Kalkine has a fully transformed New Avatar.

Company Overview: Orora Limited is a packaging company. The Company is principally engaged in providing a range of packaging solutions, including design and manufacture of packaging products, such as glass bottles, beverage cans, recycled paper, cartons and multi-wall paper bags. Its segments include Orora Australasia, Orora North America and Other. The Orora Australasia segment focuses on the manufacture of fiber and beverage packaging products within Australia and New Zealand. The products manufactured by this segment include glass bottles, wines closures, corrugated boxes, cartons and sacks, and the manufacture of recycled paper. The Orora North America segment is located in North America, and purchases, warehouses, sells and delivers a range of packaging and other related materials. The Orora North America segment also includes integrated corrugated sheet and box manufacturing and equipment sales capabilities; point of purchase retail display solutions, and other visual communication services.

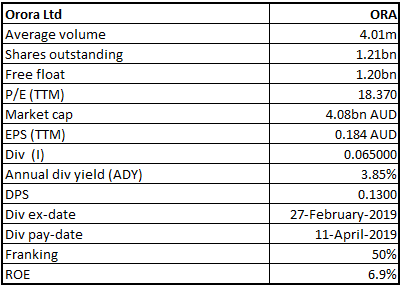

ORA Details

Rise Witnessed in Key Numbers in 1H FY19: Orora Limited (ASX: ORA) is a mid-cap packaging company with the market capitalization of ~$4.08 Bn as of 01 August 2019. It is primarily engaged with the customers in order to provide an extensive range of tailored packaging and visual communications solutions. The company has 43 manufacturing plants and 91 distributions sites across seven countries and employs around 6.8k co-workers. The company earlier came out with its results for the half-year ended December 2018 in which its consolidated statutory profit after tax for 1H FY19 amounted to $113.7 million, which reflects an increase of 9.5% as compared to $103.8 million in comparative period, and the company’s earnings witnessed a rise from $162.6 million to $175.1 million. The company had undertaken significant growth investments which can improve the broader performance of the company moving forward and could act as key growth catalysts. During the month of August 2018, the company made an announcement of the acquisition of Bronco Packaging and on November 28, 2018, the company made a 100% acquisition of the issued share capital of Pollock Investments Incorporated.

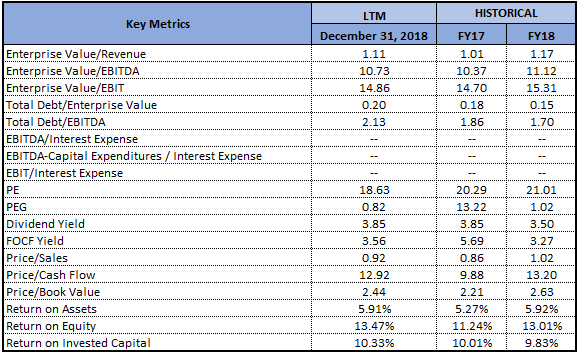

Coming to the financial highlights of the business, the company’s net profit after tax (or NPAT) amounted to $113.7 million, which reflects a rise of 7.6% on the prior corresponding period (or pcp) while EPS stood at 9.4 cents per share (or cps), which implies an increase of 6.8% on pcp basis. Talking about the dividend health, the company declared an interim dividend amounting to 6.5 cps, which is 50% franked and 50% sourced from conduit foreign income account. This reflects an increase of 8.3% on pcp and equates the payout ratio of around 69%. The company’s net debt, as at 31 December 2018, stood at $872 million, showing a rise from $667 million as at June 2018 and up from $657 million on pcp basis. It was mainly because of recent growth investments. It looks like the company’s growth investments would eventually pay-off moving forward and can help the company in delivering respectable returns to its shareholders. Also, the company’s RoAFE (return on average funds employed) stood at 14.3% in 1H FY19, which reflects a rise from 13.9% at pcp, implying earnings growth and ongoing robust balance sheet management. At CMP of $3.34, the stock of the company is trading at P/E multiple 17.22x of FY20E EPS.

