Company Overview - Origin Energy Limited (Origin) is engaged in the operation of energy businesses, including exploration and production of oil and gas; electricity generation, and wholesale and retail sale of electricity and gas. The Company has four segments: Exploration & Production, Generation, Retail and Contact Energy. The Generation segment is involved in natural gas-fired cogeneration and power generation in Australia. The Exploration & Production segment is engaged in natural gas and oil exploration and production in Australia and New Zealand and South East Asia. The Retail segment is engaged in natural gas, electricity, liquefied petroleum gas (LPG) and energy-related products and services in Australia and the Pacific. In October 2013, Origin Energy Ltd announced the completion of the divestment of Tariki, Ahuroa, Waihapa and Ngaere (TAWN) licenses, as well as the Waihapa Production Station and associated gathering and sales infrastructure in New Zealand, to New Zealand Energy Corp (NZEC).

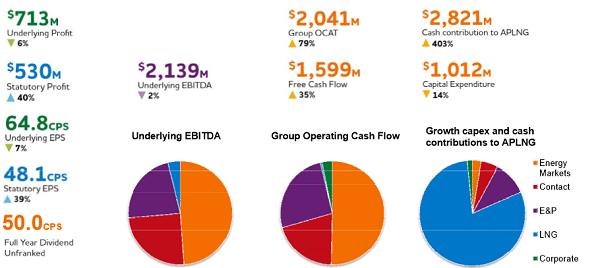

ANALYSIS - Origin Energy (ORG), the regional leader in energy markets with a significant position in Natural Gas and LNG production, reported a statutory pro?t increase of 40% to $530 million in FY14. The underlying Pro?t decreased by 6% to $713 million in view of weak contribution from the Energy Markets business, which got equipoised to some extent by increased contributions from all other business units.

2014 Full Year Financial Highlights (Source – Company Reports)

2014 Full Year Financial Highlights (Source – Company Reports)

ORG’s operating cash flow after tax rose by 79% from $1.14 billion to $2.04 billion owing to the better working capital from an improved billing and collections performance in Energy Markets and a reduction in taxes paid.

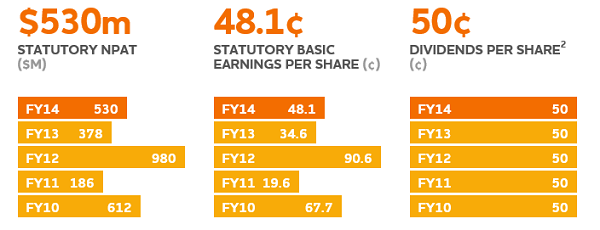

Statutory NPAT, Statutory Basic EPS and Dividends per Share (Source – Company Reports)

Statutory NPAT, Statutory Basic EPS and Dividends per Share (Source – Company Reports)

A sneak-peek into the operations reveals that ORG’s Energy Markets business encountered tough market conditions which were accompanied by a reduction in volumes owing to a decrease in electricity sales to the domestic mass market customers. Thus, indicating a lowered average consumption. Nonetheless, the margins improved in 2H14. The Company entered into a gas purchase agreement with Esso Australia and BHP Billiton with regards to its gas portfolio of the Energy Markets business. This has helped the Company to leverage the rising gas prices’ scenario through oil price-linked gas sales agreements with Queensland LNG projects and better footprint over mass market gas customers.

The Company reported that the Australia Paci?c LNG project (APLNG) is progressing as planned with an expectation to deliver ?rst LNG in mid-2015. The Company has further stated that it will be able to fund its commitments through to completion of the project in view of the $5.1 billion of existing liquidity as at 30 June 2014.

ORG’s Exploration and Production business indicated a record production and higher average commodity prices. The Company also announced for the acquisition of a 40% interest in the Poseidon exploration permits in Western Australia’s prospective Browse Basin. This will reduce the risk of securing opportunities to drive Company’s long term growth. ORG also intends to re?nance the debt facilities used for the acquisition through the issue of a new Euro hybrid security.

