Kalkine has a fully transformed New Avatar.

Company Overview: Pendal Group Limited, formerly BT Investment Management Limited, is engaged in the provision of investment management services. The Company operates through two segments: investment management business in Australia (BTIM Australia) and investment management business outside of Australia (BTIM UK). The Company operates in the funds management markets in the world, including the United States, the United Kingdom, Asia, Europe and Australia. The Company offers investment services in Australian equities, global equities, property, ethical, income and fixed interest and diversified strategies. Its Australian equities include a range of funds, such as BT Core Australian Share Fund, BT Focus Australian Share Fund, BT MicroCap Opportunities Fund, BT Smaller Companies Fund and BT MidCaps Fund. J O Hambro Capital Management (JOHCM), which operates as a boutique investment management business with offices in London, Singapore, New York and Boston specializing in the active management of equities.

.png)

PDL Details

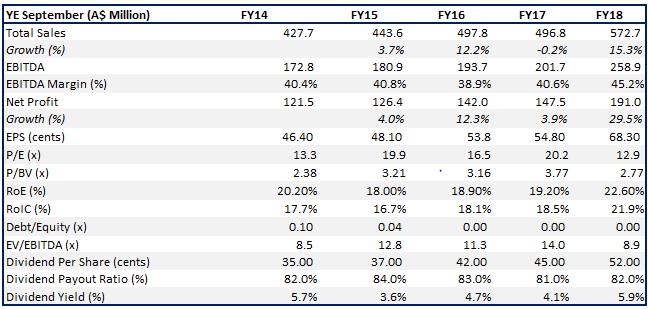

Movement of PDL’s FUM and Other Key Metrics: Pendal Group Limited (ASX: PDL) is a global asset management group that has demonstrated to sail through difficult market conditions as seen in the last one year and has been looked upon in view of the prevailing multi-year low levels of the stock. The company’s fundamental and quant analysis indicates that the financial ratios and other parameters still look decent despite the headwinds noted for the asset management profile. Having the capability to maintain a better net margin in comparison to industry, decent funds under management scenario and growth profile as the market has now more or less relatively stabilised speak about the capability of the group at a broader level.

The company recently released the results for 1H FY 2019 in which its cash net profit after tax amounted to $84.5 million, which implies a fall of 26% as compared to the previous corresponding period while the company’s statutory net profit after tax stood at $69.6 million, implying a fall of 37%. Amidst the uncertainties in the global markets, the company managed to declare an interim dividend amounting to 20 cents per share for 2019 financial year, which would be 10% franked and would be paid on June 26, 2019 to the ordinary shareholders. It was having a record date of May 24, 2019. However, the dividend reinvestment plan happens to be deactivated for FY 2019 interim dividend.

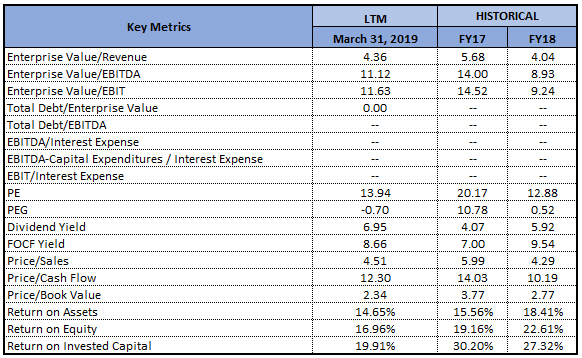

The company added that the result was mainly weighed by the significantly lower performance fees which were down 91% and stood at $4.4 million as compared to $47.6 million in pcp. The company’s base management fee revenue in 1H FY 2019 witnessed a fall of 4% and stood at $237.6 million because of 1% decline in the average funds under management (or FUM) as well as a contraction in the base management fee margin which was down 2 bps and stood at 49 bps. The margin reduction was because of the change with respect to the asset mix as investors moved out of equities and into the more defensive and lower-margin cash and fixed income products. Also, FUM ended at $100.9 billion which is reflecting a fall of $0.7 billion for 1H FY 2019 because of the lower market levels and partially offset by lower Australian Dollar while net flows were flat for the same period. At the current market price of A$7.240, the stock of the company is trading at 12.35x of FY20E EPS.

Moving forward, the company’s performance is expected to be sensitive to geopolitical conditions and other macro-economic factors. However, robust balance sheet with no debt and decent cashflow are expected to be the tailwinds for long-term growth. The key focus of market players needs to be on the company’s commitments toward expanding the investment and distribution capabilities. Seeking the long-term potential in the business along with healthy balance sheet position with nil debt and paying regular dividends to its shareholders, we have valued the stock using Relative valuation method, Price to Book Value multiple and five-year average P/E multiple of 15.0x for FY20E with consensus EPS of around $0.586 and have arrived at a target price upside in the range of $8.4 to $8.7 (double-digit upside (in %)).

