Overview: Paradigm Biopharmaceuticals Limited (ASX: PAR) is a biopharmaceutical company dedicated on repurposing the drug pentosan polysulfate sodium (PPS) for the therapy of infection. The Company has initiated the open labelled Phase II clinical trial, investigating the role of the drug PPS in treating traumatic Bone Marrow Lesions. The Company concentrates on repurposing PPS under ZILOSUL name, as a treatment for bone marrow edema (BME) lesions in the wake of painful damage.

.png)

PAR Details.png)

Strong Liquidity Position & Higher Investment are Key Growth Catalysts: A biopharmaceutical company, Paradigm Biopharmaceuticals Limited (ASX: PAR) is involved in the research and development of therapeutic products. The company deals in drug repurposing and finds new uses for old drugs which improve in decreasing the cost and time to bring therapeutics to market. PAR was listed on ASX in 2015. The company’s top clinical indications comprise treating bone marrow edema (BME), and the treatment of joint function, mobility and pain in patients with mucopolysaccharidoses (MPS).

The company had reported on positive secondary endpoints of its successful phase 2b randomised double-blind placebo-controlled multi-centre clinical trial, treating participants who are having knee osteoarthritis (OA) and concurrent bone marrow lesions (BML) with injectable Pentosan Polysulfate Sodium (iPPS). The company is now preparing for a crucial Phase 3 clinical trial, which will be conducted in the USA, EU, and Australia. There is a worldwide propensity for reliable and efficient pain relief for chronic diseases such as osteoarthritis, which is non-opioid and non-steroid. The demand for such services offers a massive market prospect for Paradigm’s iPPS.

The company recently started dosing all the ten patients with Zilosul, after receiving approval of FDA approved Expanded Access Program (EAP) in the US. The company reported a very promising real-world information ahead of its phase 3 osteoarthritis (OA) clinical trial utilising the Phase 3 product and two Phase 3 endpoints. OA patients were treated with injectable pentosan polysulfate (iPPS) (Zilosul®) under the Special Access Scheme (SAS) of Therapeutic Goods Administration (TGA). PAR was delighted to report a mean reduction of ~45% in WOMAC pain subscale of the OA index of WOMAC across 34 patients using the product and endpoints with knee osteoarthritis.

PAR has also effectively completed $35M placement and accepted a solid support from the leading institutional investors both domestic as well as international. The financing will aid the company to mainly focus on implementing the clinical trials and provide outcomes for patients in the growing market.

The company’s net cash from operating activities amounted to $529K in the quarter ended 31st March 2020 and it has also incurred $2.4 million towards research and development. Following the completion of the Capital Raising program, the company will be in a strong liquidity position, with >$107 million cash. Notably, the company will be fully funded for the completion of the Phase 3 trial, which is likely to begin at the end of 2022.

Going forward, the company’s robust liquidity position and decent revenue-generation capabilities will be a key catalyst. Additionally, PAR’s revenue includes other income, which has been increasing over the past few years. This might attract the attention of market players. The company believes to ride on several key catalysts such as increasing data from patients using TGA SAS, reduced WOMAC pain from baseline and improved Patient Global Impression of Change (PGIC) at week 8 (Day 53). On the other hand, Paradigm’s MPS 1 Phase 2 clinical trial in Adelaide is expected to commence in Q3CY20. Further, PAR is well funded to carry out its second phase 3 osteoarthritis (OA) clinical trial.

Coming to the past four-years performance, covering FY15 to FY19, PAR witnessed a CAGR of ~358.7% in its income. This reflects that PAR can make deployments towards its business activities which might help it in tapping long-term growth prospects.

.png)

Sneak Peek at Income (Source: Company Reports)

1HFY20 Financial Highlights for the year ending 31 December 2019: PAR declared its interim results wherein, the company reported revenues from continuing activities of ~$602.3K, up from $574.2K in the year-ago period. The company posted a loss of $5.1 million as compared to the previous gain of $703.7K in the prior corresponding period. Other income for the period stood at $825.9K as compared to $28K in 1HFY19. Research and development expenses for the period came in at $4.3 million as compared to $3.2 million in 1HFY19.

.png)

1HFY20 Key Highlights (Source: Company Reports)

Improving Liquidity Position: The company reported $77.2 million of total current assets, including cash of $70.9 million and trade and other receivables at $3.3 million. Intangible assets were valued at $2.98 million while total equity stood at $79.3 million as on 31 December 2019. Net cash outflow from operating activities came in at $5.9 million while net cash outflow from investing activities was at $3.7 million.

Capital Raising- a Key Catalyst: The company made an announcement of successfully completing the Capital Raising program. The funds garnered under the offer are expected to finance osteoarthritis (OA) and mucopolysaccharidosis (MPS) programs through to the end of their respective pivotal phase 3 clinical trials, and the new drug applications. Also, the funds would be deployed towards working capital, costs of the offer, further preclinical studies, etc. Henceforth, the fund raising will further strengthen its liquidity position and makes it more effective to undertake business transactions which can prove to be beneficial over the long term.