Considering the commitment towards sensible debt levels, robust balance sheet, cost synergy opportunities of Pollock and Bronco and improvement in RoAFE with respectable payout ratio, we believe the company holds significant potential to achieve further growth. The company is also focused on shareholder value creation. Based on the foregoing, we have valued the stock using the two Relative valuation methods, P/E and EV/Sales and the four-year average P/E of 17.79x for FY20E with the consensus EPS of $0.194 and have arrived at the target price in the ambit of $3.45-$3.52 (single-digit upside (in %)).

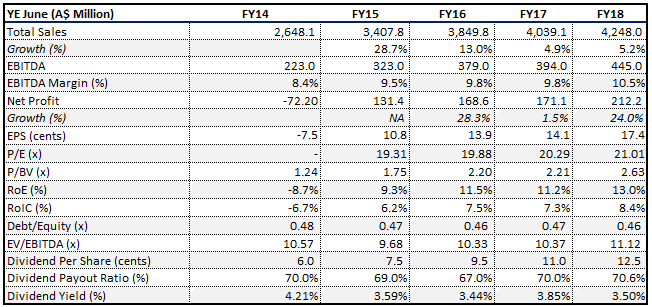

Key Financial Metrics (Source: Company Reports, Thomson Reuters), *NA: Not Applicable

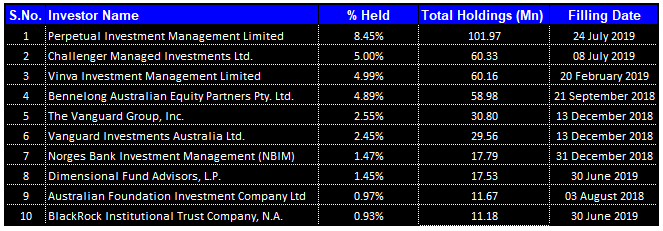

Top 10 Shareholders: The following picture provides the broad idea of the top 10 shareholders of Orora Limited:

Top 10 Shareholders (Source: Thomson Reuters)

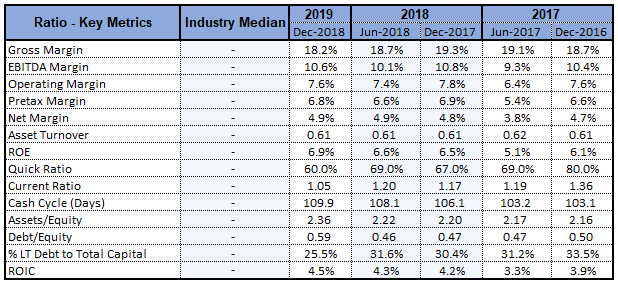

Respectable Position in Key Margins: Orora Limited is possessing a respectable position in its key margins as its net margin stood at 4.9% in 1H FY19, which reflects a marginal rise of 0.1% on a YoY basis and implies that the company has improved its capability to convert its top-line into the bottom-line. The company’s long-term debt as a percentage to total capital stood at 25.5% in 1H FY19, which reflects a fall of 4.9% on a YoY basis. The company’s cash conversion was in line with the expectations and stood at 52%, which reflects a fall from 63% in the pcp and might attract the attention of the market players moving forward.

Key Metrics (Source: Thomson Reuters)

The company has witnessed earnings growth, a rise in the dividends and higher returns which could help it in gaining traction among the market players. Additionally, it was mentioned that the robust balance sheet would be helping it to continue to pursue the growth opportunities moving forward. The continued rollout of the comprehensive risk profiling reviews and development of the improvement plans for each site might help the company from the safety performance front.

A Quick Look at Recent Updates: Recently, it was mentioned that the company’s Chairman named Chris Roberts, would continue as the Chairman into 2020 in order to assist with the smooth transition of new leadership on the retirement of Nigel Garrard as well as the appointment of Brian Lowe as the Managing Director and CEO. In another update, it was also mentioned that Mr Garrard would be leaving the company on September 30, 2019. It was also mentioned that Mr. Lowe joined the company in 2011 in order to lead Orora’s Beverage Business group and is presently Group General Manager, Orora Fibre Packaging Group.

