Kalkine has a fully transformed New Avatar.

Company Overview: Pendal Group Limited, formerly BT Investment Management Limited, is engaged in the provision of investment management services. The Company operates through two segments: investment management business in Australia (BTIM Australia) and investment management business outside of Australia (BTIM UK). The Company operates in the funds management markets in the world, including the United States, the United Kingdom, Asia, Europe and Australia. The Company offers investment services in Australian equities, global equities, property, ethical, income and fixed interest and diversified strategies. Its Australian equities include a range of funds, such as BT Core Australian Share Fund, BT Focus Australian Share Fund, BT MicroCap Opportunities Fund, BT Smaller Companies Fund and BT MidCaps Fund. J O Hambro Capital Management (JOHCM), which operates as a boutique investment management business with offices in London, Singapore, New York and Boston specializing in the active management of equities.

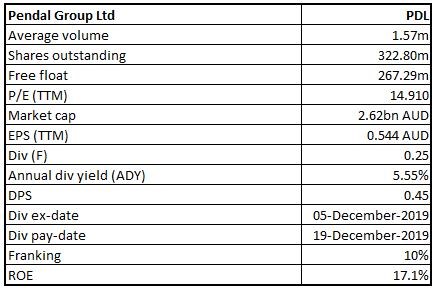

PDL Details

Robust Business Model: Pendal Group Limited (ASX: PDL) is an independent, global investment management business, which has its primary focus on providing high investment returns to its clients by active management. It is one of Australia’s leading investment managers with market capitalisation of around $2.62 billion as on November 25, 2019. As at September 30, 2019, the company reported for $100.4 billion in funds under management. The company’s core business model is an active investment in equities on behalf of their clients and diversification is the company’s key strength. The company’s diversification out of Australia and into Europe, the UK, Asia and the US allows it to intelligently manage the volatility that certainly is a feature of every market. Through the cycles, the company remains true to label and make disciplined and methodical decisions that deliver long-term value and growth to its clients and, thus, to its shareholders. The company has been delivering decent returns to its shareholders. The company has declared a final dividend of 25 cents per share, bringing the whole year dividend to 45 cents per share. Since listing of the company, the total shareholders’ returns stand at 188%, which is well above the 67% of the S&P’s ASX 200 Accumulation Index over the same period. The company’s zero debt balance sheet provides strength to its business. The company has no debt with a seed portfolio that supports growth initiatives and diversification of revenue streams. The company’s seed investment increased by $21.5 million to $259 million over the year, largely due to the improved market performance and a lower Australian dollar. The seed portfolio has grown significantly in the past three years as new strategies and vehicles are launched.

Moving forward, there are expectations that decent liquidity levels, zero debt levels, investment strategies, financial strength and robust cash flow are expected to act as tailwinds for long-term growth. Since the company has managed to declare a respectable amount of dividends despite a challenging period, it can be said that PDL has been focusing on delivering returns to its shareholders. .png)

Dividend Trend (Source: Company Reports)

Top 10 Shareholders: The following table provides an idea of the top 10 shareholders in Pendal Group Limited:.png)

Top 10 Shareholders (Source: Thomson Reuters)

FUM Figure as at September 30, 2019: The company’s Funds Under Management (FUM) closed at $100.4 billion. The FUM experienced net outflows of $4.7 billion due to geopolitical uncertainty and market volatility, which were buffered by higher markets and investment performance of $2 billion and favourable foreign currency movements of $1.5 billion. The institutional channel net inflows (+$1.5 billion) remained strong during the year, particularly in cash and fixed income asset classes. The higher margin wholesale channel saw net outflows of $3.6 billion, particularly in the Open-ended Investment Companies (OEICs) as they were affected by Brexit uncertainty and negative investor sentiment towards European equities. On the contrary, the US pooled funds generated net flows of +$0.7 billion, mainly in international and emerging market strategies, while the Australian wholesale channel flows were flat..png)

FUM Update (Source: Company Reports)

Financial Performance of the Company: The total fee revenue was down by 12 per cent to $491.3 million due to significantly lower performance fees which declined 89 per cent, from $54.5 million in the prior year to $5.9 million and lower base management fees which declined by 4 per cent. Average FUM over the year remained resilient and was down by 1 per cent to $98.8 billion. Strong institutional net inflows into cash and fixed interest strategies affected base fee margins, which were 2 basis points lower at 49 basis points.