As indicated earlier, ORG’s underlying EBITDA decreased 2% indicating weak contribution from Energy Markets of $280 million and higher contributions from Exploration & Production, LNG and Contact Energy. Energy Markets underlying EBITDA was down by 21% to $1.05 billion. Nonetheless, the operational performance improved by the uplift in cash ?ows, sticky customer numbers and better customer experience. There was a 0.05% dip in customer accounts. The Company’s churn rate was 6% lower than the market rate. There was some improvement in the margins in the second half based on the better performance of the existing businesses.

Te Mihi, New Zealand (Source – Company Reports)

Te Mihi, New Zealand (Source – Company Reports)

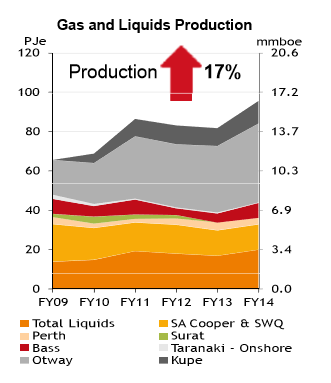

Underlying EBITDA rose by 23% to $487 million for the Exploration & Production business. This was owing to the better availability from main operating assets at Otway, Bass and Kupe basins. Also, investments in recent past have delivered higher production volumes. For LNG, the underlying EBITDA rose by 38% to $83 million indicating higher domestic gas sales and production. The Company further reported that its contribution to Australia Paci?c LNG rose from $561 million to $2.8 billion during the year. For Contact Energy, the underlying EBITDA increased by 9% to NZ$587 million owing to a better proportion of energy produced from hydro generation and the receipt of NZ$43 million of compensation relating to delays in the start-up of the Te Mihi Power Station.

ORG has a vital renewable position in view of the wind farm at Cullerin Range in Australia and geothermal and hydro generation owned by Contact Energy in New Zealand including the newly commissioned Te Mihi geothermal power station and other wind power purchase agreements. Further, there appear to be development opportunities under the Contact Energy business in New Zealand, which include approvals for up to 250 MW of geothermal generation at Tauhara. Other wind development opportunities, such as Stockyard Hill in Victoria, and geothermal and hydro development opportunities in Chile and Indonesia, add to the feather. Exemplary opportunities under renewables entail the Energia Austral, 1000MW hydro project in Patagonia, and Energia Andina, portfolio of 12 geothermal exploration projects, in Chile; and the 240MW Sorik Marapi geothermal JV in North Sumatra, Indonesia. The Company has also expanded its gas exploration acreage opportunities within Australia. A farm-in agreement in the Cooper basin has also been completed during the year. A new exploration acreage in the Bonaparte Basin has also been awarded.

ORG’s Increased Exposure in Conventional and Unconventional Resources (Source – Company Reports)

ORG’s Increased Exposure in Conventional and Unconventional Resources (Source – Company Reports)

The Company believes that 2015 and 2016 ?nancial years will be a transitional period with the commencement of LNG production by APLNG in mid-2015. Gas margins’ expansion and better supply/demand balance in electricity markets is expected from increased LNG production. The Company aims to improve returns in the energy markets businesses, steer growth in the natural gas and LNG businesses and have better distributions for shareholders while having a better capital management. Further, FY15 will include a full year of Te Mihi generation with a full year of associated depreciation and interest costs. However, probable extended shut-downs (BassGas and Otway) to invest in sustaining production capacity for 2016 and beyond may lead to a reduced contribution from the Exploration and Production business in 2015. ORG expects to have the first LNG from Australia Paci?c LNG’s Train 1 to commence in mid CY15 and from Train 2 in late CY15. The first full year of earnings and cash flows from both APLNG trains is expected to be FY17 with distributable cash flow of around US$1 billion on average per year.

