Company Overview: OZ Minerals Limited is a mining company with a focus on copper. The Company's principal activities are the mining of copper, gold and silver, carrying out exploration activities and development of mining projects. The Company's segments are Prominent Hill, which is engaged in mining copper, gold and silver from Prominent Hill Mine, a combined open pit and underground mine located in the Gawler Craton of South Australia; Carrapateena, which is engaged in exploration and evaluation activities associated with Carrapateena project located in South Australia; Exploration & Development, which is engaged in exploration and evaluation activities associated with other projects and includes interests in Jamaica and Chile, and joint ventures with Minotaur Exploration and Toro Energy Ltd., and Corporate Development activities, and Corporate, which is engaged in other corporate activities, including Consolidated Entity's Group Office, other investments in equity securities and cash balances.

.png)

OZL Details

Cloncurry Regional Alliance with Minotaur- Support Growth Momentum: OZ Minerals Limited (ASX: OZL) has an engagement in the mining and processing of ore containing copper, gold, and silver; sales of concentrate; exploration activities; and the development of mining projects. As on May 29, 2019, the market capitalisation of OZL stood at ~$3.02 billion. OZL entered into a strategic alliance with Minotaur Exploration Limited (ASX: MEP, Minotaur) over the Cloncurry region of northwest Queensland. This significant development is complementary to Minotaur’s recent announcement concerning OZ Minerals’ additional expenditure commitment for the Eloise Joint Venture between the parties. The Cloncurry Alliance is said to be established through 70% OZ Minerals and 30% Minotaur; and, and is indicated to enable the parties to work exclusively with each other for prospect identification and acquisition around the Cloncurry district.

In another development between OZL and MEP, OZL’s beneficial interest in the Eloise Joint Venture (Contains Jericho copper deposits) reached 70% on 31 March 2019 through project investment of A$10 million over 3 years. From that point onwards, Minotaur Exploration Limited (ASX MEP) was to co-contribute its 30% share of Eloise JV expenditure. Contemporaneously with OZ Minerals’ and Minotaur’s creation of the new Jericho Joint Venture, the parties have agreed to restructure the existing Eloise JV.

OZ Minerals with its partnership with Minotaur is expected to help the company in better utilization of their capacities and expertise in prospect identification, exploration, and development. Despite certain and uncertain challenges such as climate change/extreme weather events disrupting mining production, logistics, water supply, and power outages at the site and unexpected fluctuations in the commodity prices, OZL expects decent FY19 production guidance for both copper and gold. Its revenue for FY18 increased by 9.2% to $1,117 Mn, and profit after tax attributable to shareholders decreased by 3.8% to $222.4 Mn in FY18.

.png)

FY18 P&L Statement (Source: Company Reports)

Key Ratios: Its EBITDA margin and net margin for FY18 stand at 40.0% and 19.9%, which are better than the industry median of 29.5% and 14.0% respectively, indicating decent fundamentals of the company. Its current ratio for FY18 stands at 5.08x which is better than the industry median of 1.67x, implying a better liquidity position of the company to address its short-term obligations than its peer group.

.png)

Key Ratios (Source: Thomson Reuters)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 32.35% of the total shareholdings. BlackRock Investment Management (UK) Ltd. and Dimensional Fund Advisors, L.P. hold maximum interest in the company at 7.30% and 6.59%, respectively. The Company recently announced a change in the director’s interest where Rebecca J. McGrath acquired 4,900 ordinary shares at a value of $9.21 per share, taking the final holdings to 42,835 ordinary shares effective from May 21, 2019.

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Strong operating cashflow expected to drive future growth of OZL: OZ Minerals highlighted that a strong operating performance from Prominent Hill enabled investment in their growth strategy and delivery of a net profit after tax of $222 million in FY18 which is in-line over the previous year. The underlying EBITDA was $540 million at a robust 48 per cent margin. A strong operating cashflow of $450 million represented company’s cash balance of $505 million after investing in the Carrapateena project, the Avanco Resources acquisition, exploration activities, and dividend payments. The Board of Directors declared a fully franked dividend of 23 cents per share as compared to 20 cents per share in the

prior year, showing 15% growth on PCP basis. Earnings per share stood at 71.5 cents.

