Full-year results for FY 31 March, 2015

The highlights of the results included an increase of 24% in operating income to $ 90.1 million over the previous year, 22% in pro forma EBITDA to $ 34.5 million and an EPS of 10.11 cents per share up 18% over the previous year. The fully franked final dividend amounted to 3.58 cents per share making a total of 7.08 cents per share for the full year. The strong underlying business is reflected in the operational metrics, strong balance sheet and cash flow conversion and is the result of continued investment in core operations as well as underlying dividend.

.png) Financial + Operational Metrics (Source - Company Reports)

Financial + Operational Metrics (Source - Company Reports)

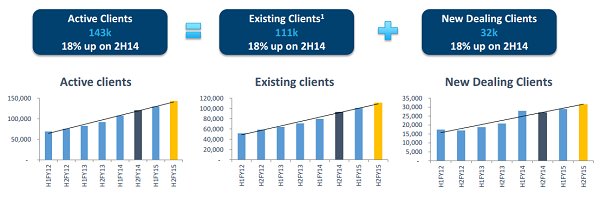

Active Clients increased by 18% over FY14 to 142,500 and Existing Clients increased by 25% on FY14 while New Dealing Clients grew by 11% to almost 61,000. Transactions increased by 21% over the previous year to touch almost 703,000 and three Average Transaction Value was slightly up on the FY14 average at $23,700.

Active Clients (Source - Company Reports)

Active Clients (Source - Company Reports)

The outgoing CEO, Mr Neil Helm, said the Group was in a good position to accelerate growth in the retail and wholesale sectors as well as to take advantage of acquisition opportunities if they should arise. “We have established a highly successful and market leading position in the international payments sector as a result of our scalable technology platform and attractive customer proposition. We have helped over 142,000 customers make international payments this year. Customers are attracted to our business for a combination of reasons including competitive pricing, ease of use and the outstanding customer service.”

Net Operating Income (Source - Company Reports)

Net Operating Income (Source - Company Reports)

During FY15 the Group completed its brand strategy review, reached the midpoint of the digital transformation program and obtained positive outcomes from all regulatory examinations conducted in a number of jurisdictions. The Group also received additional US money transmitter licenses increasing the US license portfolio to 47 states, established a corporate dealing team in Auckland NZ and saw an increase in activated OzForex Travel cards by 70% to just over 20,000. The company continued to invest in the core operations and business development with a focus on brand, marketing, the wholesale business and staff specifically in the risk and IT areas.

.png) Fee & Commission income from clients (Source - Company Reports)

Fee & Commission income from clients (Source - Company Reports)

As for the future outlook the company believes that international payment services is a large and growing market driven by increases in global population and migration, and a larger level of cross border transactions and investment. The company is well positioned to take advantage of the rapidly evolving international payments industry under the leadership of incoming CEO, Richard Kimber, who will be taking charge from 1 June 2015. He said that he's excited about the opportunities that lie ahead and that the company has a proven global platform which can be widely leveraged.

Performance and growing customer base

Customer retention is the effect of growing the lifetime value of customers and adds operating leverage to the company. An indication of the company's success is seen in the continuous increase of the percentage of fee and commission income which can be attributed to customers more than three years old. This has happened despite the fact that in the US, competitors like Travelex and MoneyGram only came into operation in the last three years. Retention at 68% was below the previous year because of the lower retention rates achieved by Travelex and MoneyGram compared to the group average.

OZ Forex Daily Chart (Source - Thomson Reuters)

OZ Forex Daily Chart (Source - Thomson Reuters)

Performance continued to be strong across the group with continued growth in Australia/New Zealand its largest region. Strong penetration in the USA has resulted in robust revenue growth in North America. The increase in the existing customer base combined with successful targeted online acquisition has helped to catalyse strong EBITDA growth though I customer acquisition costs in the UK resulted in shrinking margins. Growth in Asia was lower than expected as a result of the competitive environment and Wholesale reported a strong performance with the momentum continuing to build.

All segments showed satisfactory performance reporting income growth of 25% in fees and commissions to transaction costs increased as a percentage of income because of higher wholesale commissions paid to partners. There was an increase in interest income because of the higher yield on deposits. Operating expenses showed an increase in promotional costs on additions to new dealing clients and the group also increased headcount expenses to support and grow the growth in operations. Non-recurring professional fees of $ 1.2 million was paid out as a result of activities in core operations and business development.

The group continued to remain free from interest-bearing debt and the increases in cash were offset by increases in liabilities from clients. Net cash pre-dividend and inclusive of term deposits grew by 20% to $ 49.4 million. Cash flow conversion continued to be robust with $ 38 million in operating cash flow before tax and client liabilities. The ratio of free cash to EBITDA is in excess of 100% and the free cash flow is capable of supporting the dividend policy of 70% to 80% of statutory NPAT.

The banking relationships

The business model followed by the group necessarily requires banking relationships which provide transactional banking for receipts and payments in multiple currencies, wholesale foreign exchange services to provide hedging and liquidity and deposits. A number of global banking partners have teams specifically dedicated to this industry and the risk of overreliance on any single partner is eliminated by multiple banking relationships. The disappointment of the decision by Westpac has been overcome by replacing their services with new and existing banking relationships.

Industry trends and market opportunities

Banking services are increasingly going online to the speed of the transition varies from country to country. Digital products and services are increasingly moving to mobile devices and consumers are increasingly expecting one-stop services. In the payments industry, international transactions are becoming more important and taking place in real-time. Once again, mobile devices are becoming increasingly popular and crypto currencies are emerging as a small but viable alternative.

The market opportunities are both significant and growing. Global payments are forecast to grow between 2013 and 2018 at 7.8% to touch USD 2.3 trillion. Market penetration by the Money Service Business (MSB) industry continues to be low in the core regions serviced by the group.

On the basis of the latest results and the operating performance of the company, we are bullish about the prospects and think that the current low price represents a genuine buying opportunity for investors. We put a BUY on the stock at the current price of $2.18.

isclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...