Increased Availability and Production from Upstream Assets following Investments (Source – Company Reports)

Increased Availability and Production from Upstream Assets following Investments (Source – Company Reports)

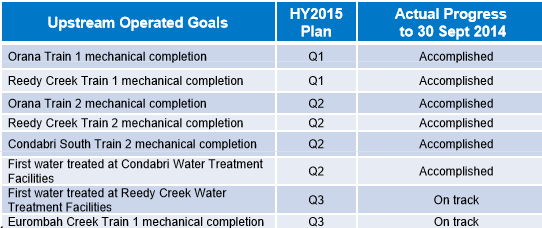

Looking at the APLNG’s upstream project, the progress with 85% completion of work as at 30 September 2014 looks appealing.

APLNG - Upstream Project Progress (Source – Company Reports)

APLNG - Upstream Project Progress (Source – Company Reports)

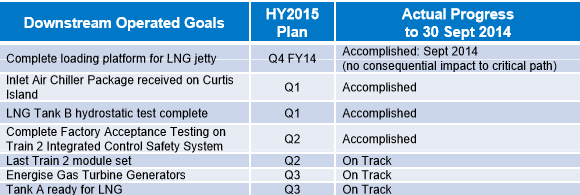

The downstream project is also progressing well with 82% work completion.

APLNG - Downstream Project Progress (Source – Company Reports)

APLNG - Downstream Project Progress (Source – Company Reports)

The recent APLNG site tour for CY14 may have indicated a few hiccups (such as the actual capital expenditure in non- operated areas being higher than anticipated) but the Company re-confirmed that the current guidance of mid-2015 is achievable. JV partner ConocoPhillips also recently stated that the first commercial cargoes are expected in 3Q or 4Q of 2015. ORG further made a refined change to its statement that APLNG will generate ~US$1bn in FY17 with an intention to reflect the May forward curve for oil prices. Moreover, APLNG is targeting a 30% improvement in per well drilling, completion and gathering costs from $3mn to $2mn by 2017.

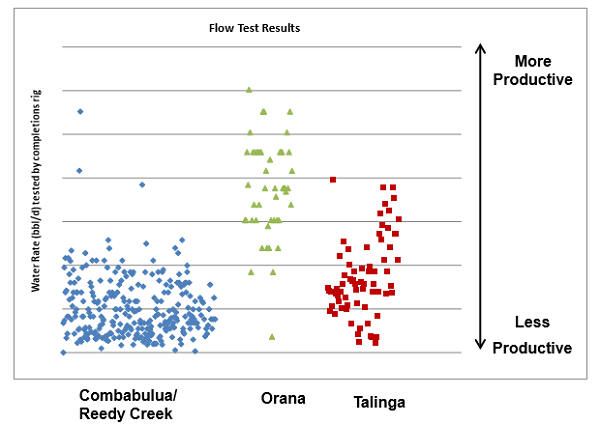

Combabula/Reedy Creek, Orana and Talinga (Source – Company Reports)

Combabula/Reedy Creek, Orana and Talinga (Source – Company Reports)

The Company reported that its retail transformation is complete with integration of nine systems into one with about 3.9m residential & SME customers being billed from SAP. The customer satisfaction scores have also improved. Customers are taking up new products, solutions and payment options. A recovery in electricity demand coupled with retail superiority could help improve the performance of the electricity retail division.

Origin Daily Chart (Source - Thomson Reuters)

Origin Daily Chart (Source - Thomson Reuters)

Most of the things on track, one point of concern revolves around the recent statement lodged by Tri-Star against APLNG claiming that the reversion trigger under the 2002 Deed of Sale was met in 2008 indicating that ownership of 22% of APLNG’s 3P reserves would revert to Tri-Star. ORG has earlier stated that the risk of reversion appears to be low which looks in consensus with the legal due diligence by ConocoPhillips and Sinopec with regards to the reversionary rights provisions upon taking equity in APLNG. ORG does not look very displeased, though there is some time before we get to have the final resolution.

Nonetheless, the overall play looks interesting; and accordingly, we put a

BUY recommendation for this stock at the current price of $13.42.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...