.png)

OZL’s Growing Pipeline Overview (Source: Company Reports)

The two main areas of growth spending were the construction of the Carrapateena Copper Gold mine in South Australia approximately 160 km north of Port Augusta; and the purchase of Avanco Resources Limited, an Australian company with several advanced development projects in Brazil and a small operating mine. This ~$400 million purchase was a 50:50 mix of cash and scrip.

.png)

Work-In-Progress at Carrapateena (Source: Company Reports)

The Avanco acquisition also added to OZL’s exploration pipeline in the highly prospective Carajas and Gurupi Provinces of Brazil. Many of its exploration pipelines take the form of farm-in arrangements with experienced explorers giving it access to a number of targeted areas at a relatively low cost and from which it can exit quickly if a project does not meet its expectations.

A healthy exploration pipeline provides future growth options for the Company, most of which have not yet been factored into the Company’s valuations by the investment market. These include projects such as West Musgrave and the Carrapateena block cave expansion, which are expected to create potential future upside for the company.

FY18 Production & Financial Highlights: Revenue for the period was reported at $93.9 Mn higher than the prior year. It was majorly driven by higher commodity prices, consistent production from Prominent Hill and revenue from Antas. The amount of contained copper sold (114,722 tonnes) was 2% higher than in 2017, while gold sales of 131,929 oz were comparable to 2017 sales. In 2018, the average copper price was 8% higher than in 2017, while the average gold price was 3% higher.

As per realisation costs, treatment charges and refining costs were $13 Mn lower as a result of improved trading terms and lower refining charges in the market. The production costs in 2018 stood at $57.2 Mn which is higher than the prior year, with inclusion of Antas in the second half of the year, an increased proportion of underground ore and higher power costs at the Prominent Hill. Mining costs including inventory movement and net realisable value adjustments were $30.5 Mn higher than the prior year. Exploration and evaluation expenditure of $67.2 Mn was incurred during the year.

.png)

NPAT (FY18 vs. FY17) (Source: Company Reports)

Q1FY19 Financial Highlights: Total production for Copper and Gold for Q1FY19 stands at 27,442 tonnes and 34,648 oz, respectively. The C1 Cash Costs and All-in-Sustaining Costs for Q1FY19 stand at 60.7 US cents/lb and 103.9 US cents/lb, respectively.

.png)

Q1FY19 Production Metrics (Source: Company Reports)

The cash balance reduced to $342 million at 31 March after payment of the 2018 final fully franked dividend of $48 million and cash investment into the Carrapateena project of $116 million ($128 million of capital expenditure).

.png)

Cash Utilization Q1FY19 (Source: Company Reports)

Working capital increased by $50 million as a result of increased trade receivables of $49 million (timing of shipments late in Q1); increased concentrate inventory of $30 million (concentrate to be shipped in Q2); decreased trade payables of $10 million (timing of payments); and decreased ore inventory of $39 million (stockpile processing).

There was a Q1 net ore inventory drawdown resulting in a non-cash ore inventory movement of $39 million. The cash balance will continue to reduce through 2019 with ongoing growth capital expenditure, primarily in relation to the Carrapateena project. Ore inventory will also continue to deplete as open pit stockpiles supplement underground ore feed, maintaining the plant at full capacity to mid-2023.

.png)

Q1FY19 Working Capital Change (Source: Company Reports)

What to Expect: As per the release, for FY19, the copper and gold production are estimated to be 97kt-109kt and 118koz-131koz, respectively. C1 Cash Costs have been estimated at US 65c–75c/lb, and All-In Sustaining Costs have been estimated at US 110c–120c/lb. The guidance excludes production for Antas which will be released in Q2 2019 upon completion of the Mineral Resource and Ore Reserve update and revised mine plan.