Key Metrics (Source: Company Reports, Thomson Reuters)

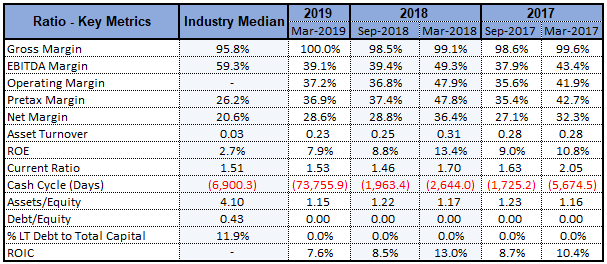

PDL Possessing Decent Position in Key Margins: Pendal Group Limited is having a decent position in its key margins as its net margin stood at 28.6% in 1H FY 2019, which is higher than the broader industry median of 20.6% that reflects the company is having better capabilities to convert its top line into bottom line as compared to concerned industry. Additionally, the company is having a current ratio of 1.53x, which is marginally higher than the industry median of 1.51x that reflects the company is in a better position to meet its short-term obligations and is having sufficient headroom to make further deployments towards the growth prospects.

Key Metrics (Source: Thomson Reuters)

The company’s Assets/Equity ratio stood at 1.15x, which is lower than the industry average of 4.10x and, thus, it looks like that the company is largely financing its assets mainly with the help of equity. However, its ROIC or (Return on invested capital) for 1H FY 2019 stood at 7.6%.

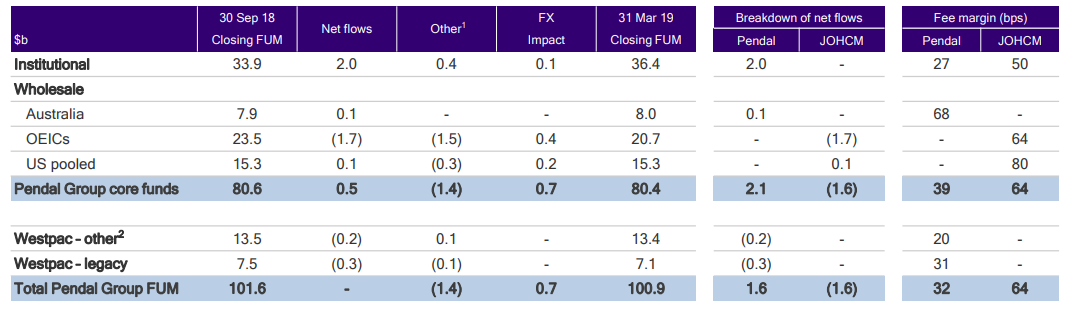

Understanding PDL’s Funds Under Management in Detail: Pendal Group’s FUM had witnessed robust net inflows in Australian business during 1H FY 2019, while the Brexit uncertainty impacted the flows in UK/European OEICs. The company’s closing FUM as at 31 March 2019 stood at $100.9 billion, which represents a 1% decrease on $101.6 billion as at 30 September 2018. It was affected by the significant negative market movements in the quarter ended December. The company had witnessed net outflows amounting to $1.7 billion in OEICs, which were predominantly led by net outflows in the European equities amounting to $1.2 billion. The economic momentum in Europe had been slow and together with the uncertainty with respect to Brexit has led to the reduced appetite for risk from the investors.

1H FY 2019 FUM and Flows (Source: Company Reports)

The company added that robust net flows were witnessed into cash (+$0.9 billion), fixed income (+$0.8 billion) as well as Australian equities (+$0.2 billion), while the Asian equities had witnessed net outflows amounting to $0.5 billion. During 1H FY 2019, the average levels of S&P/ASX 300 Price Index as well as the MSCI All Countries World Index in local currency terms were lower by 1.2% and 2.7%, respectively as compared to the same period of the last year. The company mentioned that the average level of the Australian Dollar was 3.4% lower relative to British Pound, and 8.0% lower than the US Dollar over the same period.

Light on Some Critical Events: During the month of April 2019, Westpac Group had redeemed $1.5 billion from its legacy book as part of its consolidation of superannuation offerings. The effective management fee margin on withdrawal happens to be around 31 basis points as well as predominantly from the multi-asset FUM. Also, in the month of April 2019, new arrangements were entered into for the use of J O Hambro Trademark for the 7 years term to October 26, 2025 with annual fee payable amounting to £150,000 (or $279,000) for first 4 years, and an annual fee payable amounting to £250,000 (or $465,000) for remaining three years.

Broader Overview of Strategic Highlights: Pendal Group had stated that even though it witnessed outflows across the European as well as Asian equity strategies, there were good institutional inflows into the Australian equities, cash and fixed income strategies. There was an expansion of the US distribution footprint by establishing the presence on the West Coast. However, strategic highlights also include the launching of Concentrated Global Share strategy through UCITS vehicle in Europe and moving to full ownership of Regnan. The recognised expertise of Regnan together with the Pendal’s heritage in ESG space, positions PDL well when it comes to expanding in this growing segment of the market as leading stewards of capital and offers the opportunity to leverage the capability globally.

