Kalkine has a fully transformed New Avatar.

Company Overview: Paradigm Biopharmaceuticals Limited is a biopharmaceutical company focused on repurposing the drug pentosan polysulfate sodium (PPS) for the treatment of inflammation. The Company is engaged in researching and developing therapeutic products for human use. The Company is a drug repurposing company, which seeks to find new uses for old drugs. The Company has commenced the open labelled Phase II clinical trial, investigating the role of the drug PPS in treating traumatic Bone Marrow Lesions. The Company's Rhinosul has properties consisting of both histamine stabilizing and anti-inflammatory properties. The Company focuses on repurposing PPS under ZILOSUL name, as a treatment for bone marrow edema (BME) lesions following traumatic injury.

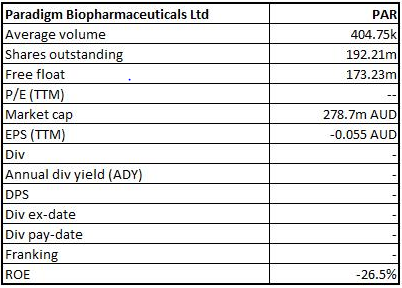

PAR Details

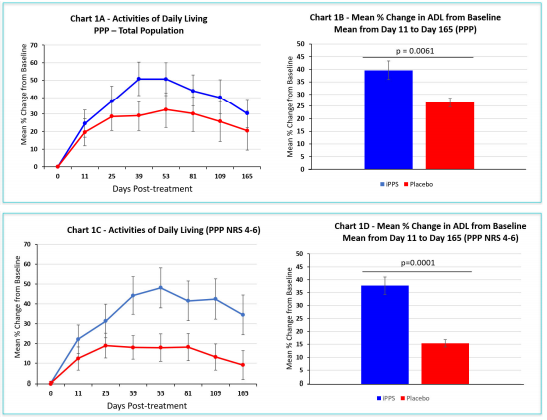

Overview of March Quarter Results: Paradigm Biopharmaceuticals Limited (ASX: PAR) is a small-cap Australian based biotechnology company with the market capitalisation of circa $278.7 Mn as of 4 June 2019. It is focused on repurposing a drug, namely Pentosan Polysulfate Sodium (iPPS) for the treatment of Osteoarthritis of the knee through subcutaneous injection. Pentosan Polysulfate Sodium (iPPS) is an FDA approved drug that has a long track record of safely treating inflammation. The company had reported on positive secondary endpoints of its successful phase 2b randomised double?blind placebo?controlled multi?centre clinical trial (n=112) treating participants which are having knee osteoarthritis (OA) and concurrent bone marrow lesions (BML) with injectable Pentosan Polysulfate Sodium (iPPS). The positive secondary end?points reported were the improved knee function (Activities of Daily Living or ADL) reflecting improved physical function to Day 165, reduction of pain to 6 months. This means that pain reducing effects of iPPS are durable over 6 month period. Adding to that, it was also mentioned that at 6 months (i.e., Day 165) the proportion of subjects receiving iPPS with more than 50% reduction in KOOS pain score happens to be clinically meaningful and statistically significant over placebo. The reduction of BML grade, size and volume on MRI reflects the potential of iPPS to slow progression of the disease. The objective data corroborates previously reported top?line?data that iPPS is safe and clinically effective (as measured by > Knee Osteoarthritis Outcome Score (KOOS) 10, percentage of subjects with >50% reduction in pain) and statistically significant improvement of Patient Global Impression of Change (or PGIC) (p=0.0062). The company’s net cash used in operating activities amounted to $1.94 million in the quarter ended March 2019 and it had also incurred $1.59 million towards research and development.

Moving forward, the company is expected to be helped by a strong liquidity position and decent revenue-generation capabilities. Also, the company’s revenue including other income has been improving from the past few years which might attract market players’ attention. We expect that there is a favourable outlook of the company at the back of several key catalysts such as filling of TGA Provisional Approval to sell ZILUSOL® (iPPS) in Australia, the first SAS filing with TGA for the treatment of MPS patients with iPPS, pre IND meetings with the FDA, and initiation of a compassionate use program in the US, etc. On the other hand, the planning for progress and partnering discussions of Phase 3 OA clinical trial have already started on the back of robust Phase 2b data package. And, the company is well funded to start its phase 3 clinical program in CY19.