Greater Than 40% Pain Reduction: PAR had reported ~44.9% reduction in the pain across 34 patients which are having knee osteoarthritis. Also, the company had stated that it had met the primary end point of safety which will be used in Phase 3 clinical trials in the participants who are having chronic Ross River virus (or RRV) induced arthralgia treated with the injectable pentosan polysulfate sodium. The pivotal two phase 3 studies will include 750 patients in the 1st phase 3 trial and 400 patients in 2nd Phase 3 trial.

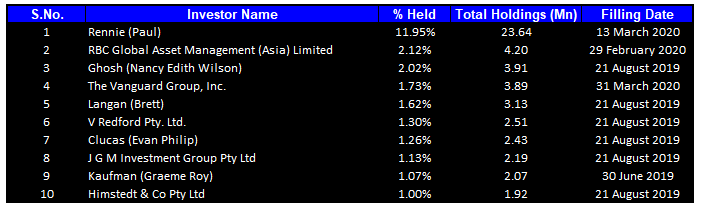

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 25.2% of the total shareholding. Rennie (Paul) is the entity holding maximum shares in the company at 11.95%. RBC Global Asset Management (Asia) Limited is the second-largest shareholder, with a holding of 2.12%.

Top Ten Shareholders (Source: Thomson Reuters)

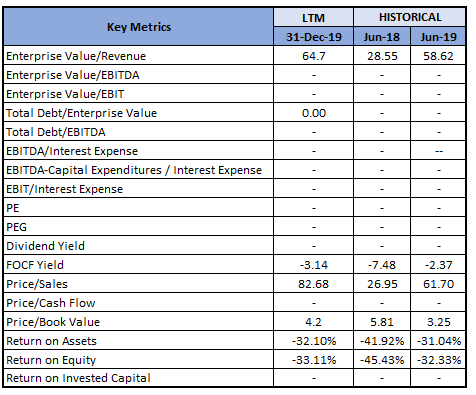

Key Metrics: In 1HFY20, the company had a current ratio of 66.64x, higher than the industry median of 3.16x, representing a sound liquidity position. Debt to Equity ratio for 1HFY20 stood at 0.01x, lower than the industry median of 0.26x. The company is optimistic about business growth, looking at the potential contribution and lower debt levels.

Key Metrics (Source: Thomson Reuters)

Outlook: With respect to the osteoarthritis market, the company stated that OA happens to be the most common form of joint disease. In the United States, it affects more than 33 million adults, while in Australia, arthritis affects more than 3 million people. In both countries, the condition acts as a leading cause of pain and disability among the elderly and the cause of life-years lost due to disability. In the US alone, the financial burden of OA has been projected to be ~$81 billion in medical costs and $128 billion in total cost per year. The demand for new effective treatment is amplified by the opioid epidemic throughout the US. The company’s capital raising initiatives, and its focus towards delivering on the pipeline of catalysts is a key positive. Moreover, the company has a long-standing relationship with commercial partners which will support growth momentum in years ahead.

The company also stated that the final patient under the EAP is scheduled to receive the final dosing of Zilosul® in May this year. Paradigm further expects initial feedback from the Joint Parallel Scientific Advice submission to both the FDA and EMA during the second quarter of CY20. Paradigm reported that the coronavirus pandemic is unlikely to have a material long term impact on the business. Subsequent to the completion of its capital raise, Paradigm has reported a strong cash position that is likely to fully fund the company through to the completion of its phase 3 trials.

Key Valuation Metrics (Source: Thomson Reuters)

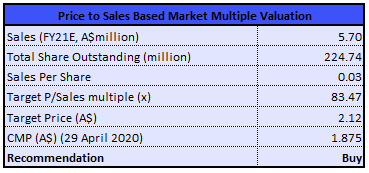

Valuation Methodology: P/S Market-Multiple Based Valuation Method (Illustrative)

P/S Market-Multiple Based Valuation Method (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters

Stock Recommendation: The stock of the company is currently trading below the average of its 52-week trading range of $1.080 - $4.5. The stock has a market capitalisation of ~$379.81 million. The stock has corrected by ~45.83% in the last six months and ran up 7.99% in the last one month. The company’s sound financial position would make it fully capitalised to execute on clinical development as well as the commercialisation strategy for OA and MPS. Looking at the long-term growth potential, we have valued the stock using a 1-year forward Price/Sales market multiple to FY21E consensus sales figure of $5.70 Mn and have arrived at a target price with an upside of lower double-digit (in % terms). Considering the current trading levels, strong liquidity position, no material impact of COVID-19, and positive outlook, we recommend a “Buy” rating on the stock at the current market price of $1.875, up by ~10.947% on 29 April 2020.

PAR Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...