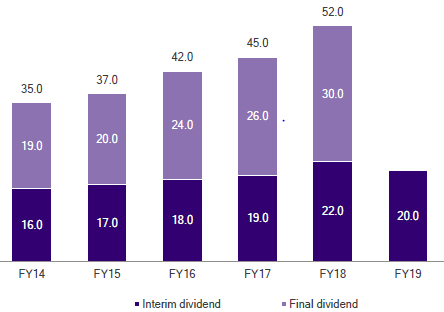

Amidst Uncertainties, PDL Declared Interim Dividend: The balance sheet of Pendal Group happens to be strong and it has no debt. The company has decent cash flows in the business which might attract the attention of the market players and this also makes the company well-positioned to make deployments which could be long-term growth catalysts. The company’s Board had declared an interim dividend amounting to 20.0 cents per share for 2019 financial year despite the uncertainties in the equity markets and, thus, it could be said that the company had been focusing towards enhancing the shareholder value. The dividend declared is representing a 1H FY 2019 payout ratio of 75% and the Board is having a policy of shelling out 80%-90% of the full year cash NPAT which can be considered at respectable levels. The company stated that the Dividend Reinvestment Plan remains deactivated for FY 2019 interim dividend.

Dividend Trend (Source: Company Reports)

The annual dividend yield of the company is about 4.8% on a five-year average basis (FY14-18). As per ASX, the company is having an annual dividend yield of 6.95%, which is higher than the industry median of 5.1%, showing a better option for dividend investors. This might attract the attention of market players moving forward. As can be seen from the above picture, the company had been declaring respectable interim dividends in the past and, between 1H FY 2015 to 1H FY 2019, it had witnessed a CAGR growth of approximately 4%.

What To Expect From PDL: The key personnel of Pendal Group had stated that 1H FY 2019 was challenging for the markets as well as investors. They added that the market returns in the quarter ended December were worst on record since September 2011 quarter, and even though there was a rebound in market returns in March quarter, the volatility over the half had resulted in a significant increase in the risk aversion from clients. The resolution to the US/China trade talks as well as clarity over Brexit might lead to the improvement in the investor confidence.

Amidst more difficult trading conditions, the company added that its robust balance sheet along with no debt and good cash flow reflects that the company is in a sound position to reap the advantages of the opportunities to expand the capabilities as well as a global presence. The company is focused on expanding the investment and distribution capabilities, maintaining the disciplined approach towards managing the capacity as well as providing support to the investment talent through investment-led culture and business model. The company is expected to report full-year results on November 06, 2019.

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology:

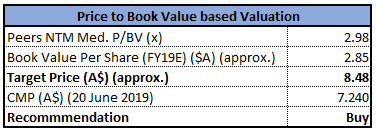

Price to Book Value based Valuation:

Price to Book Value based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

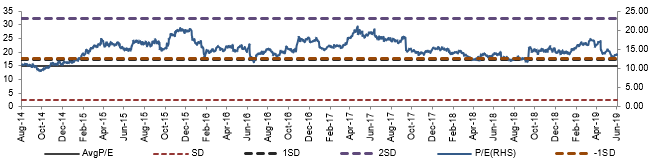

Historical P/E Band (Source: Company Reports, Thomson Reuters)

Stock Recommendation: The stock of Pendal Group Limited had witnessed a fall of 8.87% in the span of previous one month while, in the time frame of six months, it had fallen -7.35%.It can be assumed that these decreases had led to the stock trading towards its 52-week lower levels and, thus, it looks like the major negatives have been factored in the stock price. As a result, the stock’s current trading level offers a reasonable opportunity to make an entry.

With respect to FUM and flows, the company witnessed robust inflows into cash, fixed income, and Australian equities and there had been positive global/international flows. Coming to the investment performance, the company stated that 69% of the FUM had outperformed over the span of 3 years and 89% of FUM had outperformed over the five years. Also, significant institutional flows were directed into cash and fixed income.

Also, as stated above, the company’s annual dividend yield (as per ASX) is higher than the broader industry median which can be considered a positive point for the dividend-seeking investors. Considering the above-stated factors and current trading juncture, we are affirmative on the stock and expect that, if the global economic conditions and equity markets stabilize, it might positively impact the overall performance of Pendal Group. Hence, by looking at the long-term potential in the business along with a healthy balance sheet position with nil debt and paying regular dividends to its shareholders, we have valued the stock using Relative valuation method, Price-to-Book Value multiple and five-year average P/E multiple of 15.0x for FY20E with consensus EPS of around $0.586 and have arrived at a target price upside in the range of $8.4 to $8.7 (double-digit upside (in %)). Based on the foregoing, we give a “Buy” recommendation on the stock at the current market price of $7.240 (up 0.695% on 20 June 2019).

.png)

PDL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...