Its priorities for 2019 include:

1. Strengthen and elevate its approach towards work safety,

2. Reliably and consistently deliver the Prominent Hill mine plan and consider ways to extend its life,

3. Safely deliver the Carrapateena project to schedule in Q4 2019 and progress the expansion study,

4. Optimise plans to develop its Brazilian assets,

5. Complete the West Musgrave pre-feasibility study, and

6. Continue to evolve its future growth pipeline.

.png)

Multiple Projects Pipeline (Source: Company Reports)

Copper Outlook: As per the release, the long-term returns on copper are more favourable as compared to other base metals. Copper is such a metal which enables future economic growth in a world that is going to be increasingly less carbon intensive. It has the ability to recycle - repeatedly and without any loss in performance which is an important sustainable benefit. Strong demand from the transport, renewable and infrastructure sectors concurrent with the expected end-of-life for some major global mines in the early to mid-2020s, result in a combination of supply and demand fundamentals that supports continued focus on copper.

Gold Outlook: The pressure across the global equities due to uncertainty across interest rate change by various central banks is turning the gold lustre bright and attracting investors to hedge the potential interest rate risk, which in turn is expected to support the gold prices. As per the media reports, China further expanded its gold reserves due to geopolitical tensions, especially the trade tensions between the US and China which could remain high in the coming times. Other countries such as Russia, and Turkey following the sanction concerns are looking for reducing dependencies on the US dollar by increasing bullion in their reserves. These developments have brought optimism among market participants and are expected to boost yellow metal prices in the coming times.

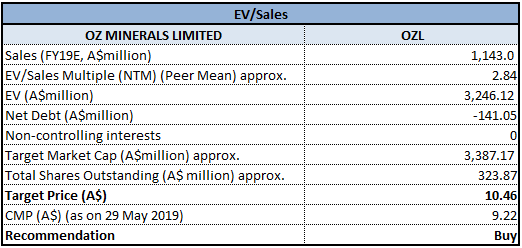

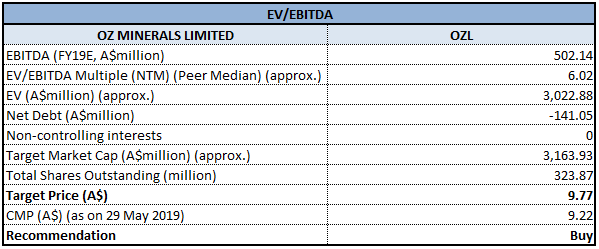

Valuation Methodology: As per few exemplary methods, below tables provide indicative upside potential for the stock.

Method 1- EV/Sales Multiple Approach (NTM):

EV/Sales Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

Method 2- EV/EBITDA Multiple Approach (NTM):

EV/EBITDA Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock of OZ Minerals Limited had delivered a decent return of 10.05% in the span of the previous six months while, on the YTD basis, the returns stood at 7.88%. In the FY19 guidance, the total copper and gold production levels are estimated to be 97kt-109kt and 118koz-131koz, respectively, which, more or less, equate to the four times of the current quarter. Moreover, the outlook for both the metals (Copper and Gold) looks bright which is expected to shift demand-supply ball game in the company’s favour and hence boost revenues in the coming years. Given the backdrop of a strong balance sheet, and decent top-line growth, the company’s future earnings look promising. Considering the aforesaid facts and decent outlook, we have valued the stock using two Relative valuation methods, EV/Sales and EV/EBITDA multiple and have arrived at target price upside in the range of $9.7 to $10.46 (single-digit upside (in %)). Hence, we give a “Buy” recommendation on the stock at the current market price of $9.220 per share (down 0.967% on May 29, 2019).

)(1).png)

OZL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...