Company Overview - OZ Minerals Limited (OZ Minerals) is an Australia-based modern mining company with a focus on copper. OZ Minerals owns the Prominent Hill copper-gold mine and Carrapateena copper-gold project, both situated in South Australia. The principal activities of the Company are mining of copper, gold and silver, carrying out exploration activities and development of mining projects. The Company operates the Prominent Hill Mine, a copper-gold mine located in the Gawler Craton of South Australia. The Prominent Hill Mine generates revenue from the sale of concentrate products containing copper, gold and silver to customers in Asia and Europe. Prominent Hill is comprised of the Malu open pit mine and the Ankata underground mine. The Carrapateena copper-gold project is an undeveloped copper deposit. The exploration and development activities are mainly in South Australia and include the Carrapateena project. Other activities include investment in Toro.

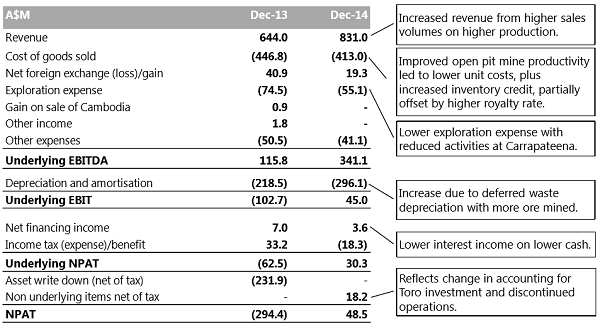

Analysis - Oz Minerals (OZL) recently highlighted its 2014 key commitments along with profit. The Company reported a revenue of $831.0 million while the underlying EBITDA was of the order of $341.1 million. The underlying NPAT was of the order of $30.3 million and statutory NPAT of the order of $48.5 million. The Company does not report of any debt while the cash was $218.5 million. OZL has an undrawn debt facility of US$200 million. All this resulted in a strong balance sheet for the Company. OZL also highlighted to relocate corporate functions to Adelaide in view of reorganising the corporate function while reducing costs and being closer to the strategic assets. There was also an announcement about Carrapateena initiatives with regards to infrastructure and processing technology. Further, the Company reported for strategic partnership with South Australian Government on technical and infrastructure projects. The business strategic review for augmenting cost base, bettering operating efficiency and exploring opportunities for business growth, is said to be completed by April. The Company did not declare any dividend with respect to 2014 in view of the strategic review which was said to be underway. The Company paid an interim dividend of 10 cents per share in September 2014.

Income Statement (Source – Company Reports)

The Company thrived in satisfying or surpassing its production targets. The positive news revolved around copper production run rate of 100,000 tonnes per annum while exceeding market guidance for copper production, gold production and costs. The drill results at Khamsin and Fremantle Doctor were quite promising which in a way established great prospective for the Carrapateena district to host further economic copper deposits. Release of the pre-feasibility study for the Carrapateena project indicating a project net present value of $1.1 billion have also been quite interesting. With regards to the Carrapateena copper assets, OZL started engaging with joint venture partners in 2014 for the development of the copper-gold project. However, partnering process has been now kept on hold in view of some recent decisions in order to reflect the true value of the Carrapateena assets. The Company could identify that the copper concentrate grade could be about doubled from 30-35% up to 55-60% given the finding of its initial concentrate treatment pilot plant tests conducted in 2014. The Company expects to have better revenues from the foregoing and better marketing terms along with about 40% reduction in freight costs per tonne of concentrate due to lower transported volumes. OZL will be commissioning a demonstration plant trial in 2015 to test the scalability in collaboration with few local and international research and technology providers and the South Australian Government. OZL intends to take this work at an existing, modified facility and expects this to entail a meaningfully longer continuous trial and a 30-fold increase in the volume tested compared to the pilot plant. South Australian government may aid in funding a portion of the cost ($18 million) associated with the demonstration plant trial.

Then OZL will be able reduce capital development costs by transporting ore to the existing production facilities at Prominent Hill through its infrastructure partnership with the South Australian Government. As per the Company’s rail Infrastructure study, enormous benefits from the development of new rail infrastructure to transport Carrapateena ore to the existing high quality processing plant at Prominent Hill have been identified. Pre-feasibility study supporting this aspect has been commenced and is expected to be completed during 2015. OZL will also consider evaluation of third party build/own/operate financing of the rail in order to work around reducing the upfront capital required to develop Carrapateena. The Company also expects a material fall in the strip ratio at Prominent Hill over the next few years. This would also help in cash flow generation. OZL expects uranium grades to increase at Prominent Hill with the deepening of the open pit which puts up a challenge to some extent.

Underlying NPAT (Source – Company Reports)

Accordingly, the Company has suspended its data room and the partnering process until the completion of the above initiatives. Owing to the discovery of the Khamsin resource and few early intersections at Fremantle Doctor, the exploration program around Carrapateena has been reported to be suspended till the completion of current three drill-hole program. All of this bringing a mix of positives and negatives for Carrapateena. Further, OZL is supposedly making efforts to deal with the challenges associated with uranium at Prominent Hill and Carrapateena. For instance, commissioning of a second Jameson Cell to reduce the entrainment of uranium-bearing minerals into the concentrate is one such effort.

Prominent Hill_Performance (Source – Company Reports)

The commencement of ore production at the new Malu Underground mine was as per the schedule. Particularly, development of the Malu Underground mine was progressed with ore production from stopes achieved in the fourth quarter as expected. The Company indicated that full production rates from this asset are likely to be achieved by Q4 2015. The production linked to higher sales resulted in an overwhelming revenue increase of 29% irrespective of the lower US dollar prices for copper and gold. The increase in revenue thus contributed to the profit with statutory NPAT.

Cash Flow (Source – Company Reports)

Quite lately, the Company also announced for agreeing the terms for the sale of its 19.1% stake in Sandfire Resources Limited. It has also been reported that the sale price has been $4.20/share, which represents a 1.75% discount to the last market price prior to Sandfire being placed into a trading halt. OZL has indicated gross proceeds of about $125 million. Further to the announcement made on 13 March 2015, the Company has finally concluded the transaction selling its shares in Sandfire. OZL announced for the potential sell down of equity holdings as part of its strategic review (due for completion in April 2015). OZL has further stated that this effort represents a cash gain of $2.5 million (unaudited) with regards to the investments made and the dividends emanating from Sandfire. There may be an accounting loss on the transaction based on the mark to market valuation at 31 December 2014. The details of the results are expected to be out as at 30 June 2015.

OZL Daily Chart (Source - Thomson Reuters)

No dividend and the stake sell down may look to be OZL’s strategy to conserve cash. It is expected that the stock will trade in line with the market given the awaited direction of the business, and commentary on Prominent Hill production and plans for near-term growth. With a few hiccups at Carrapateena, we still feel that the asset could have marginally higher yield than Prominent Hill with a superior 20-plus years of life. The Company has leverage to copper which is a key metal for the Chinese and Indian economies. With a little turbulent path but strong balance sheet with a return to profit and debt free position, we still have our likings for this stock. Of course, we need to wait and watch for the forthcoming updates.

Based on the above, we reinstate a BUY recommendation for this stock at the current price of $3.80.

.png)

.png)

.png)

Please wait processing your request...

Please wait processing your request...