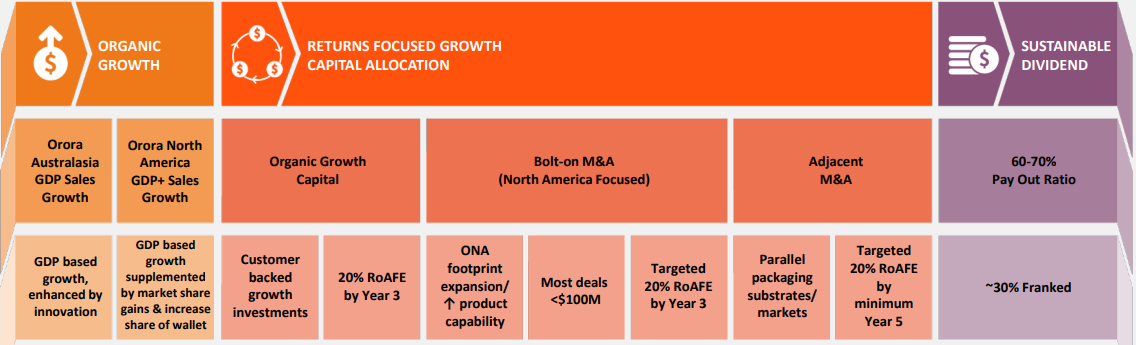

Key Takeaways From Macquarie Australia Conference Presentation: In the Macquarie Australia Conference Presentation, the company stated that North America happens to be the largest revenue generator. With respect to M&A integration update, it was added that the acquisitions of Pollock Packaging and Bronco Packaging are aligned to the company’s North American focused M&A growth strategy in Orora Packaging Solutions (or OPS). The combined consideration stood at US$104 million and they both have good cultural alignment. The company added that synergy identification has been progressing as per the expectations, and the target is US$6.5 million, and the implementation of the synergies is underway. The following picture happens to be the company’s blueprint for creating the shareholder value:

Blueprint for Creating Shareholder Value (Source: Company Reports)

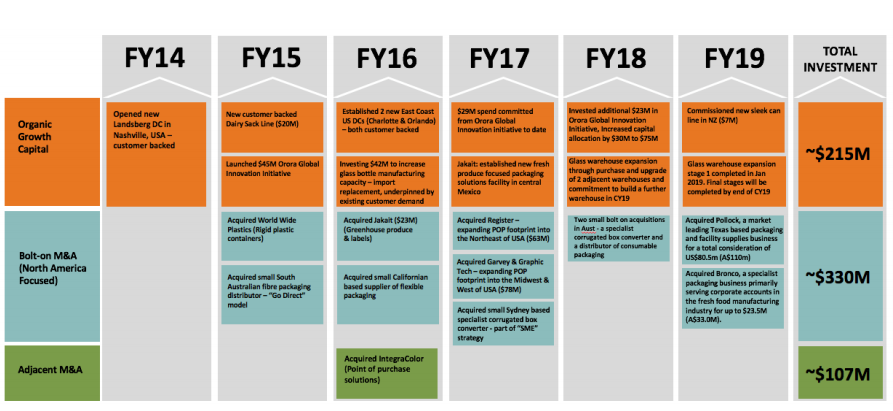

Deployments Made Might Support Long-Term Prospects: During half year ended December 31, 2018, around $215 million was deployed towards acquisitions, organic capital projects, and innovation in order to drive sustainable growth. This includes around $110 million towards the acquisition of Pollock, approximately $33 million to acquire Bronco and circa $57 million to support the asset replacement, upgrades as well as debottlenecking in the Australasian business group, which includes commissioning the secondary water treatment plant at Botany and the new can line in New Zealand. However, the deployments include around $18 million in North America to upgrade the manufacturing assets and ensure uniformity of capability in OV national network.

Total Investment (Source: Company Reports)

The Orora Global Innovation Initiative got established in the month of July 2015 involving an initial capital allocation amounting to $45 million to be deployed towards the innovation, modernisation as well as productivity throughout the business. In the month of February 2018, the initiative increased by $30 million to $75 million and it was mentioned that the additional funds would be deployed over the next 2-3 years. As at December 31, 2018, around $53 million has been committed to the initiatives which are focused towards delivering the new customer-led product solutions as well as enhancing the productivity. Also, around $2 million was deployed during 1H FY19. The company stated that numerous projects are completed/commissioned and delivering to the expectation and contributing to earnings growth.

