its Edikan Gold Mine (EGM) in Ghana, in gold production and has 5.3 million ounces (Moz) of measured and indicated gold resources, including reserves of 2.7Moz gold, and 2.36Moz Inferred gold resources. A further 1.4Moz of Indicated gold resources, including 0.66Moz of Reserves, and 0.52Moz of Inferred gold resources are held in other West African projects, Grumesa in Ghana and Tengrela in Cote d’Ivoire. Perseus’s other principal asset includes the Sissingue Gold Project located in Cote d’Ivoire. The Company comprises the following main segments: Australia, investing activities and corporate management; Ghana Mining, mineral exploration, evaluation and development activities; and Cote d’Ivoire Mineral exploration, evaluation and development activities.

Analysis - The company is focused on gold exploration, development and production in West Africa and currently produces 200 koz of gold annually at an AISC of less than USD 1000 per ounce under the guidance of its experienced and capable board of directors and managers. As of 31 March 2015, it was free of debt with cash and bullion on hand of $ 84 million and net working capital of $ 149 million. Its hedges amounted to 70koz at a price of USD 1514 per ounce.

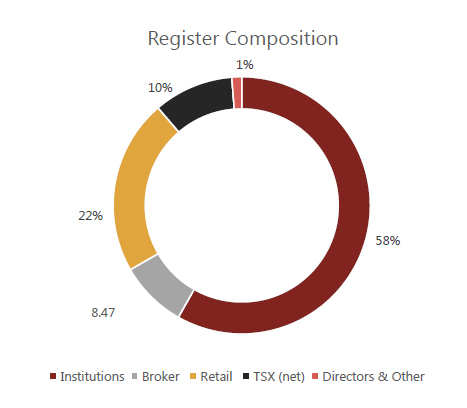

There were 526.6 6 million outstanding ordinary shares million and 534.6 4 million shares on a fully diluted basis with a market capitalisation of around $ 180 million. The share ownership pattern is 40% in Australia, another 40% in the US and Canada, 17% in Europe and 3% in Asia. The shareholding is dominated by high quality institutional ownership with the top 20 investors holding around 46% of the issued capital.

Company Register Composition (Source - Company Reports)

2015 March quarter activities report

Company Register Composition (Source - Company Reports)

2015 March quarter activities report

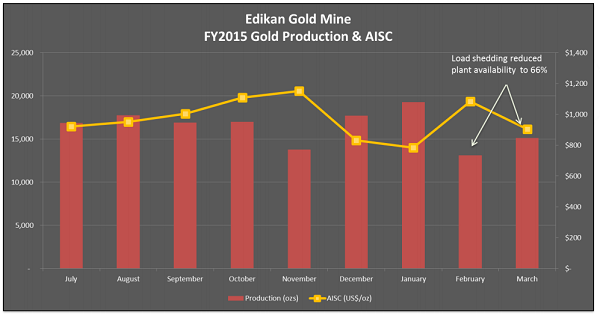

Edikan Gold mine Ghana reported strong performance during the quarter and the highlights included gold production of 47,450ozs which was only 2% lower than the December 2014 quarter, despite power restrictions imposed by the government during the quarter.All-in site costs of US$903/oz, were approximately 11% lower than in the December 2014 quarter and 25% lower than the mid-point of cost guidance for the June 2015 Half Year. Gold sales of 48,936ozs at an average sales price of US$1,375/oz resulted in a positive cash margin averaging US$472/oz. An important initiative implemented during this quarter that will benefit Edikan in the future is the acquisition of four diesel generators that can produce up to 5.8MW of electricity to address the current power shortage. Edikan able to draw full power load by 23April 2015. Other initiatives include the finalisation of the Eastern Pits mining contract at mining rateswhich, along with those contracted in the December 2014 quarter for mining the Fobinso Pit, will result in a substantial reduction of unit mining costs and the reoptimisation of Edikan’s Life of Mine Plan (“LOMP”) to deliver annual gold production of about 240kozs at a weighted average all in site cost of US$937/oz for the remaining 8 year life from 1 July 2015.