Improved Knee Function (Activities of Daily Living) to Day 165 (Source: Company Reports)

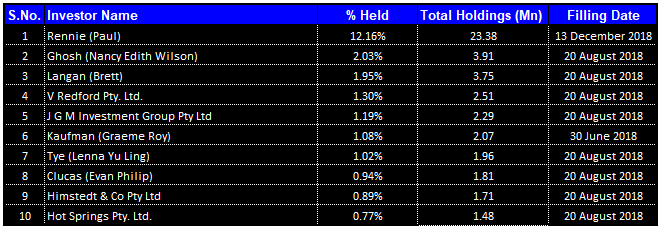

Top 10 Shareholders: The following table gives a broad picture of the shareholding pattern of Paradigm Biopharmaceuticals Limited:

Top 10 Shareholders (Source: Company Reports)

Improving Liquidity Position: Paradigm Biopharmaceuticals had witnessed an improvement in its key financial ratios in 1H FY 2019 on the YoY basis which reflects the decent performance of the operational capabilities. This also strengthens the confidence in the company’s core business activities.

From the liquidity point of view, the company stands firm as its current ratio stood at 9.20x in 1H FY 2019, which is higher than the industry median of 4.55x, reflecting its liquidity position to meet its short-term obligations. However, it also reflects that PAR can make deployments towards its business activities which might help it in tapping long-term growth prospects. PAR’s Assets/Equity ratio stood at 1.06x, which is lower than 1.53x and, therefore, it can be assumed that its assets are largely being funded by equity and it has lesser reliance on debt. As at 31 December 2018, the company enjoys debt-free status with cash and cash equivalent of $9.93 Mn.

.png)

Improving Liquidity Position (Source: Company Reports)

Placement and Entitlement Offer: Paradigm had made an announcement of $77.9 million capital raise, which comprises of the $51.6 million placement to the professional and sophisticated investors throughout Australia, Asia, the UK and the USA, including some of the existing shareholders, and $26.3 million underwritten institutional and retail entitlement offer. The funds garnered under offer are expected to finance osteoarthritis (OA) and mucopolysaccharidosis (MPS) programs through to the end of their respective pivotal phase 3 clinical trials, and the new drug applications. Also, the funds would be deployed towards working capital, costs of the offer, further preclinical studies, and further intellectual property acquisitions. Therefore, we expect that the fund raising will further strengthen its liquidity position and makes it more effective to undertake business transactions which can prove to be beneficial over the long period of time.

Material Reductions In Bone Marrow Lesions: Bone marrow lesions in subchondral bone of people with knee osteoarthritis are associated with the pain and progression of cartilage loss over time. As previously reported from Paradigm’s Phase 2b clinical trial, the group of patients that received injectable Pentosan Polysulfate (iPPS) had a clinically meaningful reduction in BML Grade which was also statistically significant over placebo (p=0.03). The company had reported that it is witnessing significant reductions in BML in sites of the body other than the knee using iPPS under TGA special access scheme. The sites where PAR had witnessed significant reduction in BML include hip, knee cap and ankle.

The company also stated that it had completed the manufacturing of iPPS in order to support expected upcoming requirements under Phase 3 OA and MPS trials and the requirements under TGA special access and FDA compassionate use. The key components of PAR’s upcoming IND filings with FDA are the completion of manufacturing as well as ownership of batch records.

Completion Of Retail Entitlement Offer: Paradigm had made an announcement that it had wrapped up the retail component of 1 for 8 accelerated non-renounceable entitlement offer which it had announced on April 15, 2019. The entitlement offer happens to be fully underwritten by Bell Potter Securities Limited. The retail entitlement offer got closed on May 6, 2019 which helped it in garnering around $16.5 million at $1.50 per Share. Together with the shares issued under the institutional component of the entitlement offer, the total amount garnered under entitlement offer (after meeting the Underwriter's commitments) would be around $26.3 million.

