Company Overview – PanAust is a copper and gold miner with operations in Southeast Asia and undeveloped deposits in South America and Papua New Guinea. It’s Phu Kham copper-gold mine in Laos started in 2008 and produces more than 60,000 tonnes of copper and 55000 ounces of gold a year. Reserve life is 10 years with unit production costs of around USD 1 to 2 per pound of copper after gold credits. The Ban Houayxai gold-silver mine is located 25 kilometres west of Phu Kham and started in 2012.

Analysis – Following an impressive Q4 of production in Laos, PNA has reported CY13 attributable profit of US$36.4m, down from US$142m in CY12. PNA incurred an impairment of US$50.9m on some of its exploration assets resulted in the lower than expected CY13 Net Profit After Tax. PNA declared a A$0.03/share dividend payable in April, bringing the total to A$0.06/share for the year. Sales were in line with expectation with 62.6kt copper in concentrate sold and 184.4koz of gold. Earnings Before Interests Tax, Depreciation and Amortisation (EBITDA) was in line with the PNA guidance but lower year on year due to higher mill rates at both mines and lower realized pay metal prices. Profitability was primarily affected by the US$50.9m impairment charge and to lesser extent due to lower commodity prices.

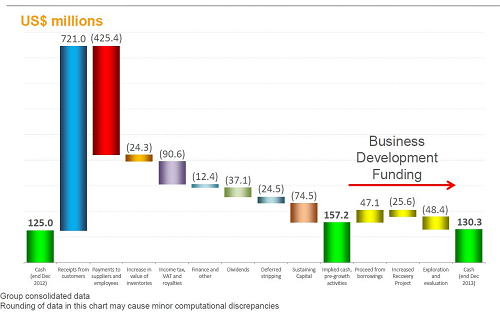

Operating Cash Flow + Development Capital Program (Source – Company Reports)

Operating Cash Flow + Development Capital Program (Source – Company Reports)

At Phu Kham, 65-70kt of copper is expected at slightly higher costs year on year as peak Life of Mine (LOM) material movements are moved in the open pit and the strip ratio increases to 1.7:1 versus 1.0:1 in CY13. Higher anticipated treatment charge/refining charge and scheduled lower grades will also impact costs. At Ban Houayxai 100koz gold is scheduled on 4.8mt milled. Regionally the KTL scoping study is underway evaluating the trucking option to Phu Kham and is planned for release in the March quarter. PNA will progress the KTL deposit by trucking high grade ore to Phu Kham for processing rather than developing the stand alone Phonsavan Copper Gold project which was being studied. The decision to abandon the standalone option resulted in the impairment of study related costs of $27m. A plan to develop a road suitable to haul ore on between KTL and Phu Kham is required before the company can progress the project. The extended Inca de Oro feasibility study is ongoing. The JV partners are set to review the results from drilling at the Carmen deposit. The study is assessing the potential to add both oxide and sulphide ore to the existing resource base and the subsequent impact on the project economics. The JV has reportedly identified a potential power source at competitive prices and water solution. The study is also assessing the scale of the project with processing rates ranging from 9-18 Mt/a. Early indications point to smaller high grade approach with improved operating costs.

Ban Houayxai Gold – Silver Operation Process Plant (Source – Company Reports)

Ban Houayxai Gold – Silver Operation Process Plant (Source – Company Reports)

Revenue has increased for PNA year on year despite the weaker metal prices as production increased especially for gold and silver. Development capital decreased by $109m in 2013 to $26m. Exploration capex declined $20m year on year to $48m. Sustaining capex was $75m in 2013. All approved capital programs have been completed. No development capital is expected in 2014. The exploration spend will fall further from 2014 from $48m to $28m. Sustaining capital will be lower in 2014 as spending on the Phu Kham Tailings Storage Facility (TSF) decreases. 2014 sustaining capex is forecast to drop to $35m. Gold sales increased 40% year on year as production at both Phu Kham and Ban Houayxai increased. A full year contribution of the Increased Recovery Project is expected to lift Phu Kham copper output to 65-70 kt in 2014, despite lower heads grades. A recovery in mined head grade from 2015 will deliver further copper production growth with the potential to reach 90kt/a in 2018.

.png) Phu Kham Copper Gold Operation in Laos (Source – Company Reports)

Phu Kham Copper Gold Operation in Laos (Source – Company Reports)

Strong sales in CY13 saw net cash build of only US$5m. Sustaining capex was high at US$74.5m, of which US$27.1m was spent on stages of construction of the TSF’s at both Phu Kham and Ban Houayxai. PNA expects sustaining capex to halve to US$35m in CY14 as reduced construction requirements are anticipated at the PHU Kham TSF. Exploration and evaluation outflows of US$48.4m are expected to reduce to US$28m in CY14 as feasibility work at Inca de Oro should wind up, resource drilling at the Carmen deposit continues and the KTL project progresses. PNA also paid US$37.1m in dividends in CY13.

Ban Houayxai Gold – Silver Operation (Source – company Reports)

Ban Houayxai Gold – Silver Operation (Source – company Reports)

PNA reported its 2014 Reserves and Resources estimates with changes year over year from the addition of the KTL reserves and depletion at Phu Kham and Ban Houayxai. The 2014 Phu Kham reserve incorporates the KTL deposit with 8.0mt at 1.06% copper, 0.66g/t gold and 3.5g/t silver. The total Phu Kham Ore Reserve is 165mt at 0.52% copper, 0.25g/t gold and 2.0g/t silver. Ban Houayxai ore reserves are mostly unchanged after mining depletion as lower revenue assumptions are offset by lower unit operating cost assumptions.

PNA Daily Chart (Source – Thomson Reuters)

PNA Daily Chart (Source – Thomson Reuters)

PNA remains our top pick in base metals for its leverage to copper, robust operating margins and rising free cash flow. PNA’s free cash flow grew to A$40m in the FY13, up from $18m a year earlier. The company expects free cash flow to more than double again this year with the free cash flow guidance of A$100m. We view this guidance as reasonable considering PNA does not have any development capex planned for 2014. Operating expenditure at Phu Kham is likely to remain little changed in 2014 with strip ratio remaining elevated. While PNA’s gold operation, Ban Houayxai is also expected to remain at the lower end of the cost curve. PNA has reaffirmed previous discussion that the KTL deposit is likely to be developed as a satellite deposit, contributing to the mill feed at Phu Kham from 2016-2021 via a smaller scale trucking operation. We will be putting a BUY on the stock at the current price of $1.55.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Please wait processing your request...

Please wait processing your request...