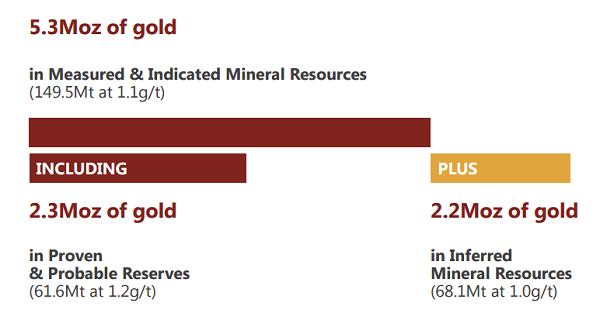

Edikan Mineral Resources & Reserves (Source - Company Reports)

Edikan Mineral Resources & Reserves (Source - Company Reports)

During the quarter mining occurred in Stages 2 and 3 of the AG pit, as well as in Stage 3 of the Fobinso pit, both of which are located on the western side of the Edikan mining leases, adjacent to the processing plant. A total of 1,346,539bcm of ore and waste was mined which is almost 13% less than in the December 2014 quarter. The reduction is consistent with the Company’s mine plan. Ore mined during the water included 1,658,147 tonnes of primary ore grading 1.26g/t gold. Ore movements were 4% down on the previous quarter while the grade of ore mined was approximately 18A% higher than in the prior quarter, as a higher grade ore zone was accessed towards the bottom of the AG pit.

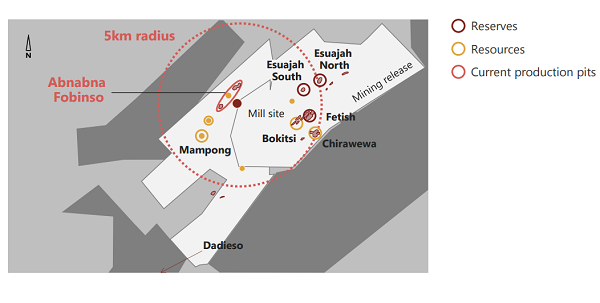

Edikan Deposits (Source - Company Reports)

Edikan Deposits (Source - Company Reports)

During the quarter, tenders received during the preceding quarter for the mining of the Eastern Pits (including Fetish, Bokitsi and Chirawewa pits) were assessed and negotiations were conducted with a short list of the three lowest bidders. By the end of the quarter, all substantive terms of a contract to perform the specified work had been agreed with African Mining Services (Ghana) Limited (“AMS”), the mining contractor that has been employed by Edikan since mining started in 2011. Subsequent to the end of the quarter, all outstanding contractual matters have been resolved and a binding Agreement between AMS and the company has been executed. The prices for the provision of the mining services under the Eastern Pits contract are lower than the rates that apply to AMS’ current mining activities in the AG Pit and should result in substantially lower unit mining costs.

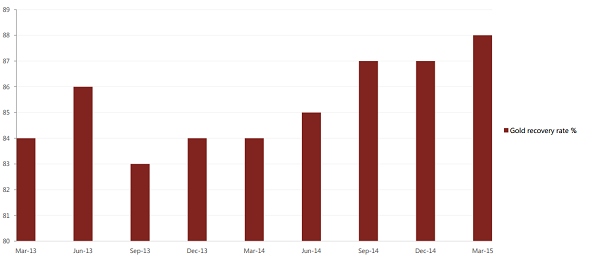

Gold Recovery Rate (Source - Company Reports)

Gold Recovery Rate (Source - Company Reports)

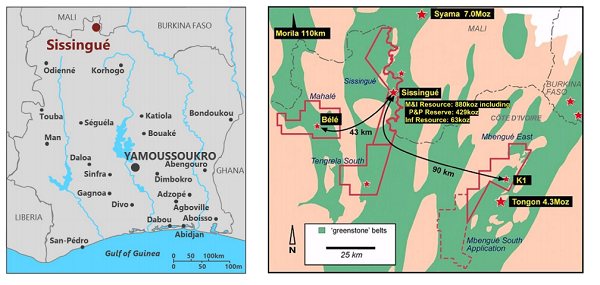

A positive feasibility study was completed for the development of Sissingué Gold Mine, Côte D’ivoire whichforecasts that Sissingué is technically viable and economically robust at a gold price of US$1,200/oz. After the end of the quarter, the company has decided to proceed with the development of Sissingué. Work has commenced on arranging financing including a modest amount of third party debt to supplement existing cash reserves.

Sissingué Gold Mine Development Project (Source - Company Reports)

Sissingué Gold Mine Development Project (Source - Company Reports)

At 31 March 2015, working capital of $148.8M included available cash and bullion of $83.7M (excluding $12.3M in escrow), an increase of $25.9M during the quarter. Gold forward sales contracts included 9,500ozs of gold sold forward at an average price of US$1,514/oz, valued at $29.7M (US$22.8M); and there was no third party debt other than accounts payable in the normal course of business.

Projects in West Africa

There were several achievements in 2014 in Edllkan. The working capital increased from $ 99 million-$ 121 million and the project remained debt free. There was an improvement in productivity and a significant decrease in all in site costs. The actively managed revenue line ensures that better than average gold prices were realised and a substantial amount of outstanding VAT was recovered from the government of Ghana. The quality of mineral resources was improved because of drilling at different sites.

