Company Profile – Origin energy (ORG) listed on the ASX in February 2000 after a de merger from Boral’s building materials business. ORG is vertically integrated energy company , via oil and gas production. With over 4.4 million retail gas and LPG customers in Australia and the Pacific and an effective interest in approximately 5,900MW of generation capacity. The firm is currently the largest producer of coal seam gas in Australia. ORG also owns 53% of contact Energy (NZ) after the acquisition from Edison Mission. It is headquartered in Sydney and employs over 5600 people. The company recorded revenues of $14,619 Million dollars for the financial year 2013, an increase of 13% over FY2012.

Origin energy is engaged in the exploration and production of natural gas and oil, power generation, and energy retailing and trading. The company’s key services include the following:

· Exploration and production of Oil and gas.

· Wholesale and retail sale of electricity and gas

· Electricity and steam generation

· Electricity trading

Analysis – Origin has struck an agreement with GLNG partners to sell gas providing a pathway for origin to monetise its gas portfolio in line with international oil linked pricing. Under the terms of the agreement, Origin will supply GLNG with at least 100 petajoules (PJ) of gas at Wallumbilla over period of 5 years commencing on January 2016. The agreement provides origin with an option to provide additional volumes of up to 94 PJ of gas to GLNG and preserves the flexibility to call back certain volumes of gas in to the origin’s portfolio during periods of high east coast gas or electricity market demand. This agreement marks a further positive step in ORG monetising the length in its east coast gas portfolio.

The bulk of the base contract 100 PJ will be supplied through volumes secured through Beach Energy Gas Supply Agreement signed last year. These volumes will be supplemented by volumes redirected from Darling Downs as ORG shifts the plant to a more intermediate to peak mode of operation.

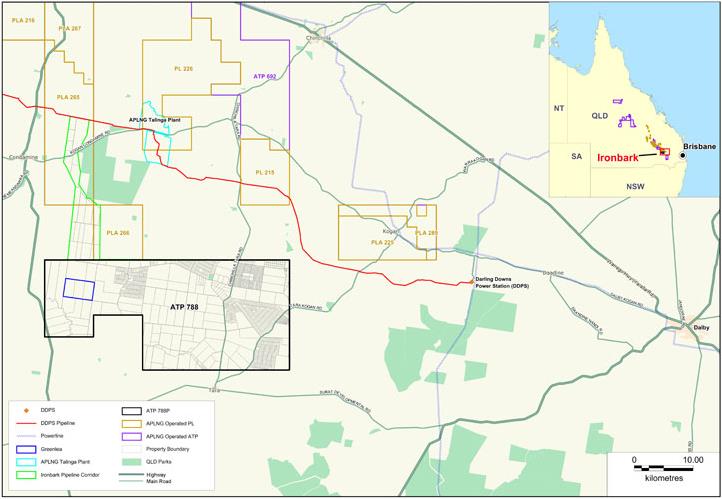

This also provides a path for Origin to monetise Ironbark. Ironbark Project is a coal seam gas (CSG) resource development project proposed for Origin’s Ironbark tenement. The Project is located in south-central Queensland to the north and west of the town of Tara, approximately 300 km west of Brisbane and 150km west of Toowoomba. Ironbark is likely to come online in 2017 and would provide the volume for ORG to take advantage of the 94 PJ option in today’s announcement. Ironbark will cost around $1 Billion to develop.

Origin’s Ironbark tenement is marked as ATP788 Source - Company Reports

Origin energy has a strong portfolio of onshore and off shore exploration permits in Australia and New Zealand. The exploration portfolio of origin energy includes off shire and onshore acreage in the Otway and Perth Basin, the offshore Bonaparte Bass Basins, and the onshore Cooper/Eromanga, Surat and Bowen Basins in Australia; and in the Taranaki, Northland and Canterbury Basins in New Zealand.

The company has major production interests in the Cooper Basin, which is the principal supplier of natural gas to New South Wales, South Australia and Queensland. Besides that it is one of the largest producers of Coal Seam Gas in Australia and has interests in the major CSG fields at Spring gully, Fairview and peat in central Queensland.

Origin energy has a wide customer base. The company's energy markets segment had 963,000 natural gas customer accounts, 3,014,000 electricity customer accounts, and 382,000 LPG customer accounts, at year-end June 2012. Origin Energy subsidiary, Contact Energy, had 443,000 electricity customers, 62,500 natural gas customers, and 61,700 LPG customers.

