Company Overview - Peet Limited is an Australia-based company engaged in developing and marketing residential land. The Company operates through the following segments: funds management, company-owned projects, joint ventures, and inter-segment transfers and other unallocated. Through the funds management segment, external equity capital raisings are undertaken to fund the acquisition of land across Australia. The Company-owned projects segment includes purchase and development of various parcels of land in Australia, for residential purposes. Within the Joint ventures segment, joint ventures are formed with Government, statutory authorities and private landowners. The joint venture partner contributes the land and the Consolidated Entity funds the development costs. Inter-segment eliminations and other unallocated segment comprises revenue, expenses and results, which include transfers between segments.

.png)

PPC Details

Oversubscribed Peet Syndicate: Peet Ltd’s (ASX: PPC) recent retail land syndicate, the Peet Werribee Land Syndicate (wherein PPC has 17% investment) was closed early, as the $25 million offer was oversubscribed. Investors of this syndicate consist of 25% of new investors and about 50% of the funds raised, excluding Peet’s investment, were from east coast-based investors. Meanwhile, the Peet Werribee Land Syndicate would develop or market a community of more than 900 residential lots, on nearly 86 hectares of land in the western growth corridor of Melbourne.

The construction of the project was expected to start in the month of June 2016. PPC already closed issue of Series 1, Tranche 1 Peet Bonds to raise nearly $75 million by issuing 750,000 Bonds with a Face Value of $100 each. On the other side, PPC had sold Greenvale project for $ 93.1m in August 2015 and got only first installment of $28 m out of the three installments, while the other two are yet to be received.

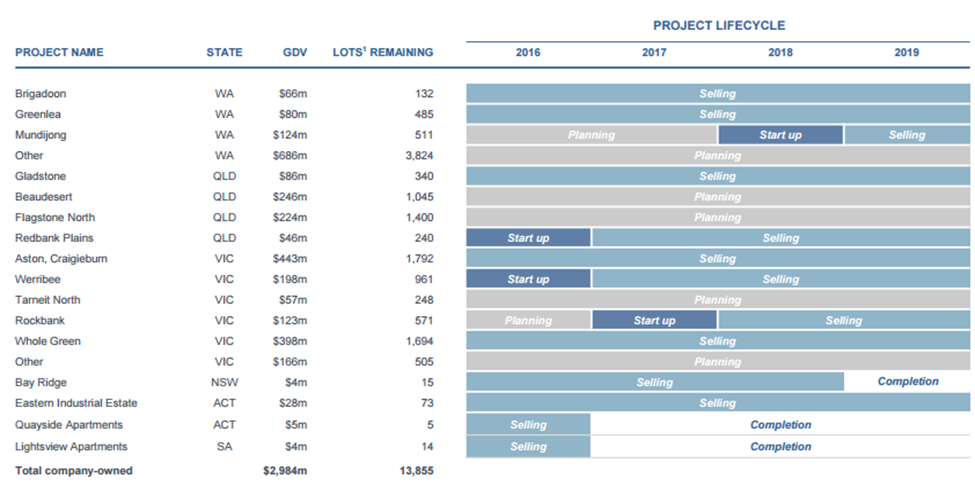

Built solid pipeline indicating a clear earnings visibility: PPC has a projects pipeline of about 48,000 lots, assuring a solid earnings visibility to the group for the next two years. The group has around 12 new projects which are forecasted to start development in the next 2-3 years. Out of these 12 new projects, over 8 new projects would start with their development or sales activities from fiscal year of 2016. PPC has over 79% of the lots in these 12 projects which are under its Funds Management business. Funds Management business accounts over 34% of Group EBITDA for the first half of 2016. The new projects comprise over 40% of current pipeline and has the average project duration of 7 years offering better visibility of future cash flows. Management reported that over 80% of entire new projects’ land bank is forecasted to be in development by end of FY17. Accordingly, the group is balancing its new Land portfolio across key growth corridors to build a diversified assets base. As a result, Peet is focusing on east coast projects, whose Contribution rose to 76% of Peet’s EBITDA for the first half of 2016. Major contribution of this EBITDA rise was from Victoria.

The group further acquired 1,700 lot Whole Green (VIC) project in this region which is expected to contribute to the group’s performance from 2H16. The second project acquired in the region is Redbank Plains (QLD). Meanwhile, management reported that the East coast EBITDA contributions would offset the ongoing pressure at WA and NT.