Operating Performance (Source - Company Reports)

Operating Performance (Source - Company Reports)

The mineral resources and reserves amounted to 5.3Moz of gold in measured and indicated mineral resources (149.5 MT at 1.1 g/t). This included 2.3Moz of gold in proven and probable reserves (61.6 MT at 1.2 g/t) and 2.2 Moz of gold in inferred mineral resources (68.1 MT at 1.0 g/t) The company has also released its revised production and cost guidance for FY 2015. Gold production in ounces is expected to be between 100,000 and 110,000 for the half-year to June 2015 and 200,000 to 210,000 for the financial year 2015 compared to 100,000 for the half-year to December 31, 2014. All in site costs in USD/oz are expected to be between 1150 and 1250 for the June 2015 half-year and between 1075 and 1175 for the financial year 2015 compared to 988 for the half-year to 31 December 2014. The increase from the previous guidance is because of the increased investment in the stripping of Fobinso Stage 3 Pit. Reduced mining costs have made this investment economically viable and should result in production of a further 130,000ozs.

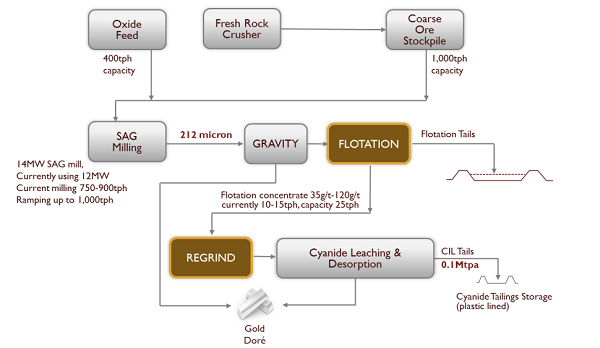

Edikan Processing Plant Flow Chart (Source - Company Reports)

Edikan Processing Plant Flow Chart (Source - Company Reports)

Sissingue Mineral Resources and Reserves amount to measured and indicated mineral resources of 880Koz of gold (15.8 MT at 1.7 g/t) which includes 429 Koz of gold in proven and probable reserves (5.5 MT at 2.4 g/t) and 63 Koz of gold in inferred mineral resources (1.1 MT at 1.7 g/t).

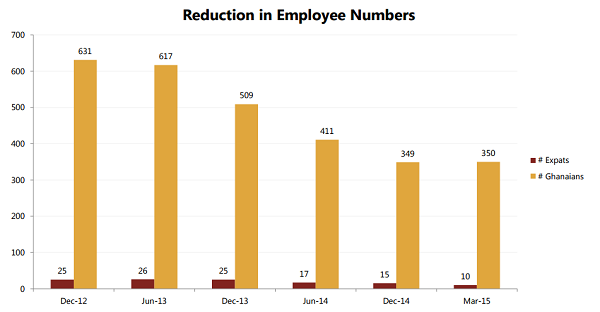

Reduction in Employee Numbers (Source - Company Reports)

The group currently has total ore reserves of 67.1 MT which at a grading of 1.3 g/t contains 2.8Moz of gold. From 2017 onwards, average gold production is expected to be 315,000 ounces annually at an average weighted all in site cost of USD 864 per ounce for the five years following. The group aims to continue producing gold from multiple sites located in West Africa and will continue to look out for opportunities both internal and external to maximise shareholder value.In the latest development, the company has announced that the Ghanaian Environmental Protection Agency has approved the Company’s Supplementary Environmental Impact Statement for its Edikan Gold Mine in Ghana, The approval allows Perseus to extend its mining operations to include mining of the Fetish, Bokitsi, Chirawewa (collectively referred to as the “Eastern Pits”) and Esuajah North gold deposits.

PRU Daily Chart (Source - Company Reports)

PRU Daily Chart (Source - Company Reports)

Perseus has been mining and producing approximately 200,000 ounces of gold per year from the Abnabna and Fobinso open pits on the western side of its mining lease since operations commenced at Edikan in late 2011. Clearing work and preliminary waste stripping activities in the Eastern Pits area will now commence and significant quantities of ore will start to be mined in the September quarter of 2015.

We believe that the company has created a platform for future growth and that their initiatives for productivity improvement are already generating tangible results. Their efforts at producing higher grade mill feed augurs well for future profitability. The continued focus on West Africa means that Sissingue will provide the opportunity to enhance production at low incremental risk while providing an opportunity to further reduce all in site costs. We put a buy recommendation on PRU at the current price of $0.41.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...