Sustainable Dividend Payouts Might Attract Attention: The company has declared an interim dividend amounting to 6.5 cps which reflects a rise of 8.3% on a pcp basis, equating to the payout ratio of circa 69%. This payout ratio happens to be at the top end of 60-70% payout range, which reflects the company’s commitment towards its shareholders.

The company is committed towards generating further shareholder value via continued focus upon the profitable sales growth, cost control as well as efficiency, deployments in innovation and disciplined allocation of the free cash flow to the growth projects which are expected to meet the targeted returns. It was also mentioned that Orora only has the capacity to partially frank the dividends and an unfranked portion has been sourced from conduit foreign income account. The company has no longer capacity to maintain this level of sourcing, and as a result, commencing with final FY19 dividend, Board of Directors have determined that unfranked portion would be partially sourced from the conduit foreign income account. The estimated level of sourcing happens to be around 30%.

(1).png)

Sustainable Dividend Payouts Ratio (Source: Company Reports)

What To Expect From ORA Moving Forward: The company stated that it is reviewing the cost structures as appropriate and the adverse weather in Queensland had a minor impact. With respect to Australasia, it was mentioned that the company would continue to identify and implement the cost reduction opportunities. Additionally, it would invest in the asset upgrades and utilise Orora Global Innovation Initiative. Coming to the North America, Orora Packaging Solutions (OPS) is focused towards the integration of M&A and ERP optimisation, and these are the key drivers for future growth. The integration of Orora Visual acquisitions has been driving the business forward towards the targeted returns. The company expects to continue to drive the organic growth, integrate the recent North American acquisitions, and deploy towards the innovation during the remainder of FY19. Additionally, there are expectations that constant currency underlying earnings might be higher than reported in FY18.

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

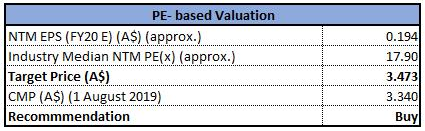

Method 1: PE- based Valuation

PE- based Valuation (Source: Thomson Reuters), *NTM: Next Twelve Months

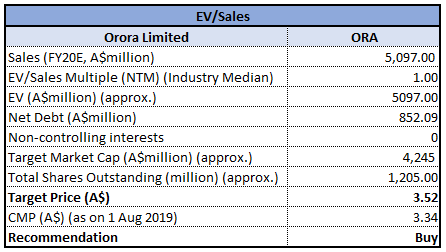

Method 2: EV/Sales Multiple Approach

EV/Sales Multiple Approach (Source: Thomson Reuters), *NTM: Next Twelve Months

Stock Recommendation: The company’s stock has delivered a return of 6.96% in the span of previous six months, while in the time frame of past three months, the stock’s return stood at 9.74% which can be considered at respectable levels. The company stated that Pollock and Bronco happen to be high quality, accretive targets with a focus towards large and growing Texas market. Additionally, they have robust cost synergy opportunities. The acquisitions of Pollock and Bronco align with the company’s 4 key strategic M&A pillars, i.e., footprint, customers, capability, and talent.

The company is possessing decent balance sheet to enable further growth investment. Addition to that, it is committed to the sensible debt levels and the investment grade credit metrics. The company is maintaining a disciplined approach towards the expenditure and acquisitions, which could help the overall company in attaining the broader business growth.

Considering the above-stated facts, availability of headroom to finance growth and optimism surrounding the acquisitions, we are affirmative on the future potential of the company and expect that it might achieve long-term growth. Based on the foregoing, we have valued the stock using the two relative valuation methods, P/E and EV/Sales and the four-year average P/E of 17.79x for FY20E with the consensus EPS of $0.194 and have arrived at the target price in the ambit of $3.45-$3.52 (single-digit upside (in %)). Hence, we give a “Buy” rating on the stock at the current market price of $3.340 (down 1.183% on 1 August 2019).

.png)

ORA Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...