.png)

Business model (Source: Company Reports)

Residential development highlights: PPC has entered into a conditional agreement for the proposed residential development of up to 3,300 residences on land owned by the University of Canberra in Belconnen, ACT. The gross development value of this project is currently expected to be circa $1.7 billion and the project is expected to be constructed in 15 years to 20 years’ period. Meanwhile, PPC through its subsidiary CIC Australia Pty Ltd has partnered with South Australian State Government for the redevelopment of the residential section of Tonsley. This development would lead to over 780 construction jobs for nine years and deliver over $265 million in housing investment. On the other side, PPC earlier undertook the multibillion project for Flagstone City Development which would consist of 12,000 homes and 126ha commercial centers with the joint venture MTAA Super.

PPC is developing the first stage of this project which would consist of 33 home sites and first commercial lots and is expected to contribute to the 2H16 earnings. On the other side, the group had started three new projects in first half of 2016 which include Botanic Village (VIC) of 783 lots, Haven (VIC) of 300 lots and Hibert Park (WA) of 997 lots.

Land bank, Peet’s owned major projects (Source: Company Reports)

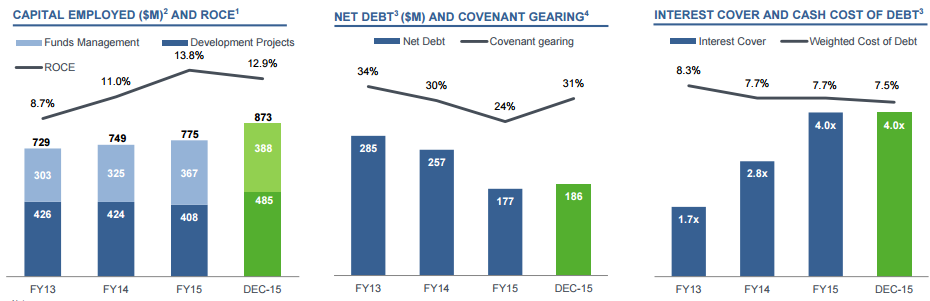

Expanded margins despite top line pressure: Peet’s revenues fell over 26% to $136.7 million in the first half of 2016 as compared to the same period of last year, as the group’s lot settlements fell 12% on a yoy basis. Accordingly, the group’s EBITDA dropped over 12% yoy to $40.3 million during the period as Quayside apartments (ACT) project and The Chimes project (WA) were finished. On the other hand, the group’s EBITDA margin enhanced to 29% in the first half of 2016 as compared to 25% in the same period of last year driven by the better than estimated rise from VIC and ACT/NSW projects. The group intends to deliver further cost-outs from WA operations. Hence, PPC was able to maintain the EPS of 3.8 cents during the period, on track with the first half of 2015.

The group generated a return on capital at 13%. However, market adjusted NTA per share fell to $1.14 in the first half of 2016 as compared to $1.17 in the same period of last year. The joint ventures contract on hand during the period was down by 9% to 607 lots with the total value of $158m due to the soft market conditions in NT.

First half of 2016 performance (Source: Company Reports)

Decrease in gearing: The group has a strong cash and equivalent assets of $99 million as of first half of 2016. PPC’s overall bank debt was steady at $186 million with a weighted average cash cost of bank debt (excluding convertible notes) declining to 6.3%, The group estimates its weighted average cash cost of bank debt to fall to 5.9% based on hedge profile for fiscal year of 2017.

However, covenant gearing rose to 30.6% in the first half of 2016 due to acquisition of Whole Green project, Tarneit (VIC). But, the group expected its gearing to fall back within its target range of 20-30% by June 2016. The company recently confirmed maturation of its convertible notes (with 489,980,559 fully paid ordinary shares) which have been repaid in full.

Balance sheet highlights (Source: Company Reports)

Stock Performance: The shares of PPC stock have fallen over 12.3% during this year to date (as of July 01, 2016) as the group delivered softness in top line for the first half of 2016 impacted by the tough market conditions. On the other hand, PPC has a strong land bank in the mainland states and territories, and continues to add new projects. In addition, PPC built outstanding contracts on hand of 2,318 lots as of first half of 2016 which is an increase of 12% since June 30, 2015. The value of these contracts has increased 19% to $523 million. Moreover, the contracts on hand for developments segment has increased over 70% to 416 lots of worth $96 million in the first half 2016, despite the top line pressure for the division. The contracts on hand under the Funds under Management division rose by 13% to 1,295 lots of worth $269 million during the period, as compared to the prior corresponding period. Peet is also diversifying its earnings base, to decrease its reliance on the challenging Western Australia and Northern Territory markets.

We believe that the recent correction in the stock also placed PPC at attractive levels which has a decent dividend yield and is trading at a reasonable P/E. Recently, UBS Group AG and its related bodies corporate became substantial holder with 5.11% as voting power. We believe investors need to leverage the correction in the stock as a buying opportunity. Based on the foregoing, we give a “BUY” recommendation on the stock at the current price of $0.905

PPC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...