Greater Than 50% Pain Reduction: Paradigm Biopharmaceuticals had reported greater than 50% reduction in the pain across 205 patients which are having knee osteoarthritis. If we combine the results of 22 patients with the previously reported 183 patients, it brings an average reduction in the pain scores to 51.3% across the total of 205 patients. Also, the company had also stated that it had met the primary end point of safety in Pilot Phase 2a randomised, double-blinded placebo-controlled, multicentre clinical trial in the participants who are having chronic Ross River virus (or RRV) induced arthralgia treated with the injectable pentosan polysulfate sodium. The participants who are having RRV-induced arthralgia treated with iPPS met the aims for pilot Phase 2a study by demonstrating the safety outcomes and effects on reduced disease symptoms.

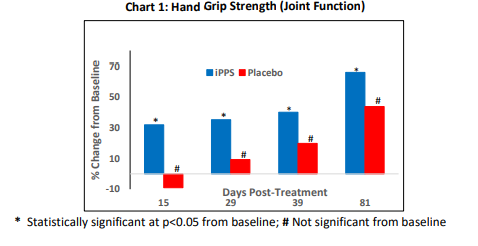

PAR’s aim was to demonstrate that iPPS was safe in the subjects with chronic and sustained RRV symptoms. Also, the aim of the clinical trial was to obtain signals of the efficacy of iPPS with respect to the alleviation of disease symptoms. As can be seen from below chart, in the subjects treated with PPS, the hand grip strength which measures maximum isometric strength of the hand and forearm muscles using handgrip dynamometer showed significant improvements from the baseline throughout the study from Day 15 to Day 81. There were significant differences from the baseline at all time points in iPPS-treated group: 32% at Day 15, 40% at Day 39 and 66% at Day 81.

Hand Grip Strength (Joint Function) (Source: Company Reports)

What To Expect From PAR Moving Forward: Earlier, Paradigm Biopharmaceuticals had made an announcement that they have wrapped up institutional component of the fully underwritten accelerated non-renounceable entitlement offer which was announced on April 15, 2019, garnering around $9.8 million. With respect to the osteoarthritis market, the company had stated that OA happens to be the common form of joint disease. In the United States, it affects more than 30 million adults, while in Australia, arthritis affects approximately 3 million people. In both countries, the condition act as a leading cause of pain and disability among the elderly and the cause of life?years lost due to disability. The demand for new effective treatment is amplified by the opioid epidemic throughout the US. The company had wrapped up the $77.9 million capital raising, and it is focused towards delivering on the pipeline of catalysts for the remainder of 2019. In Q2 CY 2019, the release of peer reviewed journal paper which details mechanism of action of PPS via Nerve Growth Factor (NGF) is expected and, during the same period, the first SAS filing with TGA for the treatment of MPS patients with iPPS is expected.

In Q2 CY 2019, the company is expected to file TGA Provisional Approval to sell ZILUSOL® (iPPS) in Australia which could act as a catalyst for the revenue in the near term. Moving forward, the company also anticipates to release Ross River Phase 2a (safety study) trial results. Moreover, the company has a longstanding relationship with commercial partners which will support growth momentum in years ahead.

.png)

Commercial Partners (Source: Company Reports)

Stock Recommendation: As stated in March 2019 quarterly report, Paradigm Biopharmaceuticals had witnessed a capital raising amounting to around $52 million institutional placement and approximately $26 million underwritten entitlement offer, helping the company with the cash position of >A$81 million upon the completion of entitlement offer component. This would make PAR fully capitalised to execute on clinical development as well as commercialisation strategy for OA and MPS.

On the other hand, the company is having lower Assets/Equity ratio for 1H FY 2019 in comparison to the industry median which might attract the attention of market players moving forward. However, in the span of previous three months, the stock has delivered the return of 24.77% while, in the time frame of one month, it delivered a return of -6.75% which reflects that the stock is quite volatile. Based on the foregoing and considering decent outlook backed by key catalysts which are lined up for the remainder of 2019 along with current trading level, we give a “Speculative Buy” recommendation on the stock at the current market price of A$1.475 per share (up 1.724% on 4 June 2019).

PAR Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...