Source - Thomson Reuters

Source - Thomson Reuters

|

Price Performance |

Price % Change |

|

Close: |

14.09 (17-Jan-2014) |

3M: |

(3.03%) |

|

52 Wk High: |

14.90 (28-Oct-2013) |

6M: |

11.21% |

|

52 Wk Low: |

11.00 (21-Feb-2013) |

1Y: |

16.64% |

|

Dividend |

|

Yield |

3.977725 |

FY |

|

|

3.556317 |

5yr Av |

ORG sells electricity to the mass market. Investors are exposed to the risk of adverse hedging contracts or unexpected and unhedged movements in the pool price of electricity. Investors are moderately exposed to fluctuations in the oil price and to the org’s ability to replenish its reserves.

ORG is Australia’s largest vertically integrated energy retailer. ORG has diverse operations spanning the energy supply chain; from oil and gas exploration and production to power generation and energy retailing. ORG also has a 37.5% interest in Australia Pacific LNG (APLNG), which is expected to commence delivery of cargoes mid – 2015. In terms of ORG’s exposure to APLNG, the project continues to track in line with expectations for project delivery and cost. Furthermore ORG’s retail transformation and cost reduction programmes are set to contribute improved operating performance in the Energy Markets business over the coming years.

|

ORG (AUD, Millions) |

2013 |

2012 |

2011 |

2010 |

2009 |

|

Total Revenue |

14,619 |

12,935 |

10,344 |

8,534 |

8,042 |

|

1Y Growth |

13.0% |

25.0% |

21.2% |

5.9% |

(3.2%) |

|

Total Operating Expense |

14,116 |

11,575 |

9,949 |

7,658 |

372 |

|

Operating Income |

503 |

1,360 |

395 |

876 |

7,670 |

|

Net Income After Taxes |

461 |

1,058 |

248 |

680 |

6,998 |

As one can see from the above figures that the revenue has been growing year on year for the last 4 years consecutively. Origin’s Energy Markets business continued to make good progress on the integration of the NSW energy assets, as well as successfully completing a major SAP billing and customer relationship management system implementation. This new system will increase the efficiency of their operations, improve competitiveness and allow Origin to respond more effectively to customer needs.

|

|

Industry Median |

2013 |

2012 |

2011 |

2010 |

|

Profitability |

|

|

|

|

|

|

Gross Margin |

43.3% |

24.1% |

28.4% |

28.7% |

25.7% |

|

EBITDA Margin |

35.5% |

9.8% |

12.4% |

16.4% |

14.0% |

|

Earning Power |

|

|

|

|

|

|

Pretax ROA |

5.8% |

1.7% |

4.9% |

1.6% |

4.0% |

|

ROE |

10.8% |

2.9% |

7.7% |

1.7% |

6.0% |

|

Liquidity |

|

|

|

|

|

|

Quick Ratio |

1.25 |

0.68 |

0.77 |

0.70 |

1.51 |

|

Current Ratio |

1.47 |

0.72 |

0.81 |

0.75 |

1.61 |

The growth in Origin’s underlying profit and underlying EBITDA reflects the continuing strength of Origin’s underlying businesses. Energy Markets underlying EBITDA increased by 33% or $388 million to $1562 Million, an increase which was largely attributable to full year contribution from the acquired NSW energy assets. Exploration and Production Underlying EBITDA increases by 23 percent or $61 Million to $329 Million, primarily due to a lower exploration expense and higher commodity prices partially offset by higher operating costs.

There are a number of opportunities that Origin can pursue both domestically and internationally to drive growth in the medium to long term. Origin is well positioned to take advantage of the expected rise in domestic gas process. As evidenced by the recent gas sale to GLNG project at the international Oil Linked pricing, fuel integration is key source of Origin’s competitive advantage.

We put a buy recommendation on origin at current closing price of $13.88.

Disclaimer

Kalkine provides general advice on securities. Kalkine does not provide advice that takes into account your, or anybody else’s investment objectives, financial situation or needs. We strongly suggest that you should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. Employees and/or associates of Kalkine Pty Ltd may hold one or more of the stocks reviewed on this website. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...