The total operating expenses were down by 8 per cent to $290.2 million, mainly due to lower variable expenses. Variable employee costs fell, reflecting employee variable reward linked to lower revenue and non-staff variable costs were lower due to a decline in third-party manager fees. The fixed cost base increased 5 per cent, mainly because of the addition of 26 FTE over the year, which included operational staff in the UK office and eight staff in Australia after moving to full ownership of Regnan..png)

Financial Performance (Source: Company Reports)

Key Margins Above Industry Median: The company has improved its gross margins from 98.9% in FY18 to 99.6% in FY19, which states that the company has reduced its cost of goods sold. Its RoE stood at 17.1% in FY19, which is above the industry median of 6.2%, which means that the company is delivering decent returns to its shareholders.

Also, the company’s current ratio stood at 1.48x in FY 2019, which is higher as compared to FY 2018 figure of 1.46x and, therefore, it can be said that PDL has improved its capability to meet its short-term obligations. Also, a decent liquidity base can also help the overall company to make deployments towards strategic growth activities..png)

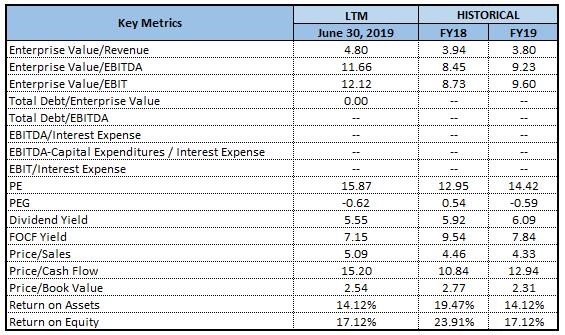

Key Metrics (Source: Thomson Reuters)

Purchasing Program for Pendal Group Employee Equity Plans: The company has announced that it has authorised the Trustee of its Group Employee Equity Plans to purchase PDL Shares up to a value of $38.1 million to help in delivering its share requirements for the next 12 months.It is anticipated that shares would be acquired off-market from the employees whose shares have been released from the restriction under the plans.

Company Appoints JOHCM CEO- the UK, Europe and Asia: The company announced that it has appointed Alexandra Altinger as the CEO of the JOHCM (J O Hambro Capital Management)operations in the UK, Europe and Asia. Alexander Altinger is appointed to support growth in offshore markets as she has cross border experience and expertise in wealth and asset management. Her passion for investment management and broad experience across multiple markets would be invaluable in contributing to growth of the business. She recently spent four years as the CEO of Sandaire Investment Office, a UK multi-family office offering tailored investment portfolios and solutions for families and foundations.

What to Expect from PDL, Moving Forward: Despite the current difficult year, the company remains confident on a strategy of attracting, retaining and developing superior investment talent, and expanding its distribution and investment capabilities to meet clients’ needs. The company’s financial strength and strong cash flow keep it in a good position to invest for growth and take advantage of opportunities.

The company will continue to identify new investment strategies and teams that can materially grow FUM. It would be focusing on developing extension strategies that can provide further investment capabilities. From the perspective of fund flow, the company witnessed outflows in its European and UK strategies, and the sentiments were impacted by the ongoing uncertainty around Brexit. The appointment of the new CEO for JOHCM business and her dedicated attention and focus will enable the company to anticipate and react to changes in the market and capture growth opportunities.

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

Method 1: EV/EBITDA Multiple Approach:.png)

EV/EBITDA Multiple Valuation (Source: Thomson Reuters)

Method 2: Price to Earnings Multiple Approach:.png)

Price to Earnings Multiple Approach (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The company added that the appointment of the regional CEOs having significant industry experience for JOHCM business was important to the future growth strategy. The attention as well as focus that the dedicated CEOs bring to each of the region would better enable the company to anticipate and react to changes in the market and tap the growth opportunities. During 2019, the company has moved to full ownership of Regnan, a leading ESG research, engagement and advisory business. This will support PDL’s objectives to improve investor outcomes through a continued focus on stewardship.

Considering the company’s zero debt balance sheet and decent liquidity footing, we are affirmative on PDL’s expected performance and there are expectations that the company might witness respectable growth moving forward. Also, higher RoE as compared to the broader industry median can help it gaining traction among market participants. Considering the aforesaid facts and decent outlook of the business, we have valued the stock by using two relative valuation methods, i.e., EV/Sales and P/E multiples, and arrived at the target price of high single-digit to low double-digit (in % terms). Hence, we give a “Buy” rating on the stock at the current price of A$8.180 per share (up 0.863% on 25 November 2019).(1).png)

PDL Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...